The Boston Beer Company, Inc. (NYSE: SAM) reported its second quarter fiscal 2020 results ended in June after market today that exceeded analyst expectations, causing shares to trade higher post market.

The company generated $481.09M of revenue, above analyst estimate of $421.4M by 14.2%, and up by 42.1% year over year.

Earnings per share exceeded street consensus of $2.42, by 101.8% at $4.88.

The company’s EBITDA at $74.57M also beat analyst estimate of $59M by 26.4%, however its EBITDA margin was lower than last fiscal year’s second quarter by 18.3%.

The lower year-over-year (YOY) EBITDA margin was due to the company incurring higher production costs, as it transferred most of its operations to third party breweries due to COVID-19 related safety measures.

Increases in advertising expense and salaries and benefits costs also contributed to lower YOY EBITDA margins.

Valuation Breakdown

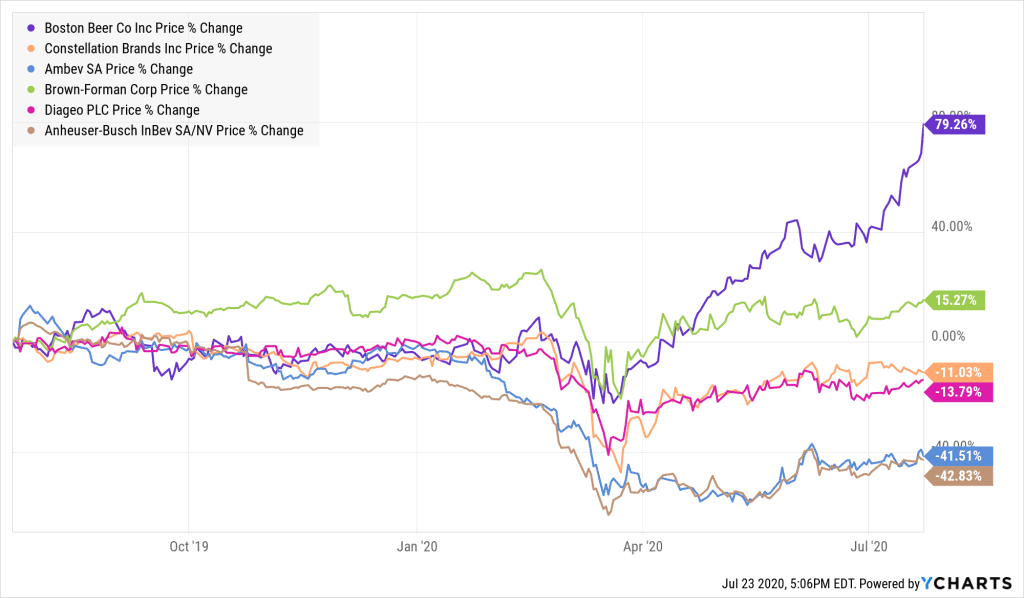

The rise of alcohol usage during the lockdown has benefited the shares of The Boston Beer Company (B.B.C.) the most since the march lows.

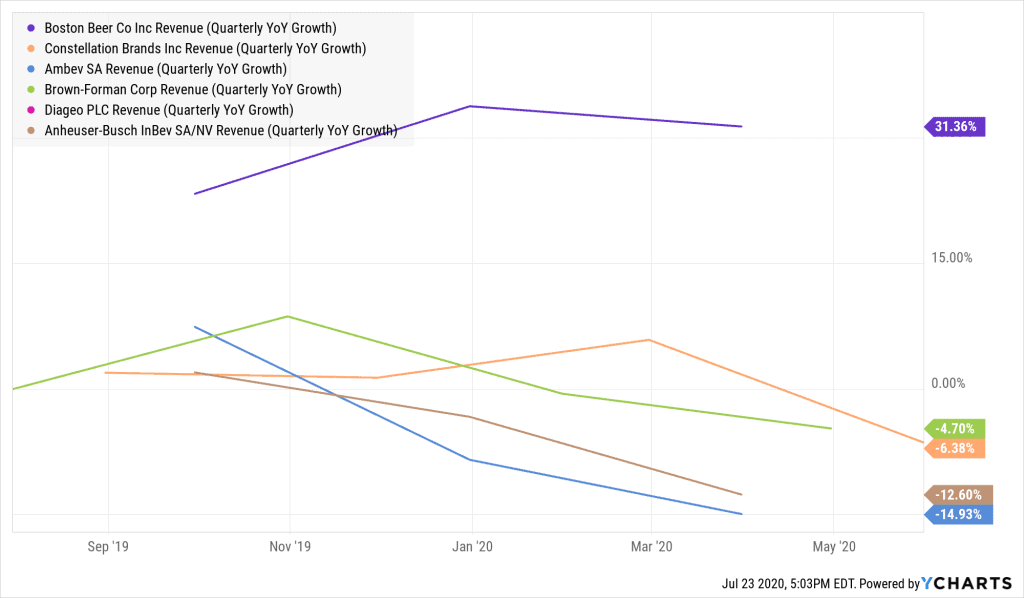

This tremendous outperformance is justifiable when considering the fact that B.B.C.’s quarterly revenue growth has remained relatively strong compared to their prominent competitors.

