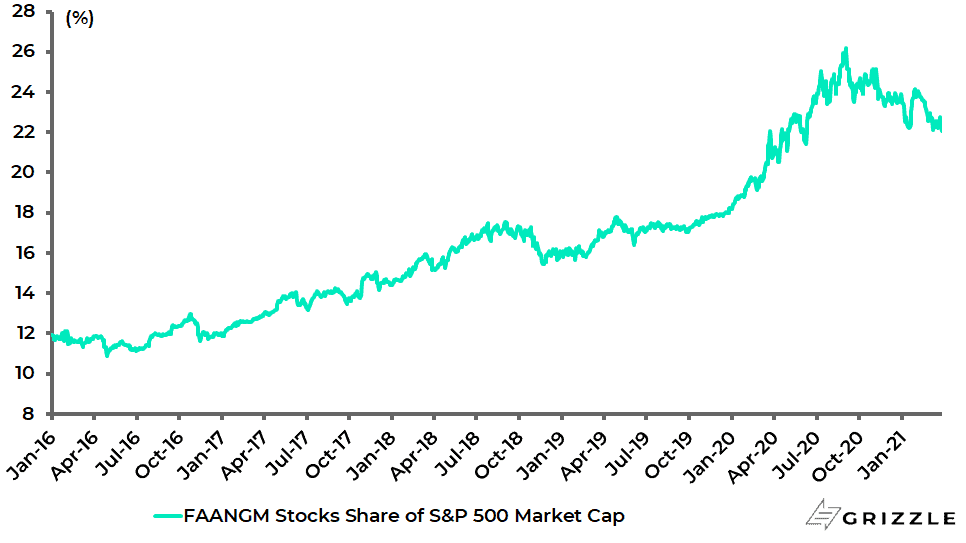

The view here remains that the Big Tech stocks’ market capitalisation peaked as a percentage of the S&P500 at the peak level of 26.2% reached last September.

US Big Tech’s Share of S&P500 Market Cap

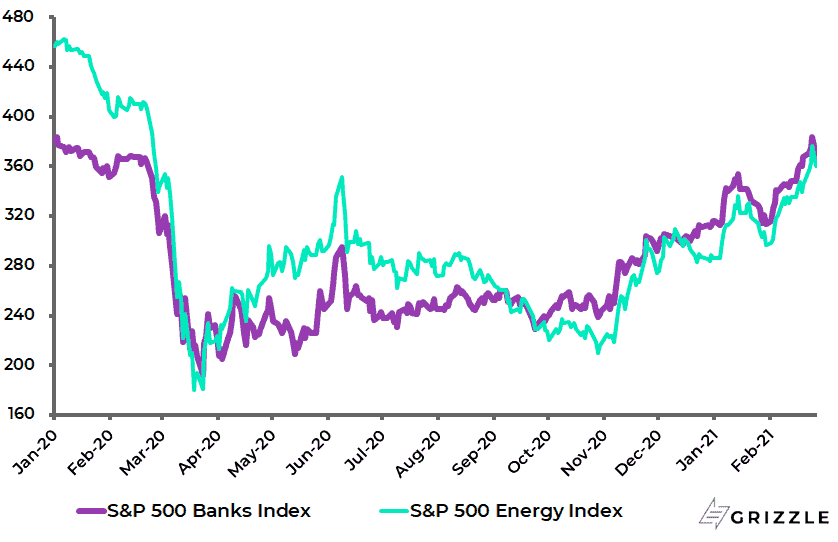

One reason for this view was the anticipated rotation into cyclical stocks on the back to normal trade with the S&P500 banks index and energy index up by 55% and 44% since then.

S&P500 Banks Index and Energy Index

But another reason is the anticipation of significant regulation of US Big Tech in the next five years despite the extremely close relations between Silicon Valley and the Democratic Party establishment.

Big Tech Regulation is Still Coming

Indeed regulation of Big Tech is one of the few areas of policy where the progressive wing of the Democratic Party and the right-wing of the Republican Party can probably work together.

This was on display in the tough questioning, from both sides of the aisle, of tech executives in the House of Representatives last week.

There are already plenty of initiatives underway to rein in Big Tech.

In December the US Federal Trade Commission accused Facebook of unfair competition and asked a federal court to break it up.

Just because the stock market did not react so negatively to this news, with Facebook declining by only 1.9% on the day the announcement was made, does not mean it is not important.

