Stock market action remains “risk on” as the base case remains a deal on trade between the U.S. and China, though the implication of America’s increasingly aggressive moves towards China’s Huawei highlights the long-term threat to the Sino-American relationship.

This is a reference less to the arrest of the unfortunate Huawei CFO Meng Wanzhou on Dec. 1 but to the U.S. Justice Department’s criminal charges against Huawei for theft of intellectual property, and the related campaign to persuade allies not to adopt Huawei’s 5G technology.

Who Will Cave to American Pressure on Huawei?

So far Australia and New Zealand have agreed not to go with Huawei, while Canada is reportedly considering such a ban. Reservations have been expressed by both Britain and Germany. See, for example, Financial Times article “Huawei’s green light from Britain dents US drive for global 5G ban”, Feb. 18.

It will be interesting to see how many countries cave into the American pressure. So far most of them have shared the distinguishing feature of being “white”. This raises the point that American pressure is on course for putting Asian governments in a position none of them want to be in. That is to be forced to choose between America or China, which is why they will seek to avoid making that choice, for as long as possible.

The Clash of Empires

I have no idea whether Huawei is guilty of the charges levelled against it. But it would seem the main driver for Washington is the sudden concern that a digital industry standard for 5G was about to be set by a country outside the American orbit.

With talk of strategic rivalry and the “clash of empires” now increasingly fashionable among the chattering classes, it is not necessary to subscribe to the theories of famous radical MIT political scientist, Noam Chomsky, to agree that there is a lot of historical evidence that American political culture requires that it always needs an external enemy.

If the above poses the long-term risk in terms of the US-China relationship, it remains the view here that Donald Trump is definitely not one of Washington’s natural security zealots, and that he will still want to do a deal with China on both trade and North Korea. Remember a summit is meant to be held with the North Korean leader Kim Jong-un in Hanoi this coming week on Febr. 27-28.

So long as both sides are talking, as has been the case this past week in Washington as regards the ongoing US-China trade talks, that hope should be maintained. But for a deal to happen the Donald will probably have to meet China President Xi Jinping.

The Biggest Risk

Probably the biggest risk to the above base case is that some development happens internally in America, for example, concrete developments from the ongoing Mueller investigation, that undermines Trump’s political position domestically in a way that fatally compromises his position to do a deal with Beijing. This would be a major negative since the world economy will be a lot better off if a trade deal is agreed and the existing tariffs are dropped.

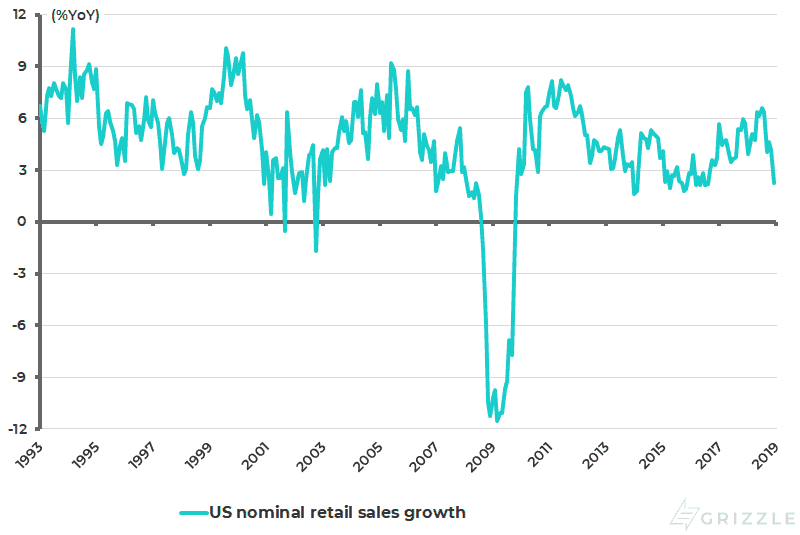

As for the state of the American economy, the anticipated slowdown after the surge triggered by last year’s tax reform has been clearly signalled by the significant flattening of the yield curve that took place last year. And one sign of such a slowdown was the latest U.S. retail sales data. Thus, U.S. retail sales declined by 1.2%MoM in December and were up only 2.3%YoY, down from 4.1%YoY in November and the slowest year-on-year growth rate since August 2016 (see following chart).

