Pinterest (NYSE: PINS) Q1 earnings gave 2019 guidance for revenues of only $1.1 billion, disappointing analysts’ estimates and driving a big fall in the stock after hours. International revenue was minimal at $0.08 per user and will need to grow above $1.00/user to make the business sustainable.

Click Here for our in-depth 30-page guide to investing in Pinterest.

Bottom Line

Pinterest’s first earnings release as a public company should be another reminder to investors to be very careful about buying IPO shares.

The IPO has been well received by investors with shares popping 30% on the first day of public trading and up a further 30% in the month that followed.

This strong stock price performance reflected very positive investor sentiment backed up by big growth estimates from bank analysts.

Unfortunately, early earnings results from newly public companies often fail to meet sky-high expectations and Pinterest is no different.

The company’s earnings results were in line with previous guidance, but guidance for the rest of 2019 was much lower than analysts were expecting, a full 40% below our estimates, and the stock is now down 17% after hours.

At the current price of $25/sh Pinterest is only up 10% from where it opened on the day of the IPO leaving early investors perilously close to where they started.

Pinterest is at a Very Important Crossroads

If management can grow the user count past Twitter and Snap, the bull case for the stock could be legit.

Our greatest fear is that Pinterest is copied by a larger platform like Instagram and goes ex-growth. Continued user growth is key to proving this company can successfully survive a Facebook and Google dominated world.

Historically tech stocks have not done well at price to sales ratios above 10x and with Pinterest sitting at 17x based on 2019 revenue guidance, the stock is unlikely to find support above $16/sh in our opinion.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]We recommend investors sit on the sidelines until numbers show the company is successfully monetizing users outside the U.S. and user numbers have surpassed Twitter while still growing 10%+ per quarter. [/su_panel]

What Went Right in the Quarter

Pinterest is still showing good user growth.

Users were up 22% year over year which was in line with our expectations. User growth has stayed steady at around 20%+ per quarter over the last year which is a win for management.

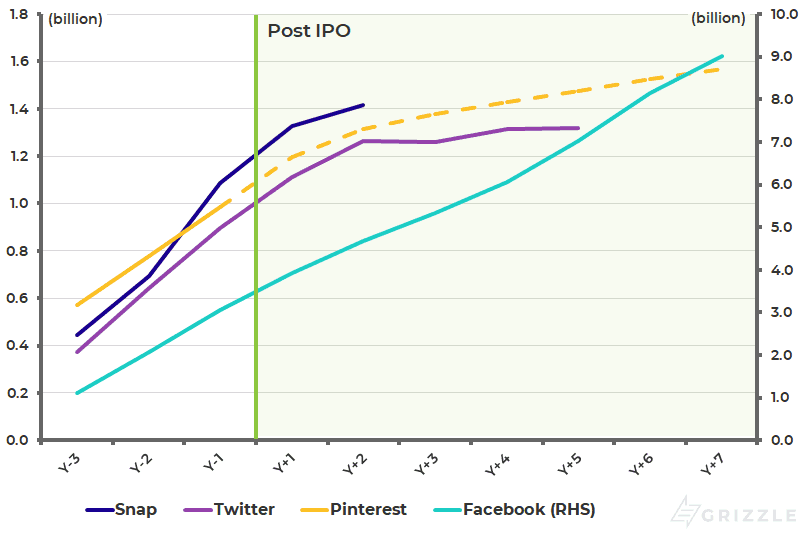

Pinterest is on pace to pass Twitter’s user count by mid-year and Snap’s by sometime in 2020 driven by strong international growth.

Grizzle MAU Estimates

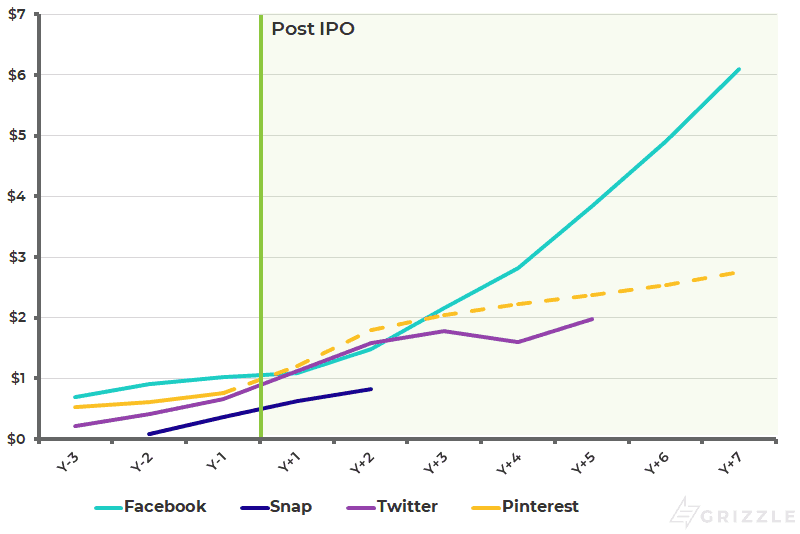

Revenues per user were up strongly as well and are still growing at historical rates.

International revenue remains low compared to peers, but offers the most potential to maintain healthy revenue growth over the next few years.

Grizzle ARPU Estimates

What Went Wrong in the Quarter

Revenue per user internationally is still only a blip compared to the U.S.

The company said they are building out a sales force outside the U.S. but it will take time, basically the rest of 2019.

Without the contribution of international revenue and a stagnating user base in the U.S., Pinterest is going to struggle to show the revenue growth investors are looking for in 2019.

Costs in the quarter were also a disappointment, coming in much higher than we were expecting.

Total costs were 120% of revenue in the quarter compared to our expectations that 2019 costs could be below 100% of revenue.

The company is spending more than we expected on headcount to maintain growth and the guidance of a $45-$70 million EBITDA loss this year reflects that spending.

It is looking like Pinterest will break even sometime in 2020.

Summing it All Up

Pinterest is a platform that shows real promise, but the next year will be pivotal in determining the future of the company.

If Pinterest can fend off Facebook’s Instagram and find a way to generate real money from international users, the stock has tangible upside.

However, if Pinterest only grows to the size of Twitter or Snap, the stock is worth $10/sh or less.

Investors should watch this stock closely to see if price weakness opens up an attractive entry point.

Buying the stock at $10-$15/sh or below offers investors a balanced risk/reward tradeoff in our minds.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.