The old investing adage ‘buy the rumour, sell the news’ befits cannabis equities rather well right now. In Canada recreational cannabis went legal on Oct. 17, a jubilant time for cannabis connoisseurs, not so much for cannabis investors.

Bear Market Triggered

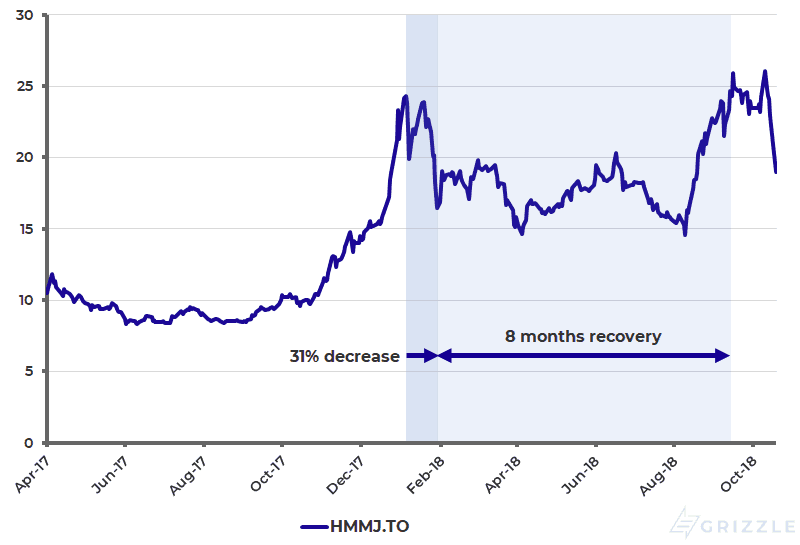

It’s been nothing short of a bloodbath since Oct. 17. The Horizons Marijuana Life Sciences Index ETF (Ticker: HMMJ, $900M Net Assets) has fallen -22%, deep in bear market territory (a fall greater than 20%). Additionally from the peak (Oct. 15) the index has fallen 27%.

Since the inception of the ETF (April 4, 2017) we’ve seen one other significant bear market that was triggered after Jan. 10, 2018. In the following 3 weeks the index plunged 31% and it took 8 months for the index to reclaim the previous peak (Sept. 11).

Horizons Marijuana Life Sciences Index ETF (Ticker: HMMJ)

Should Cannabis Investors Hibernate Till Spring?

We’re pretty much at the same draw down levels as the last bear market (-30%), however we believe the market dynamics are fundamentally different between the two.

In both bear markets, frothy valuations have been the main market concern cited by financial media and financial pundits. We do believe there is a significant amount of speculation in the periphery of the cannabis sector — overvalued small-cap companies with dreams of production but nothing tangible to show today.

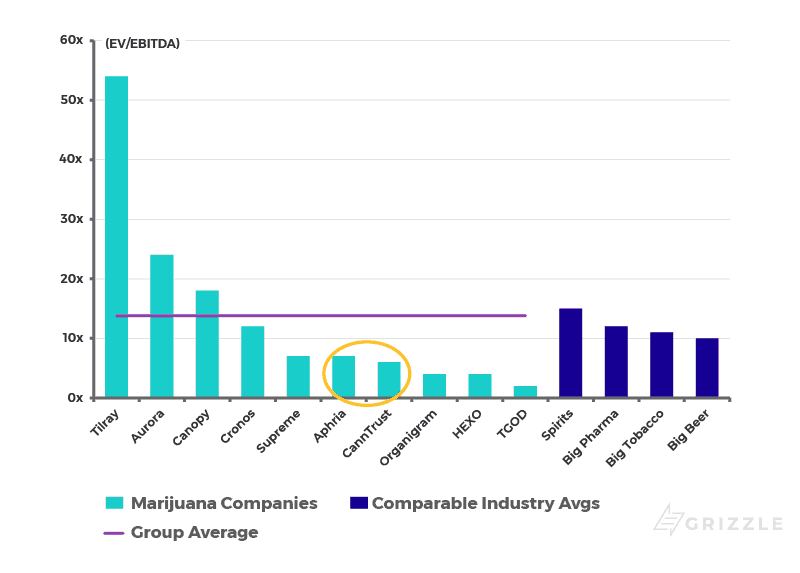

However, there is a group of high-quality large-cap companies that are trading at very attractive valuation multiples. In our view companies like Aphria (tickers: APH / APHQF) and CannTrust (Ticker: TRST) present significant long-term value for patient investors.