U.S. Nominal Retail Sales Growth

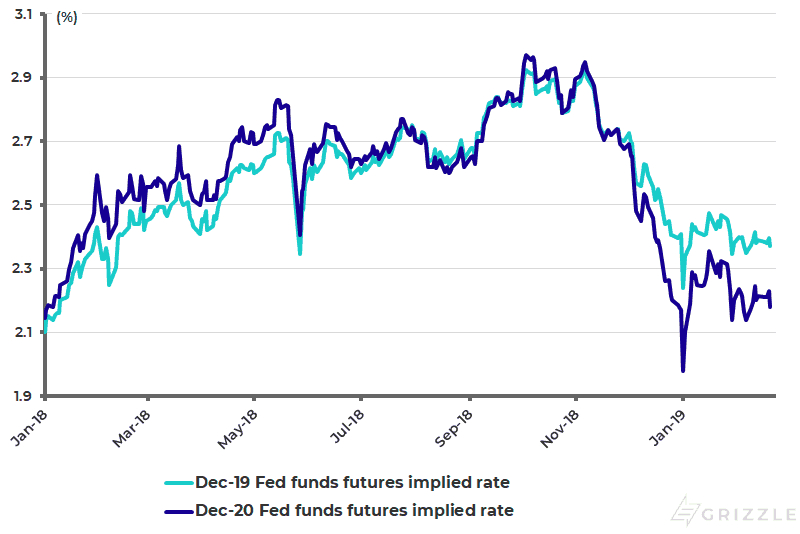

Federal Reserve Jerome Powell has now all but acknowledged that the monetary tightening cycle could be ending with his “Powell pivot” at the FOMC meeting in late January. As a result, the Fed funds futures market is now discounting no rate hike in 2019 and a 25bp rate cut in 2020. This is very different from what was discounted as recently as early November, when the Fed funds futures were discounting a 50bp rate hike in 2019 and no rate cut in 2020 (see following chart).

Fed Funds Futures Implied Rates

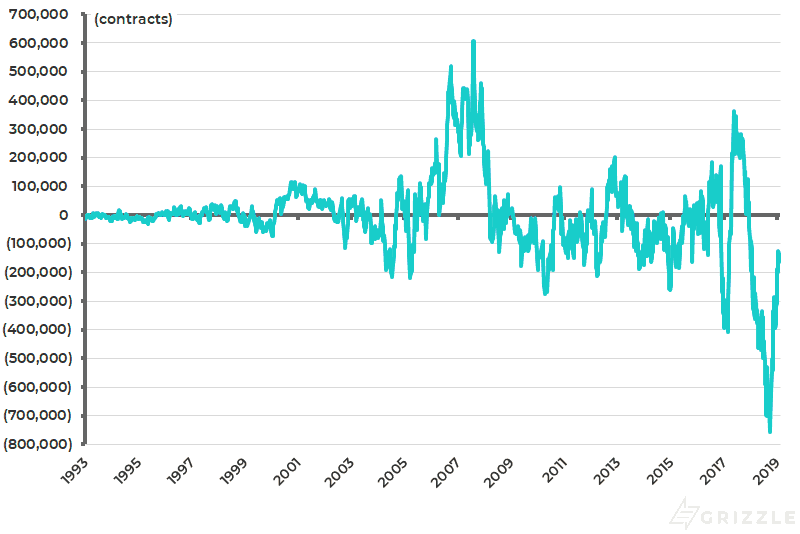

With such a change in market perceptions, there is clearly a risk that a sudden re-acceleration of economic activity triggers renewed tightening concerns. It is interesting from this point of view that investor positioning does not suggest such complacency. In this respect, the end of the federal government shutdown means that investor positioning data has begun to re-appear, albeit only up to the week ended Feb. 5.

