If there is an area of American finance likely to blow up in any coming downturn, where the dynamic is driven by the unwind of QE-driven asset inflation, it is most likely to be the so-called ‘private equity’ industry which has been the biggest winner in the ten-year cycle since the global financial crisis.

Private equity is often viewed as consisting of nothing more than substituting debt for equity on a company’s balance sheet, firing employees, cutting R&D and capex, and paying out huge fees to private equity firms. There is a lot of truth in this.

Is Private Equity Really Worth It?

This writer recently came across an interesting critique of private equity that is worth reading (see American Affairs Journal article “Private Equity: Overvalued and Overrated?” by Daniel Rasmussen, Spring 2018).

The author reports how his firm, Verdad, compiled a comprehensive database of 390 private equity deals. In 54% of the transactions examined, revenue growth slowed. In 45%, profit margins contracted, and in 55%, capex spending as a percentage of sales declined. The author went on to note that there is a big difference between what private equity used to do, namely buying companies at 6-8x Ebitda with debt at a reasonable 3-4x Ebitda, and what private equity does today, which is buying companies at 10-11x Ebitda with debt at 6-7x Ebitda.

In a further sign of excess, the author describes how private equity funds are now coming up with so-called “long-dated funds” with longer lockup periods, and buying companies from other funds they manage. The author writes: “This shell game of overpriced deals getting pawned off to other pools of capital is evidence of rising private equity froth”.

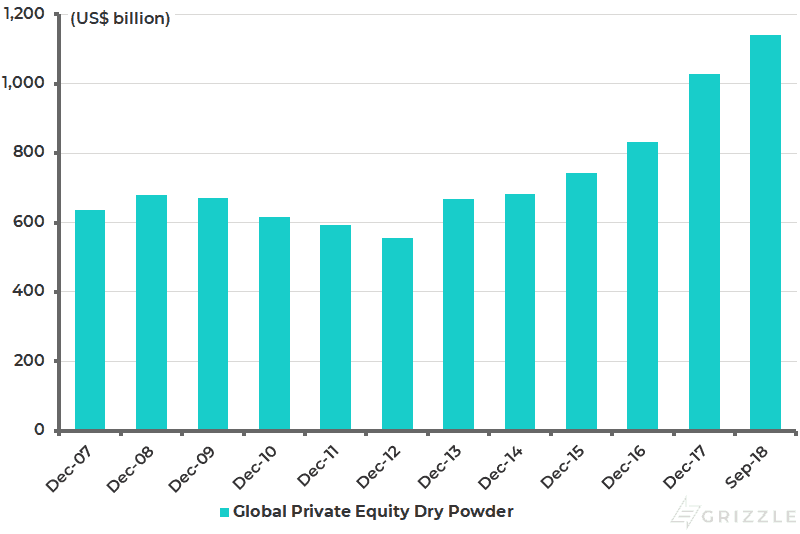

The excesses have only grown since this article was published with the latest estimates indicating that the global private equity industry now has US$3.1 trillion in assets under management with US$1.1 trillion in cash, or so-called ‘dry powder’, to invest, according to private equity data provider Preqin (see following chart). The obvious problem in the making is the debt the private equity industry has taken on to finance these deals.

Global private equity dry powder (cash reserves)