Then also in mid-December, the European Union proposed sweeping new rules forcing Big Tech to take more responsibility for policing content on websites and to refrain from anti-competitive practices or face break-up threats.

Facebook vs Australia

Still, perhaps the most interesting initiative against Big Tech of late has occurred Down Under.

This is a reference to Facebook’s initial response last month to groundbreaking legislation in Australia that would effectively compel the social media giant and other “platforms” to pay for traditional media content.

For Facebook’s response was to impose a news blackout of both local and international media in Australia as well as, in a public relations disaster, also “inadvertently” to remove the pages of some Australian government agencies.

By contrast, Google, which also opposed the proposed legislation, agreed to pay media companies for content (see The Wall Street Journal article: “Facebook’s Australia Blackout Criticized”, 20 February 2021).

That Facebook subsequently reversed its stance and announced an agreement with the Australian Government reflects belated recognition of the PR own goal.

One of the agreed amendments to the so-called media bargaining code was that the Australian government will consider whether a digital platform has made a “significant contribution to the sustainability of the Australian news industry through reaching commercial agreements with news media businesses” when deciding whether to apply the code.

The amended legislation was then passed on 25 February.

As a former print journalist, this writer may be more interested in the above than most because of the way both Facebook and Google have destroyed the economics of traditional media with the two companies accounting for about 60% of digital advertising revenues in America by their exploitation of surveillance capitalism, a business model which regulators are, belatedly, finally focusing on.

Still, the media companies only have themselves to blame because they should never have allowed their news content to be shown on the platforms’ “news feeds” free of charge in the first place.

In their desperate search for “eyeballs” they gave away free their prime asset, namely content.

Can You Trust Facebook’s Metrics?

Still, while the Australian situation made headlines for good reason, another interesting development concerning Facebook occurred last month in terms of claims made in unsealed documents in a California court which this writer only became aware of by reading the attached online newsletter (see BIG newsletter – “Facecrook: Dealing with a Global Menace”, 20 February 2021 by Matt Stoller).

The court documents focus on the alleged practice by Facebook of telling advertisers that their ads reach more people than they actually do.

One example cited is that Facebook told advertisers in 2018 that it had a potential reach of 100m 18 to 34 years old in America even though there were then only 76m people in that age cohort.

In a further development on a related issue, in the last quarter of 2020 Facebook reported that it disabled 1.3bn so-called fake accounts.

This is an amount equal to almost half its active users.

Yet, as noted by the Financial Times in a Lex column article on 24 March (Facebook: billion-dollar bots, 24 March 2021), user accounts are the basis for advertising sales that make up almost all Facebook’s revenues.

Facebook Ad Revenue Not Yet Taking a Hit

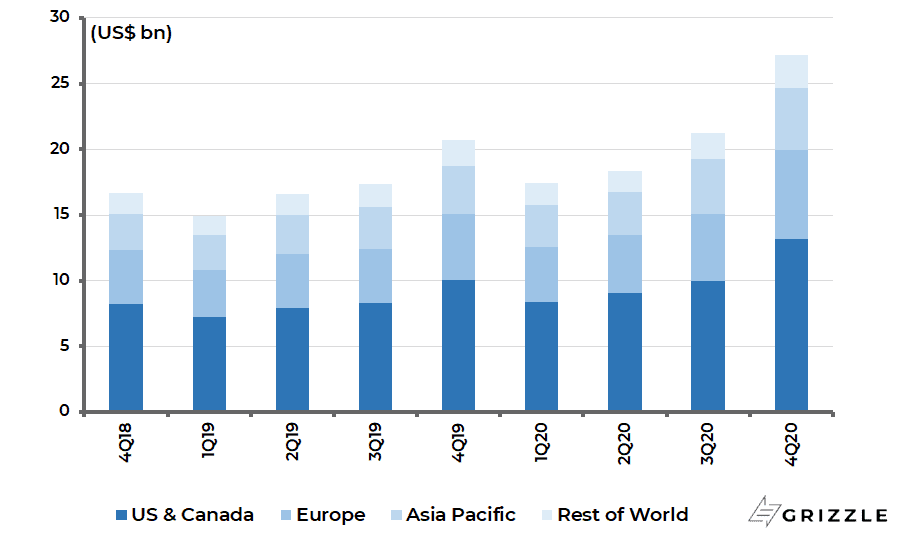

Meanwhile, it will be interesting to see the impact of recent events on the number of Facebook users in Australia, though that is clearly only a tiny percentage of its global reach.

