More Pandemic, More Fed Bailout

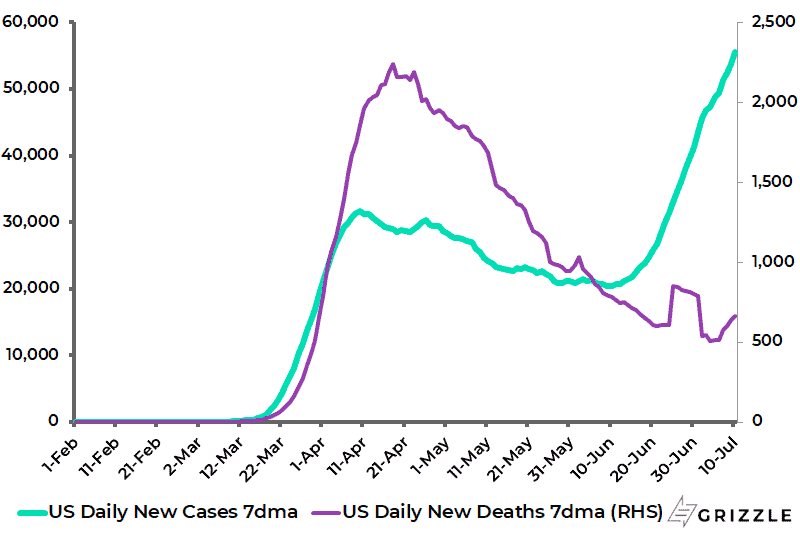

There remain legitimate reasons for concerns about second waves, even though for now there continues to be a wide divergence between cases and deaths in America.

The 7-day average daily new cases in America have risen by 173% since bottoming in early June, while the average daily deaths are down 70% from the peak reached in April though they have risen by 30% from the low reached on 4 July.

Daily New Covid-19 Cases and Deaths in America (7-day mov. avg.)

Still, the reality is that any renewed concerns about the pandemic will, under Jerome Powell, trigger more dramatic Fed easing in response to any resulting stock market weakness.

It is, by now, clear that this man seems willing and able to buy everything and anything, including equities, if he deems it necessary.

Obviously, this writer does not approve of this as a matter of public policy. But that is irrelevant from the practical point of investing in markets.

So in this sense, bad news on the pandemic, in terms of second waves and the like, will again prove to be good news for equities even if that news triggers initial sell-offs.

The Real Risk: Virus Burns Off and Stimulus is Withdrawn

In this sense what the stock market, and the growth stocks, really need to worry about, ironically, is that the base case on the pandemic turns out to be true.

That is that Farr’s Law works and the virus essentially burns itself out sooner rather than later. For in this context V-shaped recovery expectations will return to the market with a vengeance along with yield curve steepening.

This will be further encouraged by investors’ growing realization that, in the case of America, amendments last month to the so-called Paycheck Protection Programme (PPP) make it much more likely that temporary laid-off workers will be rehired.

The details of this issue are worth spelling out.

The requirement that companies have to spend 75% of the PPP loan on payrolls to qualify for complete loan forgiveness was reduced in early June to 60%. That means the amount of the loan that can be spent on other expenses, including rents, mortgage payments, utilities and interest on loans, is increased from 25% to 40%.

The law also extends the time period to spend the loans from eight weeks to 24 weeks, while pushing back the deadline to rehire employees from 30 June to 31 December.

It is this requirement to rehire temporarily laid-off workers by the end of this year, in order to qualify for loan forgiveness, which creates the potential for a dramatic rebound in employment.

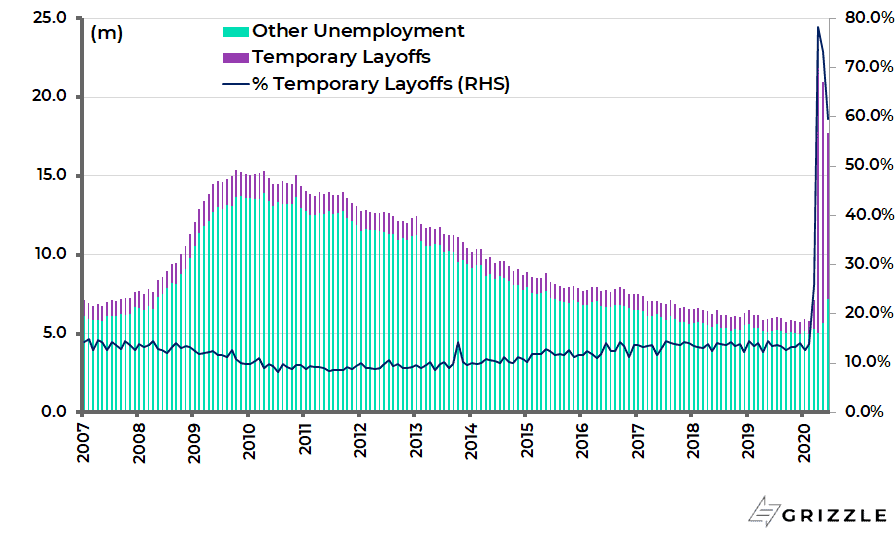

Total unemployment surged from 5.8m in February to a record 23.1m in April and was 17.75m in June.

