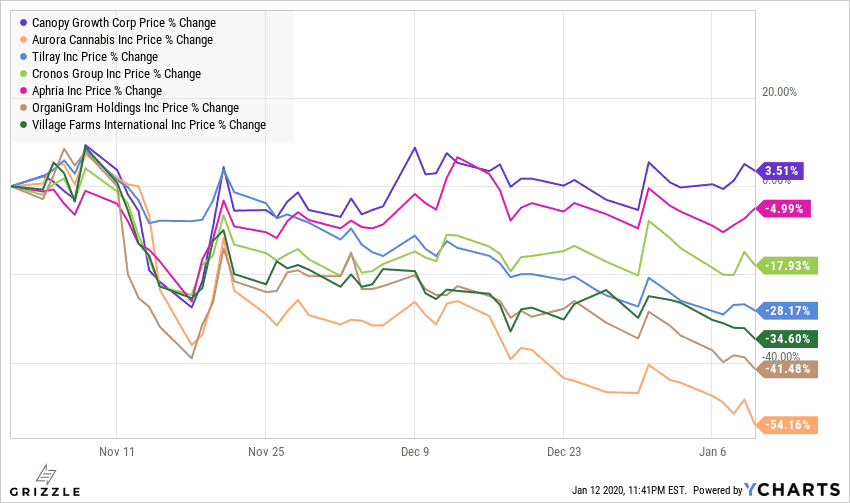

No stock has been immune to the bloodbath going on in the cannabis market, not even the largest player, Canopy Growth (NYSE: CGC; TSE: WEED).

Though Canopy’s stock is down big, it could have been much worse if it hadn’t been for the “Constellation Put”.

The “Constellation Put” is the shared view among market participants that beverage giant Constellation Brands (NYSE: STZ) will buy out Canopy, saving stockholders from suffering further losses.

This is the reason Canopy stock has been flat since a terrible earnings report, even though peers with similar results are in freefall.

Canopy stock has outperformed peers by 15%-60% since November, solely because investors expect a buyout sooner than later.

If investors dug a little deeper and put themselves in the shoes of Constellation’s management team they would quickly see their blind belief is completely misguided.

In the following report, we lay out why Constellation is most definitely not buying Canopy Growth and what Canopy is worth without the Constellation buyout premium.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Bottom Line: Canopy will have to raise more money before it turns a profit and will further disappoint earnings expectations in the process.

A flat stock price for the next two and a half years is the best-case scenario in our view. The stock is still expensive at US$20.00/$C26.00 and would have to fall 50% to US$10.00/C$13.00 to be fairly valued.