Facebook Daily Active Users by Region

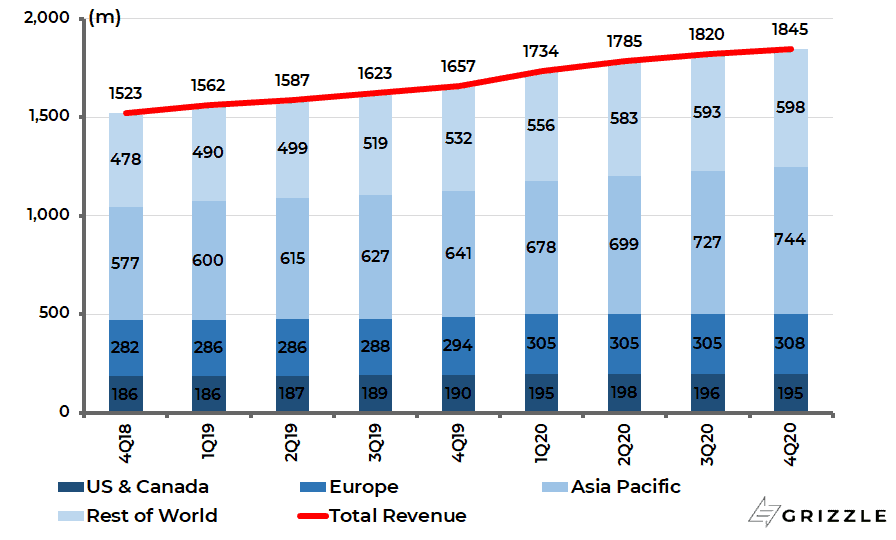

More importantly, from an investment standpoint, Facebook’s user base has been more or less flat in America and Europe for the past four quarters though, interestingly, advertising revenues have not yet been hit.

Facebook Advertising Revenue by Use Geography

Certainly, Facebook has long ceased to be “cool” to teenagers, as also reflected in the rising revenues and users of Snap Inc, the developer of Snapchat.

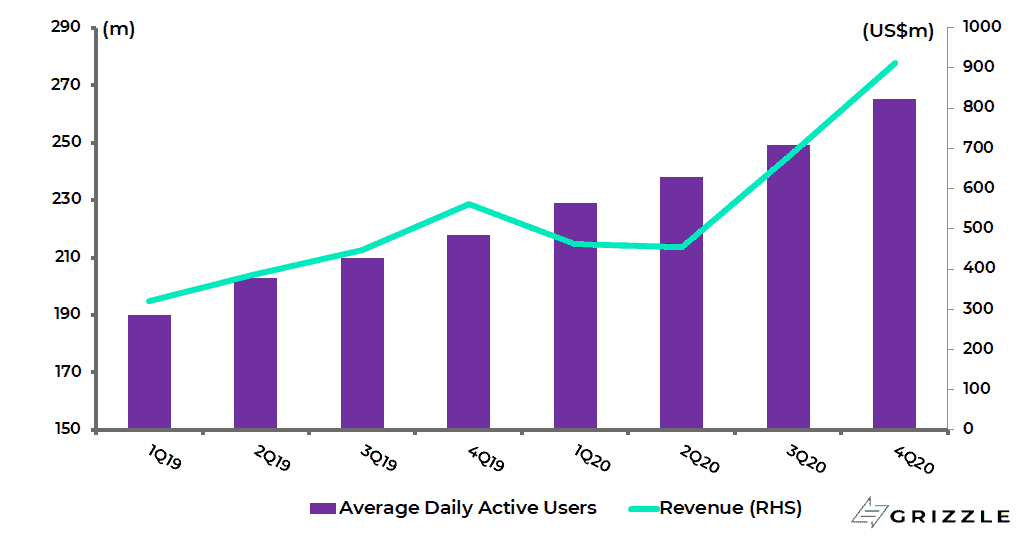

Snap’s revenue rose by 62% YoY to US$911m in 4Q20 and was up 46% YoY to US$2.5bn in 2020, while the number of average daily active users rose by 22% YoY to 265m in 4Q20.

Snap Inc. Quarterly Revenue and Average Daily Active Users

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.