Of the total in June, 10.6m or 60% are classified as unemployed on temporary layoff, meaning that they have been offered to return to work or are expected to be recalled to their job within six months.

This is down from a peak of 18.1m in April (78% of total unemployment) but up from 801,000 in February (14% of the total).

Excluding such temporary layoffs, the unemployment rate in June would decline from the reported 11.1% to only 4.5%, compared with peak of 14.7% reached in April.

US Unemployment Breakdown

In an environment of rising V-shaped recovery expectations, market focus will sooner or later turn to concerns about a withdrawal of extreme stimulus (i.e., good news becomes bad news).

It is at that point that the Fed will likely announce “yield curve control” in the sense of introducing price controls in the Treasury bond market.

That will mark the formal introduction of financial suppression in the American financial system and, with it, the likely ending of the deflationary era and the beginning of a new inflationary one.

Pent-Up Demand from COVID-19 Forced Savings

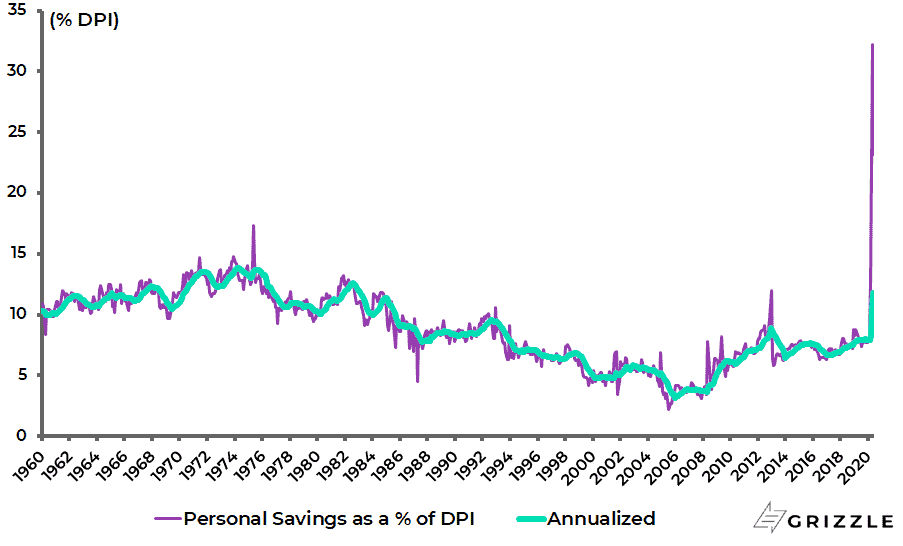

Meanwhile, in a world where the concerns about the virus have suddenly disappeared, the pent-up demand from all those forced savings during the lockdowns should not be underestimated.

The US personal savings rate surged from 8.4% of disposable income in February to a record 32.2% in April and was 23.2% in May.

US Personal Savings as % of Disposable Income

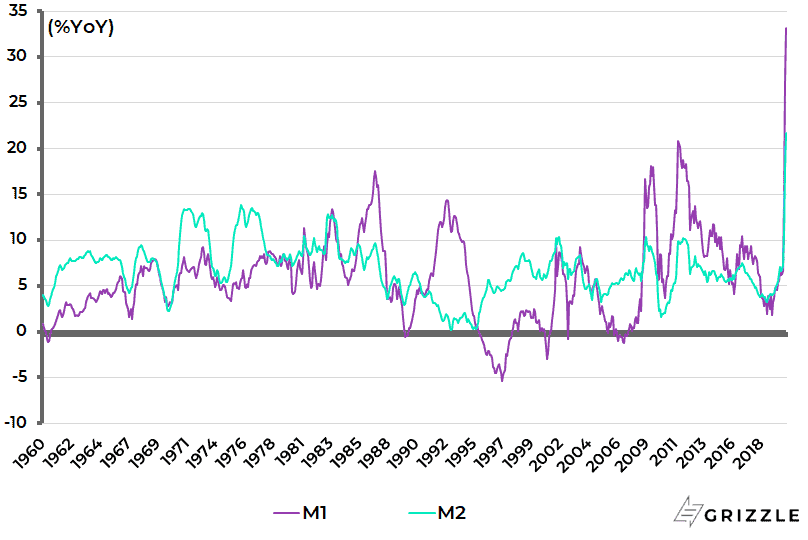

In such a world there is clearly the potential for inflation readings to surprise on the upside, a fact also signaled by the continuing surge in both broad and narrow money growth, be it in America or, for that matter, in the Eurozone.