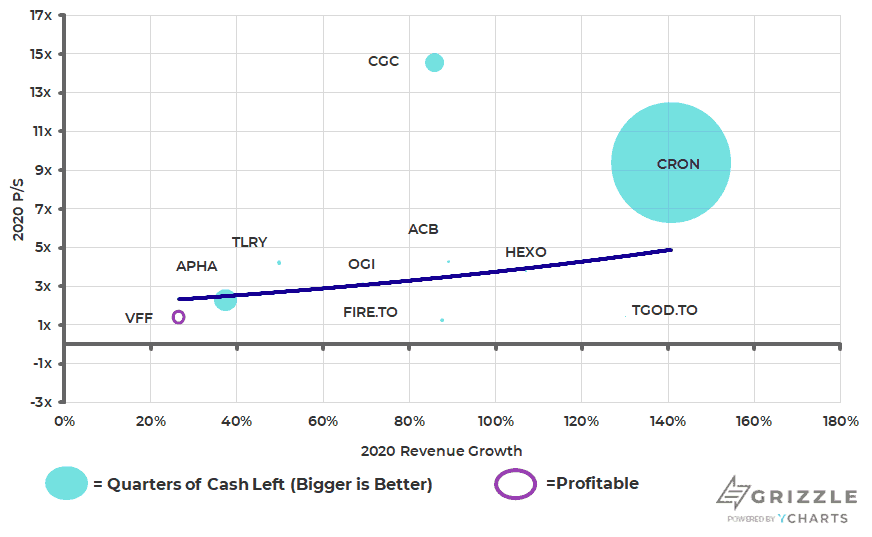

[/su_panel]Canopy Way too Expensive vs Cannabis Peers

Canopy Stock Supported by Constellation Buyout Rumours

All the Reasons Constellation is Not Buying Canopy Growth

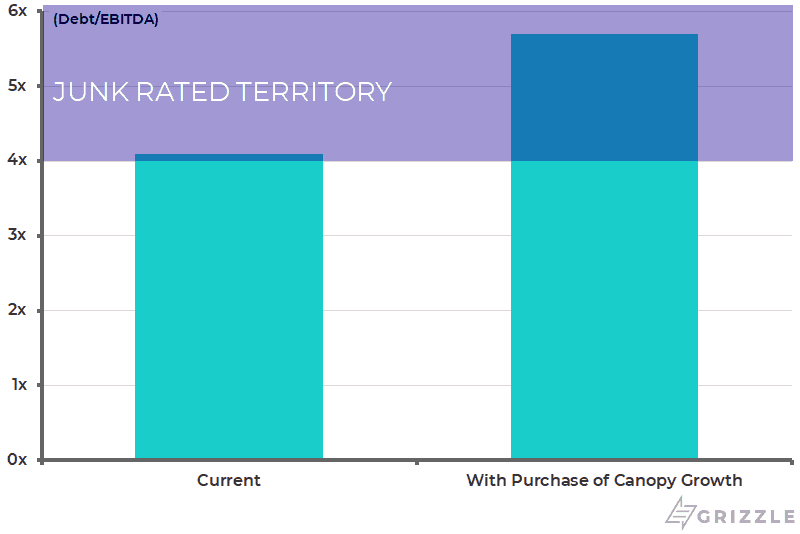

#1: Buying Canopy Would Drive Constellation’s Debt Rating to High-Yield

Quote 1

Quote 2

Constellation management has made strongly-worded promises to investors that they are serious about cutting down on debt.

Constellation has one of the highest leverage ratios in the large-cap beverage industry and the debt rating is dangerously close to being cut to high-yield.

Constellation is already on super secret probation with rating agency Moody’s who has threatened to downgrade the company to junk status if debt to cashflow doesn’t fall below 4x by October of 2020 from 5.2x today.

Even if Constellation uses cash from a pending asset sale to pay off some of this debt, the ratio will still be above 4x.

A purchase of Canopy Growth, even at the current price would cause debt to cashflow to spike to ~6x and Constellation will become a junk-rated borrower.

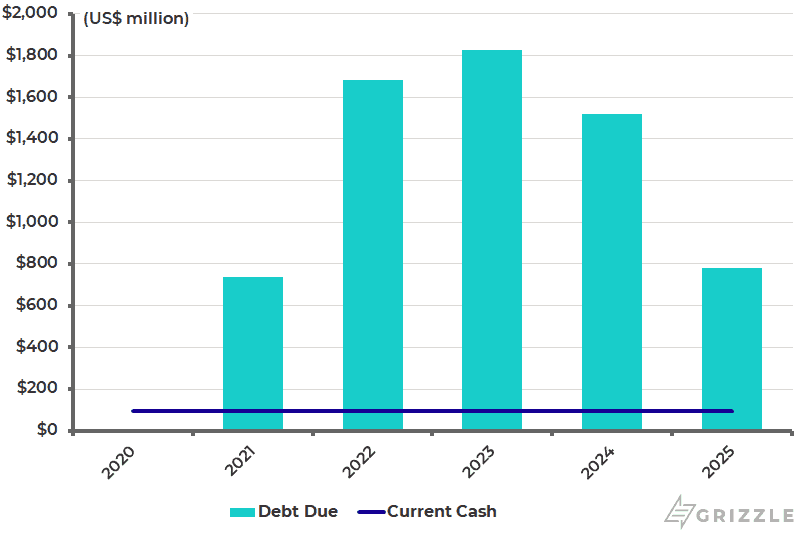

Constellation Debt Rating Cut to Junk if it Buys Canopy Growth

If cut to high-yield Constellation would be cut off from borrowing in the commercial paper markets and will lose access to a portion of the $1.15 billion revolving credit facility, not to mention the restrictions on selling more assets and the higher interest they will have to pay as a riskier borrower.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Constellation can’t afford to pay back $280 million of commercial paper and lose partial access to a billion-dollar credit line when cash is only $94 million and they are on the hook to pay back $730 million of debt this year. Management really, really doesn’t want to lose that investment-grade credit rating.[/su_panel]Available Cash Not Enough to Cover Debt Due This Year (2021 in the chart)

#2: Constellation Has Promised Big Cash Payouts. Buying Canopy Would Make These Payouts Impossible

Constellation’s stock has rebounded 16% this year mostly on the back of aggressive promises about increased shareholder payouts.

