Social media and shopping platform Pinterest (NYSE:PINS) announced earnings that beat expectations.

Investors may like the company’s $1.52 billion revenue guidance for 2020 but will likely be disappointed by the limited EBITDA guidance for next year even though Q4 was better than expected.

Revenue came in at $400 million, above consensus of $369 million and management’s own guidance of $365 million.

Revenue growth of 46% was just shy of last quarter’s growth of 47%.

Adjusted earnings per share beat estimates, coming in at $0.12 compared to the consensus estimate of $0.08.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Pinterest is still priced like it will become the second most profitable social media property behind Facebook. With no indications yet that revenue per user will ever surpass Twitter, we will be on the sidelines until the stock comes down below our long-term price target of $16/sh [/su_panel]

Pinterest’s multiple has come down significantly since last earnings when the stock was closer to $25, but it still is slightly expensive given the much lower monetization levels than peers.

Pinterest makes 35% less per user than Snap and 60% less than Twitter.

The Pinterest platform is built for monetization so the cashflow will come, but the stock is still pricing in that Pinterest becomes the most profitable social media platform behind Facebook.

We have absolutely no data indicating this will be the case, making this a risky bet at this time.

| Company | 2020 P/S | Revenue Growth Rate | (Avg Rev Per User) |

| Snap | 7.3x | 32% | $1.36 |

| 6.3x | 46% | $0.87 | |

| 5.9x | 19% | $8.44 | |

| 6.3x | 13% | $2.03 |

Ever since the IPO, we could never justify a stock price higher than $16/sh, even if we assume Pinterest becomes more profitable than all of its competitors, except for Facebook.

ARPU Needed to Justify Only $16/sh

Our handy visual guide below will help you make buy and sell decisions if you choose to invest in Pinterest over the long term.

Grizzle Guide to Buying or Selling Pinterest Stock

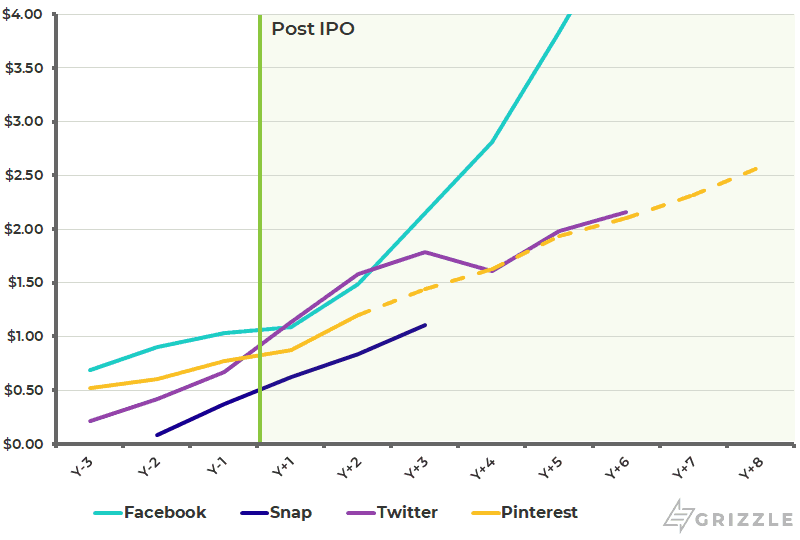

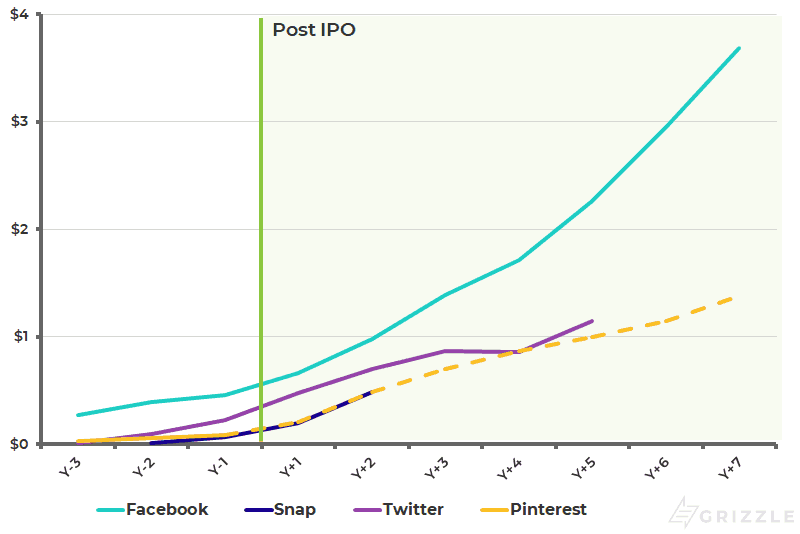

PINS has Been the Worst Performing Social Stock Since its IPO

Snap has been improving the EBITDA loss rapidly in 2019, driving a rebound in the stock.

If we back out stock-based compensation which is non-cash, the EBITDA loss was only $40 million or 10% of revenue last quarter, compared to $138 million or 50% of revenue a year ago.

Snap guided to $10 million of EBITDA this quarter and the fact that they beat both their guidance and market expectations is a good sign.

Management subsequently guided to a return to losses next quarter and likely killed some of the positive sentiment from this quarter’s cashflow beat in the process.

EBITDA Loss Improving Quickly

Pinterest is accelerating the revenue it generates from each user but is still lagging the profitability of Twitter, Snap, and Facebook when they were at the same stage of growth.

The market is pricing in a nice acceleration in per user revenue and if Pinterest doesn’t at least meet Twitter’s numbers, the stock has further downside to it.

It is still early days for management and they are only a year into figuring out how to fully monetize their platform internationally which is where the real growth will come from.

Watch international revenue per user closely as it could foreshadow the acceleration in revenue the company needs to get the stock moving higher.

PINS International Profit Per User Still Has a Long Way to Go

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.