US M1 and M2 rose by 37.3% YoY and 24.1% YoY, respectively, in June, the fastest growth rates since the data series began in 1959.

US M1 Growth and M2 Growth

Still the timing of such a withdrawal-of-easing scare in the markets is most likely to be a third-quarter affair if Farr’s Law proves correct.

Such a scare will then run into the gathering noise of the presidential election campaign where Donald Trump will be doing everything in his power to raise expectations of a V-shaped recovery.

If the Second Wave Materializes, Buy the Dip

But what about if the second wave really happens in size?

In that event, this writer would expect any second wave triggered sell-off to be a buying opportunity. This is not only because of renewed central bank easing, but also because this writer does not expect governments to lock down economies in the same across-the-board way again.

This is because it is now realised, though not admitted by the vast majority of politicians, that these lockdowns did more harm than good once it became clear that hospital systems were not being overrun.

In this respect, US Treasury Secretary Steven Mnuchin stated in a CNBC interview last month that, in the event of the so-called second wave, there would not be a repeat of the lockdown.

Mnuchin said: “We can’t shut down the economy again. I think we’ve learned that if you shut down the economy, you’re going to create more damage” (CNBC article: “Treasury Secretary Mnuchin says ‘we can’t shut down the economy again’”, 11 June 2020).

This is the closest anyone in an official position has come to admitting that governments over-reacted.

Policy should be focused on protecting the elderly and letting everybody else get on with it. What about the evidence of a second wave?

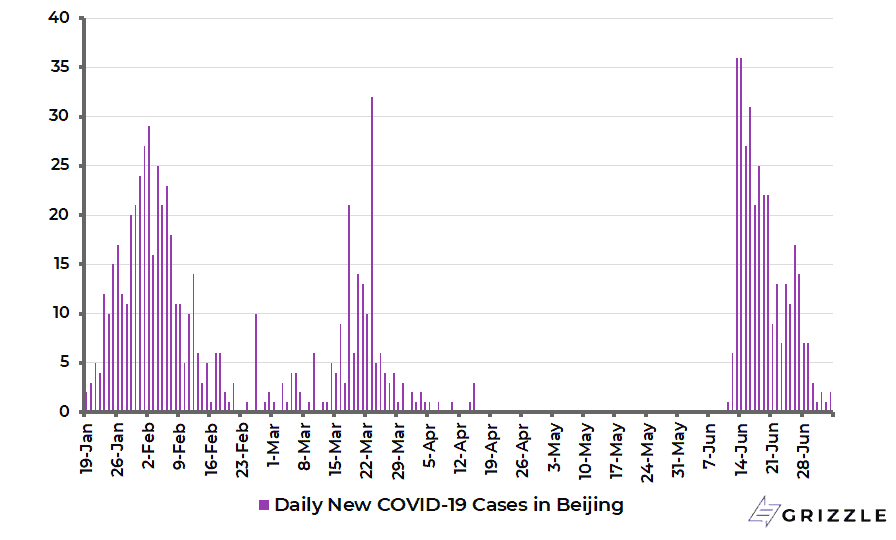

Perhaps the most worrying point over the past month was the renewed outbreak in China in the middle of summer at Beijing’s biggest wholesale food market.

There were 227 new cases in Beijing during ten days from 11 June, after having had no new infections since mid-April.

Beijing Daily New Covid-19 Cases

Still the central government, as ever, can be relied upon to have managed the outbreak as efficiently as possible.

The immediate high-risk areas were locked down with the People’s Liberation Army (PLA) enforcing the quarantine.

While Beijing tested 2.3m people in the following week. Cases have now collapsed!

Indeed there has been no new cases in Beijing over the past five days. Meanwhile, in a classic example of turning a negative into a positive, the unemployed were being paid about three times the minimum wage in the capital (around Rmb300/day) to do contact tracing.

What about America’s risk of a second wave?

Some of the states where the cases are now rising are those which did not really suffer in the first surge during March and April, or those that had not declined significantly from their April highs.

In this sense, the new cases may not really constitute a second surge. For example, 7-day average daily new cases have risen by 395% since mid-May in California to 8,624, and by 768%, 1322% and 889% since late May in Texas, Florida and Arizona to 8,280, 9,365 and 3,574 respectively.

By way of comparison, in early April there were “only” 1,357 cases in California, 9,22 in Texas, 1,214 in Florida and 2,03 in Arizona.

Daily New Covid-19 Cases in California, Texas, Florida and Arizona (7-day mov. avg.)

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.