Management says they will pay out $4.5 billion of cash to shareholders through dividends and buybacks over the next 30 months.

A $4.5 billion payout is currently achievable, but if the company buys Canopy Growth there is no way they can live up to this commitment.

Canopy is spending USD$1.3 billion a year on growth not to mention another USD$600 million for acquisitions in the last six months alone.

Even if we assume no more spending on acquisitions, Constellation’s free cash flow after dividends would completely disappear if they buy out Canopy compared to $981 million with no deal.

That promise to return $4.5 billion to shareholders will have to turn into a promise to return only $1.8 billion to shareholders, a 60% drop.

Stockholders will not be happy.

Cash Left Over for Buybacks if Constellation Buys Canopy

| USD$Millions | Year Ending Feb 2020 |

(+) Canopy Growth |

| Free Cash Flow | $1,550 | $529 |

| (-)Dividends | $569 | $569 |

| Leftover for Buybacks | $981 | ($40) |

Source: Grizzle Estimates, SEC.GOV

#3: Constellation is Telling Shareholders it Won’t Put Another Dollar into Canopy Until November 2023

Just yesterday the Chief Financial Officer (CFO) told the analyst community that Constellation has no plans to put another dollar into Canopy Growth except to exercise warrants that are in the money.

The warrants that expire in 2020 will only increase Constellation’s ownership by 5%.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Looking past the 2020 warrants, the only warrants remaining don’t expire until four years from now and are 50% out of the money. Canopy won’t see more than $250 million from Constellation for the next 3-4 years.[/su_panel]With both the current CEO and outgoing CFO saying they are committed to an outcome that does not include a Canopy buyout in it, we think it’s safe to say investors are on their own.

There is no reasonable price Canopy could fall to that would allow Constellation to buy the company without having their credit rating cut to junk.

No Constellation buyout is coming.

