Roku (NASDAQ: ROKU) reported Q4 2019 earnings, beating analyst expectations as the company benefits from the streaming wars.

Sales for the online media player company were $411.2 million, topping consensus estimates of $392.6 million. Revenues overall were up 49% over the same period the previous year, lead by sales from the company’s platform revenue segment which was up 71% year over year.

Roku has been a beneficiary of the increased competition in media streaming as it receives a cut of streaming services monthly fees when users signup to a service through the Roku platform. So the launch of both Disney+ and Apple TV during the quarter was expected to be a tailwind for the company’s sales.

While revenues have been surging, the company was [also able to/unable to] grow gross margins which came in at 62.5% for the quarter which were down 0.1% over the previous quarter and down 7.4% year over year.

Overall, Roku is still losing money however, reporting a loss of $0.13 per share which was exactly what Wall Street analysts expected.

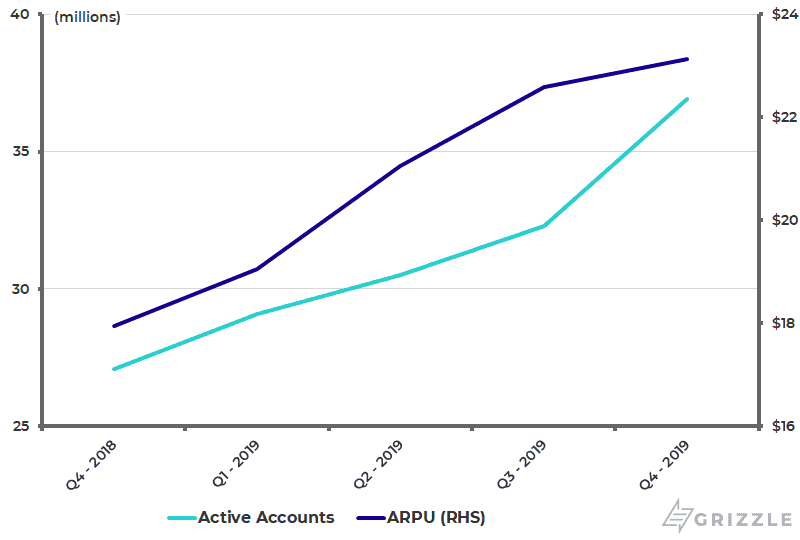

Two important metric for the company are the number of active accounts and the average revenue per user (ARPU). In the earnings release Roku reported the number of active accounts grew to 36.9 million, up 36% year over year and ARPU of $23.14, up 29% year over year.

The company also provided their outlook for fiscal 2020, indicating they expect revenues of $1.6 billion for the year representing a 42% increase year over year with adjusted EBITDA breakeven. Analyst expectations for the firm for fiscal 2020 were $1.56 billion in sales on EBITDA of $65 million.

Roku’s stock was one of the top performers of 2019, gaining a whopping 337% over the year and while the stock has had a bumpier ride in 2020 thus far it has still added a little under 5% year to date. In after market trading after releasing earning the stock was up 7% as of the time of publishing.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.