https://youtu.be/-MVCtS_DV4g

Pot Stock Investors Meet the Kitchen Sink

When the capital landlords of Canopy Growth (TSE: WEED, NYSE: CGC), Constellation (NYSE: STZ) showed Mr. Bruce Linton the door in July it was clear as day that write-downs were on deck. Grizzle outlined exactly how it would play out the moment it happened — the stock is down nearly 70% since our note.

We now have full confirmation with Canopy’s latest earnings release that the company is in full write-down/kitchen sink mode. We outline the ugly downside in our review of the earnings.

For a normal established sector, seeing a bellwether go down isn’t a mortal wound for the industry, however, for an emerging sector like cannabis built on a lot of hype and promises it makes things very difficult for the rest of the pot stocks complex.

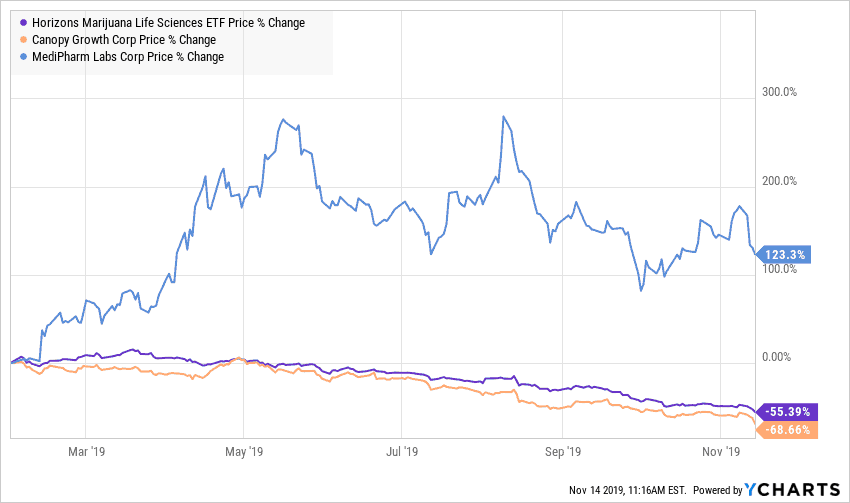

Cannabis ETF (HMMJ) & MediPharm Performance Since Canopy Growth Share Price Peak (Jan 31/19)

Where’s the Bottom?

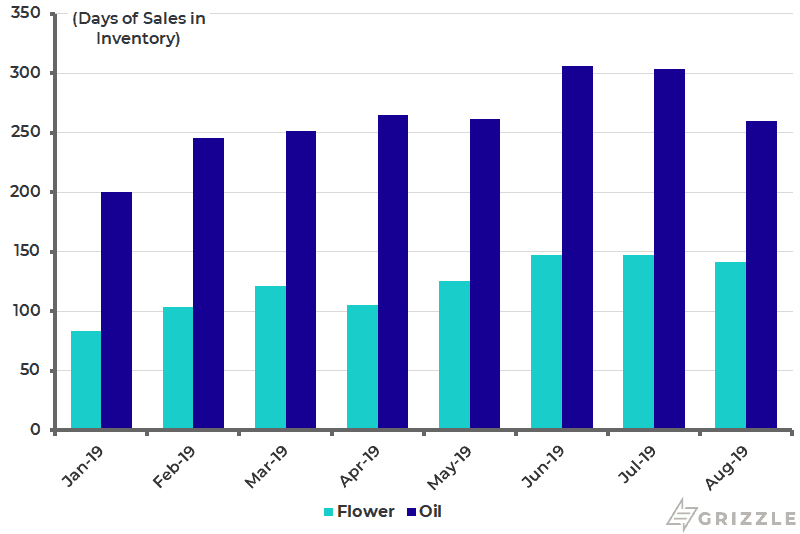

As I highlighted in my note yesterday there simply isn’t anything fundamental you can hang your hat on in this sector. Cannabis is a commodity and commodity stocks can’t begin to rally until the supply/demand imbalance gets sorted out…. and it’s a big issue — we’re sitting on 250 days of cannabis oil inventory.