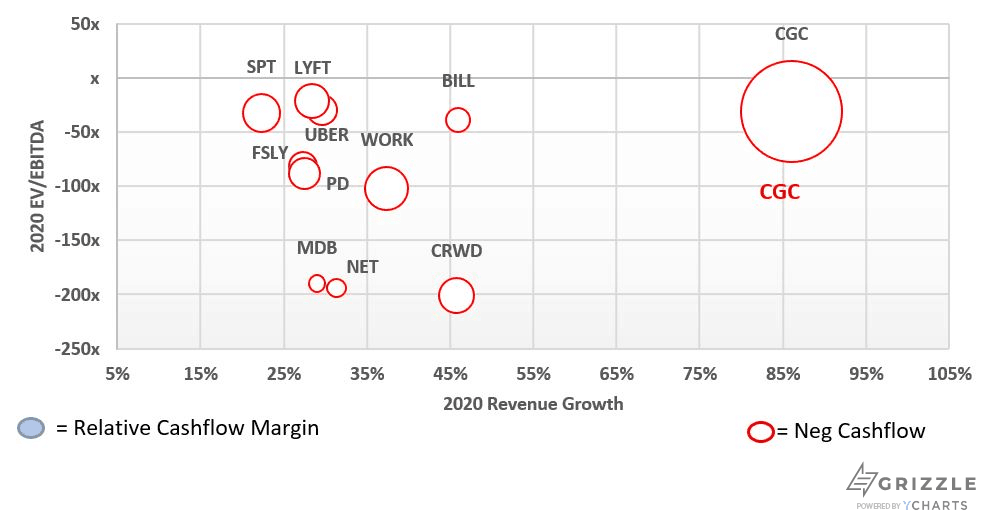

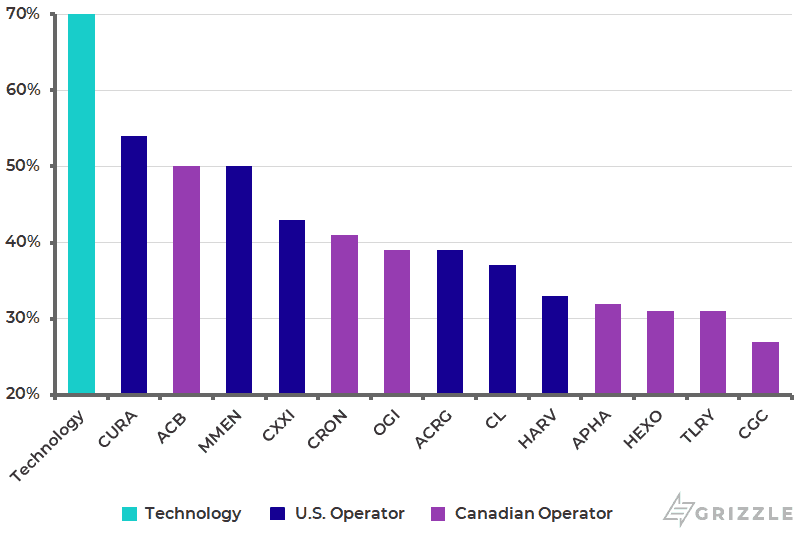

Canopy is Priced Like a Tech Stock Without the Tech

Canopy’s financials should look similar to the beverage or pharmaceutical industries longer term.

But today, the market is still pricing the company like it’s a tech stock and this creates risks for investors.

Canopy will not be able to meet both growth and profitability expectations in our view.

Earnings results will continue to disappoint and with the Constellation buyout premium removed, the stock will be going lower.

Canopy Not Priced Like a Beverage Company

Not Priced Like a Big Pharma Company

Canopy is being priced like a tech company even though the cannabis business shares no similarities with the tech industry besides rapid growth.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]The market is giving Canopy full credit for its rapid growth and also assuming margins are going to end up at attractive levels even though no one has any idea how profitable legal cannabis will ultimately be. [/su_panel]Priced Like a Tech Stock With None of the Tech

Canopy is currently a cultivation company and someday if it’s lucky will become a consumer packaged goods company.

A tech company it is not.

Gross margins, a measure of how profitable the underlying business is before we include corporate costs, are just one way we can see the Cannabis business is different than the tech business.

Gross margins in the tech sector are 70%-90%

Cannabis Is Not Tech (Gross Margins)

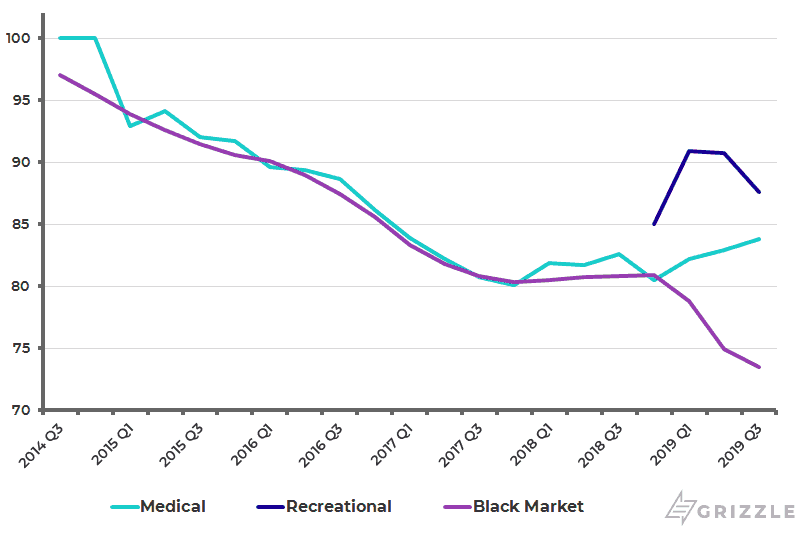

Looking at the cannabis industry, gross margins are already half of what a tech company generates, not to mention we know legal prices are falling due to an acute cannabis oversupply, putting further pressure on margins across the industry.

