Pinterest (NYSE: PINS) beat big on Q2 earnings. Revenue came in 10% ahead of consensus and the EBITDA and Net Income Loss were a full 40% below what analysts were expecting. Pinterest will likely turn a profit in 2020, 1 year ahead of expectations. Most of all, growth in both users and revenue per user is actually accelerating which the market has to love.

Click Here for our in-depth 30-page guide to investing in Pinterest.

Bottom Line

Pinterest is a tale of two markets. If you compare the stock to peers simply based on multiples it looks fairly valued.

Pinterest is growing users far faster than peers like Twitter and Snap while revenue per user is growing in line with peers. This above-average growth is reflected in the 100% premium Pinterest trades for on a user profitability metric.

| Company | MAU 2018 (MM) | Rev/ MAU | Market Cap ($MM) | Mkt Cap/ User | Price/ Revenue Per User | YoY MAU Growth | YoY ARPU Growth |

| 2255 | $6.09 | 501,500 | $222 | 37x | 9% | 20% | |

| 389 | $2.16 | 32,520 | $84 | 39x | 6% | 25% | |

| 291 | $0.79 | 19,901 | $68 | 87x | 32% | 29% | |

| Snap | 383 | $1.01 | 23,170 | $60 | 60x | 3% | 38% |

| Average (Ex PINS) | $3.09 | $122 | 45x | 6% | 27% |

| Company | MAU 2018 (MM) | Rev/ MAU | Market Cap ($MM) | Mkt Cap/ User |

| 2255 | $6.09 | 501,500 | $222 | |

| 389 | $2.16 | 32,520 | $84 | |

| 291 | $0.79 | 19,901 | $68 | |

| Snap | 383 | $1.01 | 23,170 | $60 |

| Average (Ex PINS) | $3.09 | $122 |

| Company | Price/ Revenue Per User | YoY MAU Growth | YoY ARPU Growth |

| 37x | 9% | 20% | |

| 39x | 6% | 25% | |

| 87x | 32% | 29% | |

| Snap | 60x | 3% | 38% |

| Average (Ex PINS) | 45x | 6% | 27% |

However, we live in a world of quantitative easing where money costs almost nothing and valuations across the equity landscape are stretched to say the least.

If we move away from relative value and look at absolute value we see problems with Pinterest.

Even if we assume Pinterest becomes more profitable than Twitter and attracts twice that platforms users, the stock is fundamentally only worth $12.50/sh.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]For Pinterest to justify a stock price above $20/sh it would have to take serious ad dollars away from Facebook and Google. Considering no company has been able to break the advertising stranglehold these two juggernauts have over the market we think investors are making a very risky bet. [/su_panel]Putting our trading hat on, we think Pinterest could gain some momentum off the back of this earnings report. It will continue to trade at a premium to Twitter and Snap and could continue to go up with earnings beats.

But once this bull market turns and risk matters again, the fundamental floor for this stock is far away indeed.

Pinterest is at a Very Important Crossroads

If management can grow the user count past Twitter and Snap, the bull case for the stock could be legit.

Our greatest fear is that Pinterest is copied by a larger platform like Instagram and goes ex-growth. Continued user growth is key to proving this company can successfully survive a Facebook and Google dominated world.

Historically tech stocks have not done well at price to sales ratios above 10x and luckily for Pinterest the multiple should fall to 10x or below by next year due to strong revenue growth.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]We recommend investors trade the stock around earnings but wait for confirmation the company is successfully monetizing users outside the U.S. and user numbers and profits per user have surpassed Twitter before building a long term position. [/su_panel]