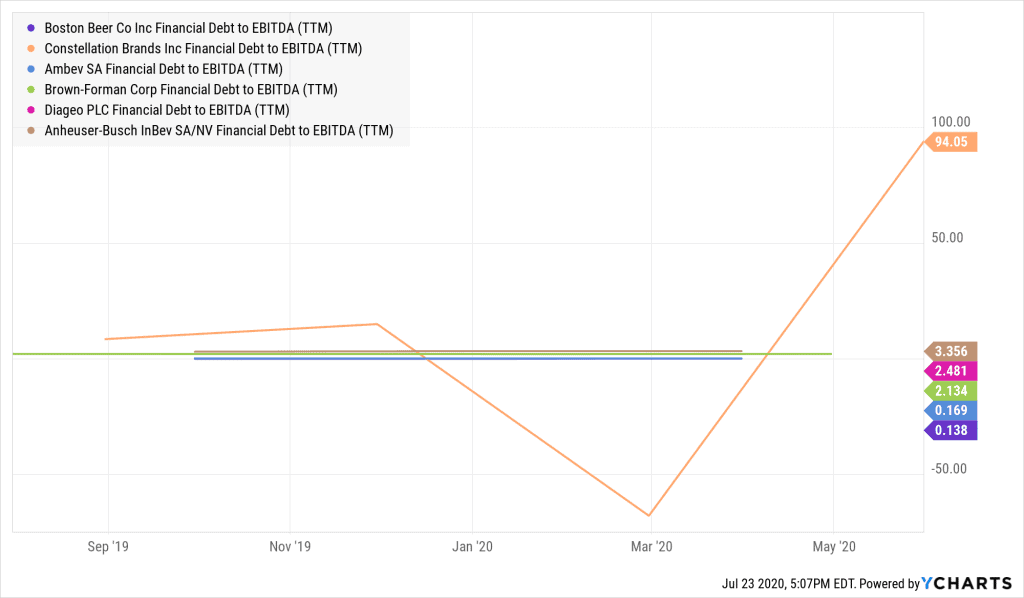

Additionally, with little to no debt recorded on their balance sheet, and cash and cash equivalents buffer of $86.7M, the company also enjoys a strong financial position too.

This is a far cry from Constellation Brand’s leverage situation, which according to the following chart their Debt to EBITDA ratio is 94.05 times!

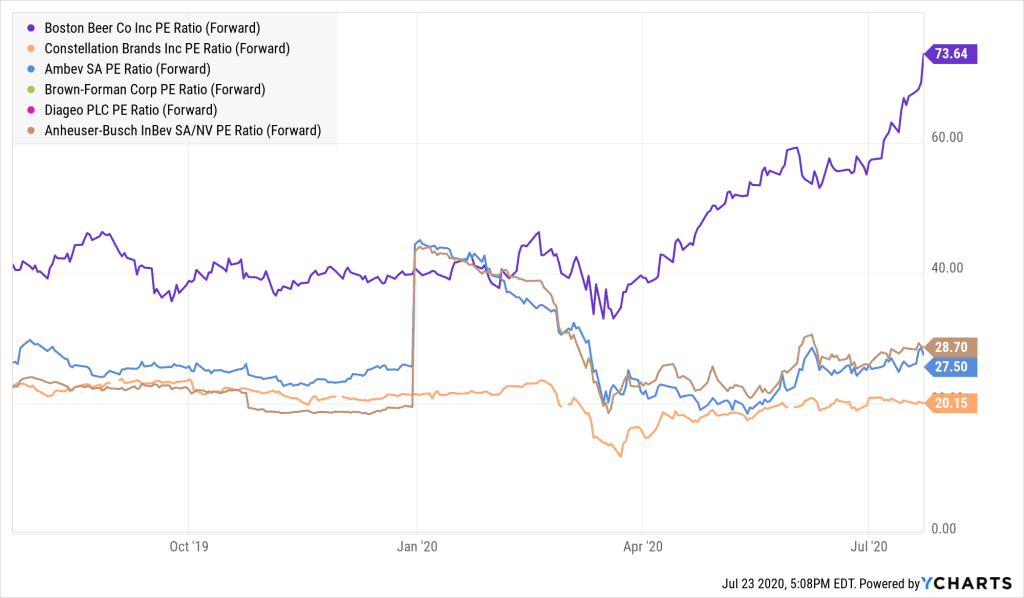

Therefore, it is a no brainer that B.B.C’s price to earnings multiple is the highest amongst its peers as illustrated below.

Final Remarks

The impact of the pandemic has given an excellent boost to The Boston Beer Company’s top and bottom line performance.

In a time where many companies are struggling to keep afloat through debt financing, B.B.C. has the privilege to avoid such means to operate thanks to its already strong balance sheet.

Therefore, it is definitely worth taking a look at if you have space for one more position in your portfolio.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.