Prices Under Pressure from Oversupply of Cannabis (2012=100)

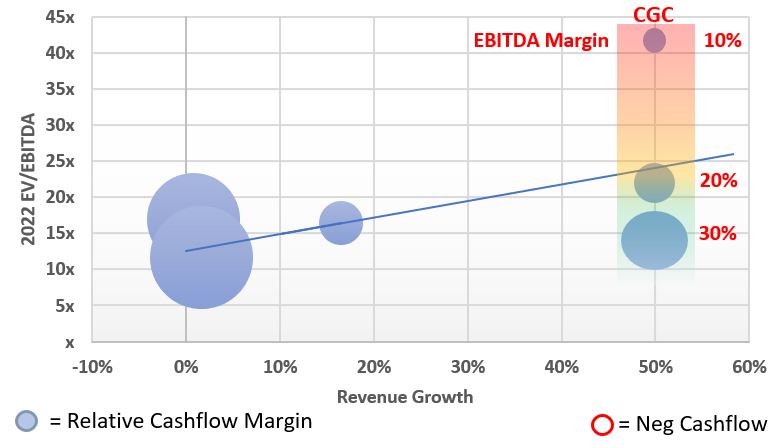

Looking at Canopy’s valuation another way, if the stock price goes nowhere for the next three years, the stock will still be overpriced against beer and liquor peers.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Canopy has to grow revenue 76% a year for the next three years and reach an EBITDA margin of 20% from -30% today for the stock just to stay at $20.00/C$27.00 per share. Not exactly a rosy outlook.[/su_panel]Potential Multiple of Canopy Three Years From Now (2022)

All the Reasons Canopy’s Stock Price is Going Lower

#1: Analysts Expectations Are Still Too High

Analysts still expect blistering revenue growth and a growing market share of Canadian sales.

In real life, early entrants almost always lose market share as competition intensifies before industry sales eventually end up in the hands of a few large winners.

Betting that this time is different is not a winning strategy.

On the revenue front, analysts expect annual revenue growth of 87% meaning Canopy would go from USD$300 million in the last twelve months to USD$1.1 billion by 2022.

Either falling retail prices or a refocusing on profits over growth would cause results to miss estimates, dragging the stock down further.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Analyst revenue estimates assume a doubling of the Canadian market every year, a 5% increase in Canopy’s market share to 30% from 25% and stable industry prices. With competition increasing and an oversupply pushing down prices, betting on all three outcomes at once is truly foolish.[/su_panel]#2: The New CEO will Focus on Profits not Revenue Growth

The new CEO, a veteran of Constellation Brands and that company’s previous chief financial officer, is being brought in to cut costs and generate some profits.

As any business major knows, when you focus on profits, you aren’t spending on growth.

It’s highly likely in our view that in 2020 the new CEO sacrifices growth in the pursuit of profits, causing Canopy to miss revenue estimates while still losing money.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Profitability is crucial longer-term, but if you take growth out of the equation cannabis becomes an industry with worse margins than tech and slower growth. Why would any big-money investors bother moving money into cannabis when better risk-adjusted returns can be found elsewhere? [/su_panel]#3: Share Count Will Be on the Rise to Fund the Cash Burn

There is one place where we are in agreement with the market.

Canopy will run out of money before management is able to turn a profit.

However, estimates are far too rosy even on this front.

Analysts expect Canopy to only burn another C$500 million in cashflow by mid-2022 even though current spending implies a C$2.2 billion deficit.

We also need to add in capital spending which would consume another C$2.5 billion by mid-2022 for a grand total of C$4.7 billion of cash spent before a dollar of profit is generated.

This C$4.7 billion deficit doesn’t even include any more purchases of other companies or the cash burn if Canopy closes the purchase of U.S. operator Acreage and has to pay for that company’s growth.

Burning C$4.7 billion of cash for a company only worth C$9 billion is really something.

If Canopy had to fund a C$4.7 billion cash hole they would issue 72 million more shares after burning through the cash balance, a 20% increase.

Both the expectation and the reality of more shares or dilutive convertible debt hitting the market will put pressure on Canopy’s stock price over the next two and a half years.

Canopy shareholders are stuck holding a deeply unprofitable company that is already priced for a big turnaround.

Even if everything goes right, the stock price is merely where it should be.