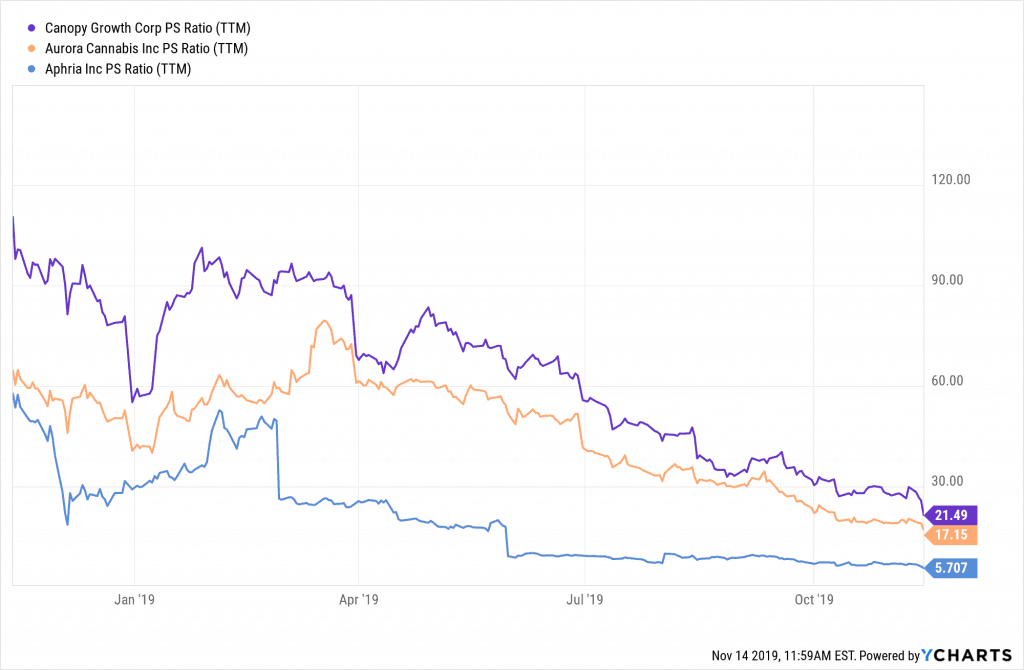

Additionally, operational results have been abysmal for big players, heck one of them even grew pot illegally — CannTrust (ha!). Trailing Price-to-Sales is as good of a measure as any to use for a sector continually disappointing investors. We simply don’t see a scenario where Canopy or Aurora (TSE: ACB; NYSE: ACB) should continue to trade at a multiple 3-4x higher than Aphria (TSE: APHA; NYSE: APHA).

Trailing 12-Month Price/Sales

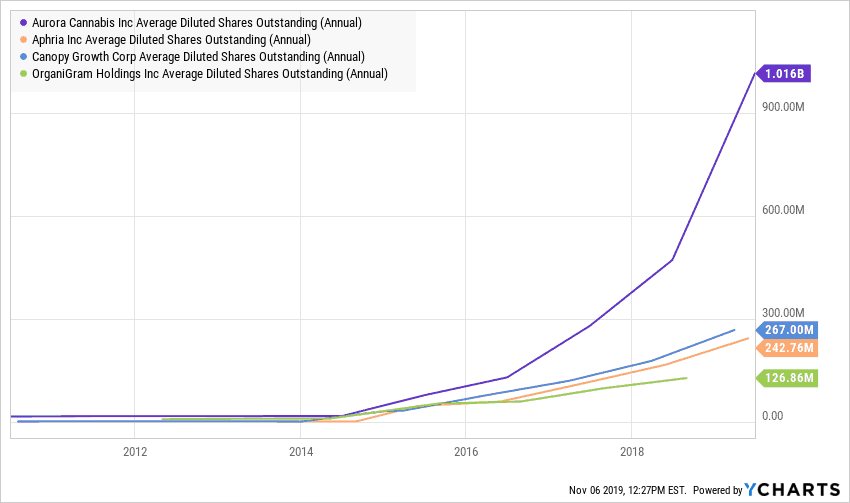

Also, let’s not forgot that Aurora has a wee little problem of obscene share count. At last tally they were well over 1 Billion (yes capital B) shares outstanding.

Average Diluted Shares Outstanding

Trading Pot Stonks

Obviously the easiest tactical move here is to stand back and watch ugly stocks that couldn’t really ever grow pot swirl down the drain.

There’s still a lot of valuation multiple premium to short in Aurora and Scott’s analysis of Canopy suggests we could easily see the stock sell off another 50% without looking ‘cheap’.

The cannabis extraction stocks (MediPharm, Valens) in our view are very exposed to the downside. MediPharm (TSE: LABS) is up over 120% YTD vs the sector (TSE: HMMJ ETF) down -55%. Peak operating margins are never a good look for commodities and the stocks have significantly outperformed the cannabis peer group.

The view that cannabis extraction stocks can magically ‘decouple’ from a sector-wide oversupply is naive at best.

M&A Wildcard

It’s been nearly a year since we’ve heard any hype about mega-cap consumer product companies (CPG) looking to get splashy with an investment in the cannabis sector. And frankly why would they? Constellation and Altria have literally taken a capital bath in their investments of Canopy and Cronos, respectively.

Our view is that either Canopy or Cronos are far better off acquiring a producer that can actually grow good pot versus continuing to grow their own ditch weed or chasing unfruitful celebrity joint ventures.

Every #potstocks rally continues to get FADED, harsh reality of oversupply (of ditch weed)

Companies with a semblance of a balance sheet ( $CRON, $WEED) should/will at some point have a critical look at companies that CAN grow chronic at scale ( $WMD, $FIRE, Tantalus… ) https://t.co/hdCUNkLtGX

— Thomas George (@thomasg_grizzle) November 12, 2019

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.