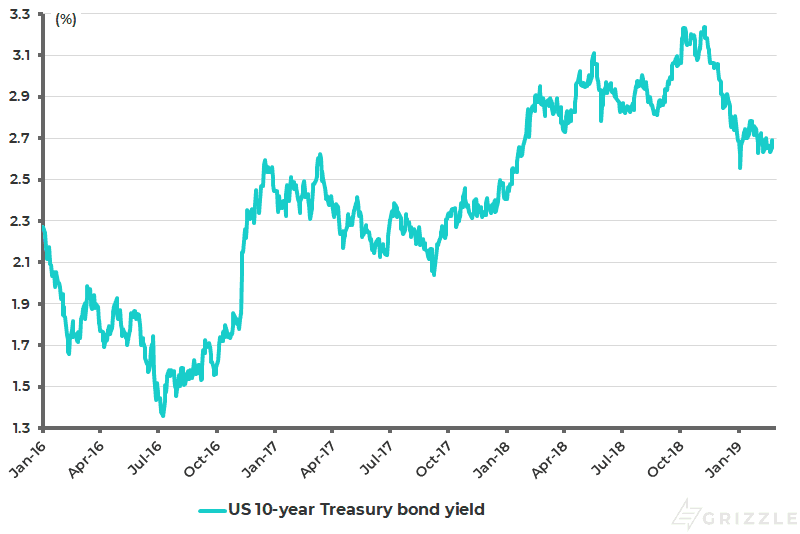

The most interesting point is that investors are still net short U.S. Treasury bonds, even though the “shorts” are well down from the peak level reached in September 2018. Thus, the U.S. 10-year Treasury bond futures’ net speculative short positions peaked at 756,316 contracts in September 2018 and have since declined to 162,950 contracts in the week ended Feb. 5 (see following chart). The continuing “shorts” are despite the significant bond rally since early October 2018 when the ten-year yield peaked at 3.26% (see following chart).

CFTC US 10-year Treasury Note Futures Net Speculative Positions

US 10-year Treasury Bond Yield

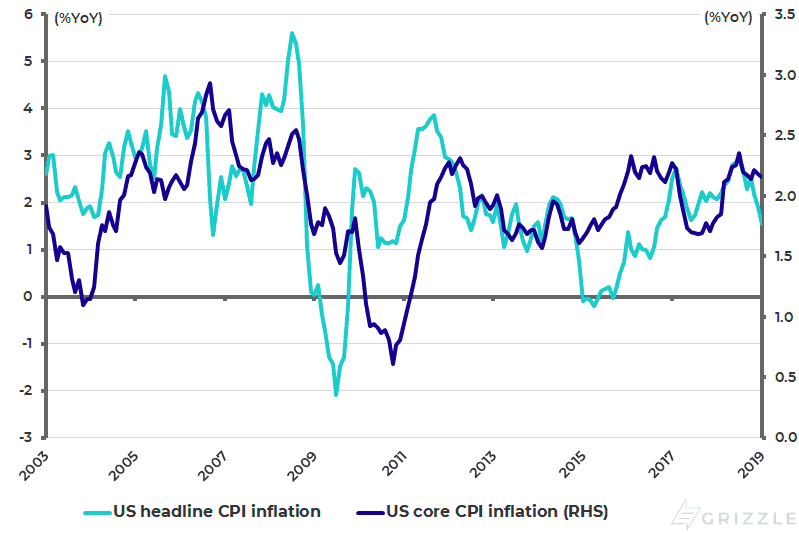

The latest U.S. inflation data released has not upset the bond market. Core CPI inflation remains unchanged at 2.2% YoY in January, while headline CPI inflation slowed from 1.9% YoY in December to 1.6% YoY, the slowest since September 2016. Core CPI inflation remains below the recent high of 2.4% YoY reached in July 2018 (see following chart).

US CPI inflation

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.