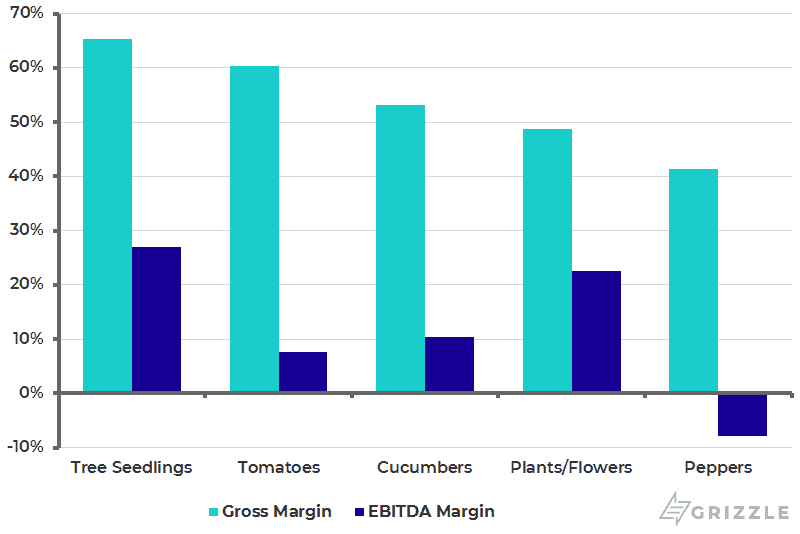

#4: Margins in a Maturing Cannabis Market Are Unknown

The industry arbitrarily came up with 30% as a guidepost for where cashflow, also called EBITDA, margins may ultimately end up.

We can’t find any research justifying why this number has been used in investor decks and by management teams when talking to investors.

Our best guess is the industry took the margins of traditional produce growers and tripled them.

Ultimately we think cashflow margins will fall somewhere between 10%-30%, but until the industry oversupply is dealt with, results will be much worse.

Margins for produce growers currently vary between a loss for growing peppers in Alberta to a 22% margin for growing flowers.

EBITDA Margins for Growing Produce and Flowers

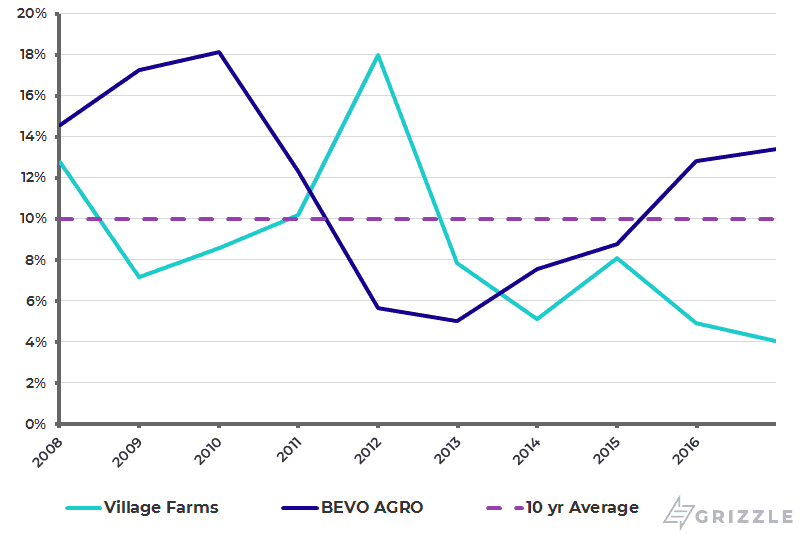

Just to make sure the industry margins were in line with those of individual companies we looked at the cashflow margins for two of Canada’s oldest greenhouse growers, Bevo Agro and Village Farms.

These companies have been public for more than a decade proving they are two of the most successful greenhouse operators in Canada.

With a 10-year average EBITDA margin of 10%, their results support the other industry margin data we collected and displayed above.

We think cannabis margins will look similar to selling flowers.

Flowers are perishable and usually a time-sensitive and impulse purchase allowing sellers to charge a premium.

If cannabis ultimately generates EBITDA margins of 20%, in line with growing flowers, the industry ultimately has to take another leg down before finding a bottom.

10 Years of EBITDA Margins for Bevo Agro and Village Farms

The Next Year Will Not be Kind to Canopy Growth

Canopy Growth stock is hanging on for dear life and the only thing propping it up is a rumoured acquisition by Constellation Brands.

We have debunked that rumour and pointed out all the negative catalysts coming in the future that will chip away at Canopy’s US$20 stock price.

As we have recommended with other cannabis stocks, better to invest in technology and wait for some serious industry headwinds to blow over before diving back in for the multi-year rebound.

One by one the potstock dominos are falling and Canopy is next.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.