2020 EV/EBITDA Multiples

The critical difference between the two bear markets is the new M&A/partnership market dynamic that was triggered by beer and spirits maker Constellation Brands’ (Ticker: STZ) $5 billion investment in Canopy Growth on August 15. This was the catalyst of the current bull market run in the entire cannabis space.

Other consumer companies have been put on notice by Constellation. They have to either pony up now to enter the cannabis sector or play a wait-and-see approach. The challenge for consumer companies is that they have effectively gone ex-revenue-growth as a result of their portfolio of outdated brands and are desperately seeking new products that appeal to millennials.

As the Economist has noted, Diageo, Coca-Cola and Altria are all rumoured to be considering deals in the sector. Consumer companies interested in participating in the cannabis sector in a meaningful way don’t have the luxury of waiting a year or two; a veritable lifetime in branding and product development.

We believe it is for this reason that cannabis investors should maintain core holding in high-quality companies that are targets for M&A. There is no way to know when these deals will hit the tape so it makes sense to remain fully invested. These core high-quality holdings currently trade at valuation multiples below that of their acquirers — specifically Spirits, Pharma, Tobacco, and Beer companies.

The Cannabis Rally has been Driven by Retail Investors; When will Institutional Investors Step in?

The massive $51 billion market capitalization of the cannabis sector has been driven primarily by Canadian retail investors. This has truly been a euphoric bull market where institutional investors (mutual funds) have missed the party in a very meaningful way.

Up until very recently, risk adverse Canadian institutional investors didn’t have a particular reason to dabble in the speculative cannabis asset class. However, for portfolio managers benchmarked against the S&P/TSX Composite index the cannabis sub-sector now has a weight of 1.2%; this is not an immaterial weight from a risk perspective.

Institutional portfolio managers are always wary of looking dumb and buying a stock they missed at the top of the market as the scrutiny they’ll get from the risk management department and the Chief Investment Officer will be significant. A better setup is to buy the stock after a meaningful pullback (>20%) and go benchmark weight.

On that note, one of the most well respected agricultural analysts on Bay Street, Ben Isaacson from Scotiabank, initiated on the cannabis sector last Friday with an ‘Outperform’ recommendation on Aphria (target price of $26 per share CAD) and ‘Sector Perform’ recommendation on Canopy Growth ($61 per share CAD).

Broad Market Weakness Could Hamper Cannabis Recovery

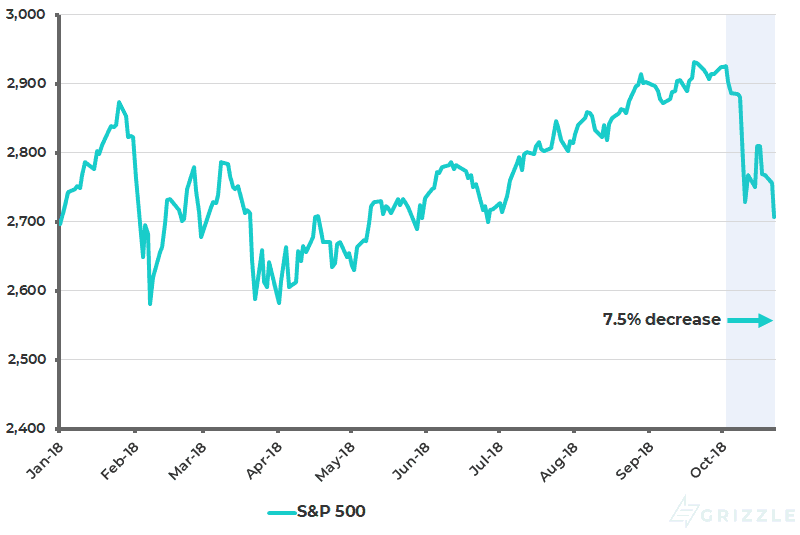

Another very real challenge for cannabis investors is the broad market weakness globally. The S&P 500 has fallen 8% from its recent highs and is on pace for its fifth straight weekly decline.

We believe that if this weak global market dynamic continues to play out, cannabis equities will continue to trade like risk assets — i.e. they will fall greater than the market.

Owning high-quality blue chip cannabis equities that are positioned as M&A targets is in our view the optimal risk/reward strategy for investors. Our preferred name in Canada is Aphria.

S&P 500 Index

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.