What Went Right in the Quarter

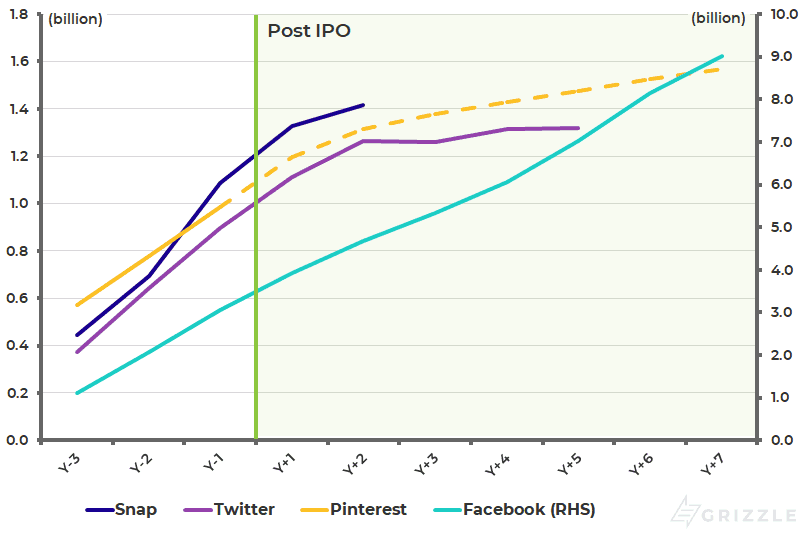

Pinterest is still showing peer leading user growth.

Users were up 30% year over year which is actually an accelerating from last quarter. User growth has stayed steady at around 25%+ per quarter over the last year which is a win for management.

Pinterest is on pace to pass Twitter’s and Snap’s user counts by mid-2020 driven by strong international growth.

With revenue growing ~60% year over year, at almost twice the pace of peers, Pinterest should continue to track or exceed the stock performance of Twitter and Snap.

Grizzle MAU Estimates

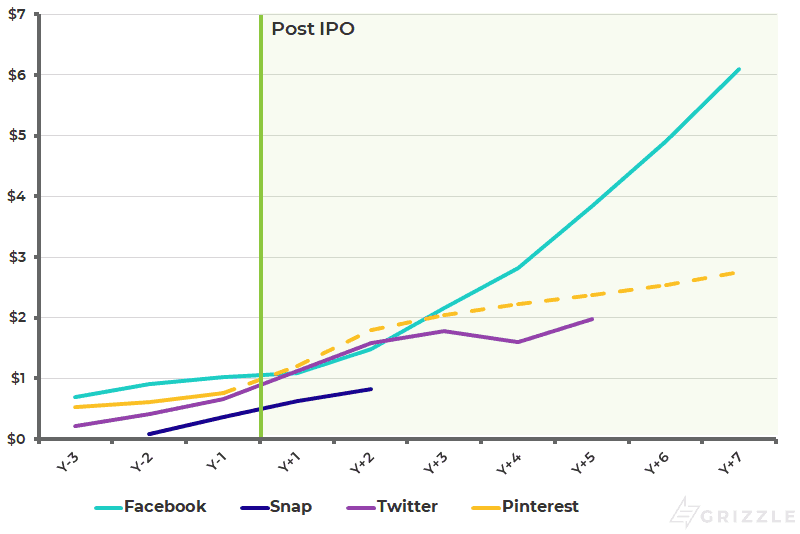

Revenues per user were up strongly as well and are still growing at historical rates.

International revenue remains low compared to peers, but is likely what analysts are watching closely as the engine of healthy revenue growth longer term.

Pinterest ads convert to sales at twice the rate of other platforms meaning theoretically Pinterest should generate far superior revenue per user than Twitter or Snap.

Grizzle ARPU Estimates

Summing it All Up

Pinterest is a platform that shows real promise, but the next two year will be important to determine the future of the company.

If Pinterest shows it can fend off Facebook’s Instagram and find a way to generate real money from international users, the stock has tangible upside to $40/sh.

However, if Pinterest only grows to the size of Twitter or Snap, the stock is worth $10/sh or less.

Investors should watch this stock closely and play the momentum from solid earnings results, but if the overall stock market begins to show cracks this is not a stock that will provide any shelter from the storm.

Buying the stock at $10-$15/sh or below offers investors a balanced risk/reward tradeoff in our minds.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.