The Growth of Leveraged Finance

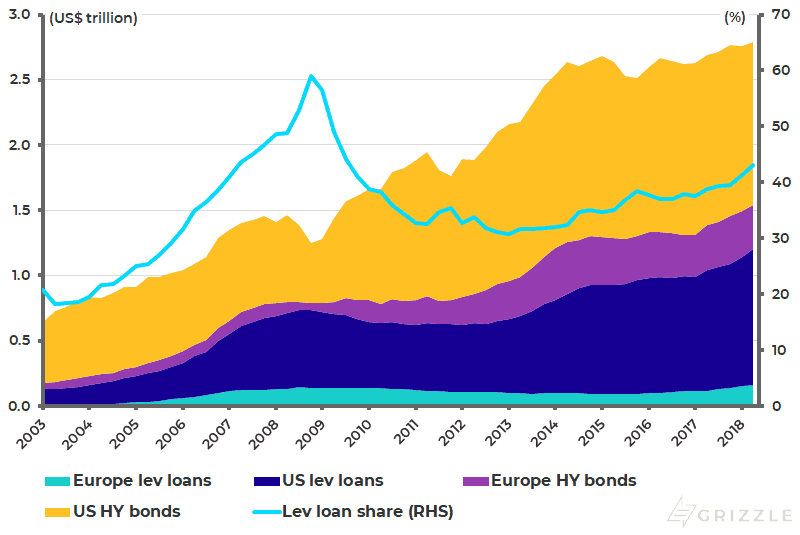

This leads to the risk highlighted by the ever-sensible Bank for International Settlements (BIS) research department in its quarterly review published in September. This is the resurgence in so-called leveraged finance, comprising high-yield bonds and leveraged loans, which has doubled in size since the financial crisis.

Total leveraged finance rose from US$1.25 trillion at the end of 2008 to US$2.79 trillion at the end of 2Q18, while within this aggregate, leveraged loans rose from US$0.62 trillion at the end of 1Q11 to US$1.2 trillion at the end of 2Q18 (see following chart). The BIS study also notes that corporate restructuring, such as mergers, acquisitions and leveraged buyouts, have accounted for nearly 40% of US institutional leveraged loan issuance since 2015.

Leverage finance outstanding

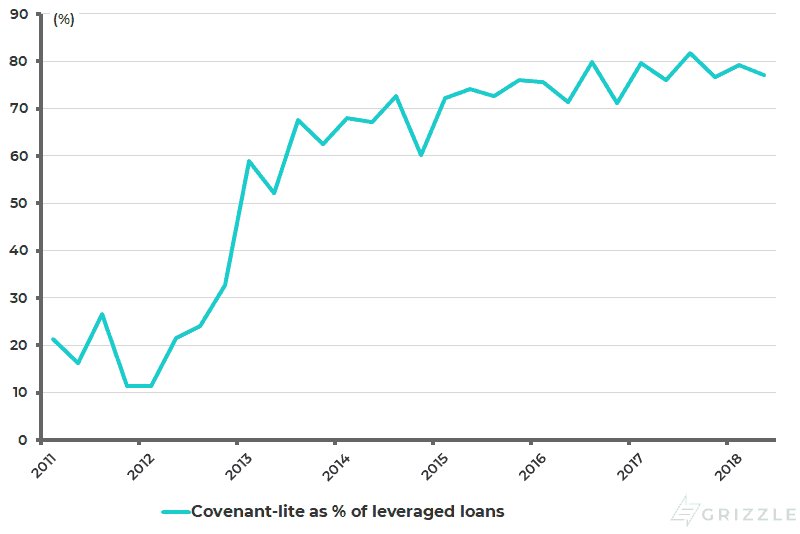

Covenant-lite loans as % of leveraged loans

Weakening Creditor Protection

A further sign of growing vulnerability is investors’ increasing willingness to accept weaker creditor protection. Thus, the fraction of so-called covenant-lite loans reached its post-GFC peak in late 2017, rising to 82% in 3Q17 and was 77% in 2Q18 (see previous chart).

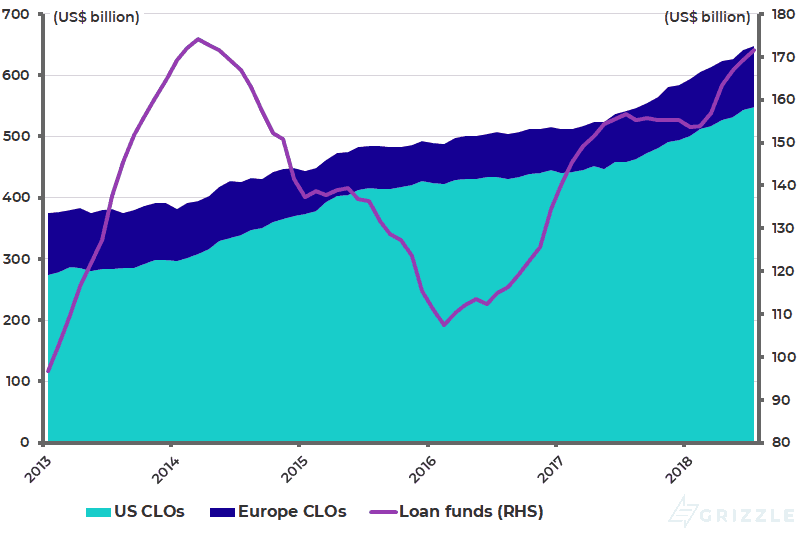

The demand for these loans has been increased by the growth in so-called loan mutual funds since 2016. Assets under management in loan funds have risen from US$107 billion in February 2016 to US$171 billion in July 2018 (see following chart). This in turn raises the risk of loan defaults and resulting mutual fund redemptions leading to forced selling.

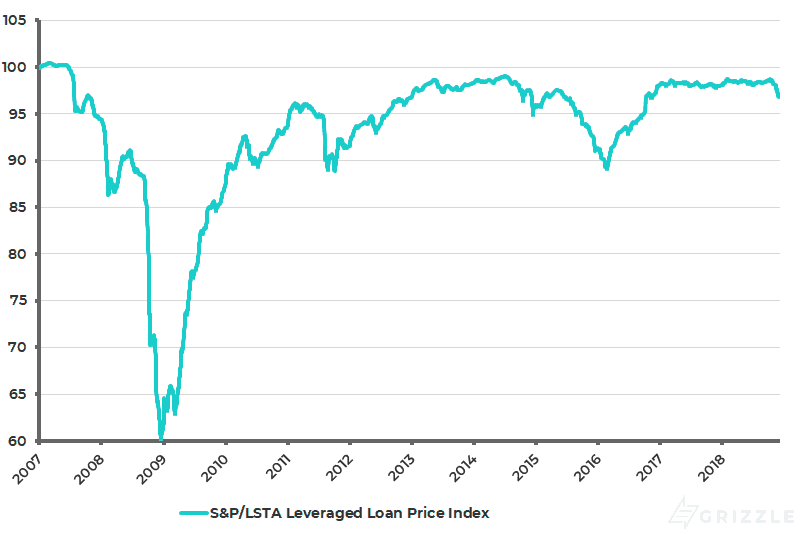

Meanwhile, the leveraged loans have been attractive in a period of rising interest rates because they offer a return indexed to the interbank rate. Still, the price of the S&P/LSTA Leveraged Loan Index has now declined to its lowest level since October 2016, though the long-term chart shows there is a lot of room for a further fall if market conditions deteriorate (see following chart).

Assets under management in collateralized loan obligations (CLOs) and loan funds

S&P/LSTA Leveraged Loan Price Index

If the above is an obvious area of vulnerability in a downturn, it should be noted that a lot of this financing has taken place outside the banking system in often opaque and complex structures. Meanwhile, ‘private equity’ will undoubtedly be remembered by financial historians as the chief beneficiary of the quantitative-easing-driven asset-inflation cycle of the past 10 years which has led to such outsized gains for the few in a period of mostly anemic growth.

This cycle began in America with private equity firms taking advantage of the housing bust to buy tens of thousands of single-family homes to rent out, an entirely sensible investment, and has since morphed into ever more complicated highly leveraged transactions. Sensible private equity groups would be advised to have already exited the game and turn to markets where there is an obvious opportunity to ‘unlock value’, namely Japan where quoted corporates still retain huge amounts of cash on their balance sheets. And this indeed is what the smart money has been doing.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.