The base case remains that a US-China trade deal is coming. This should continue to support stock markets for now, helped by the following wind provided by the “Powell Pivot”.

Meanwhile, one longer-term threat to U.S. equity valuations is emerging in the form of the growing risk of left-wing populism in America. This is not only a reference to the rising number of Democratic presidential candidates competing to sound more socialist. Indeed more relevant, from a narrow stock market standpoint, is the growing political focus on the negative consequences of leveraged financial engineering in America.

A prominent example of this of late was an op-ed published in the New York Times last month by Senate Minority Leader Chuck Schumer and former Democratic presidential candidate Bernie Sanders (see New York Times article “Schumer and Sanders: Limit Corporate Stock Buybacks”, Feb. 3, 2019). This article amounted to a coherent critique of the excesses of America’s by now very-long-in-the-tooth share buyback boom.

I certainly have no problem with the argument made in this article, having long highlighted how leveraged share buybacks in the U.S. have become a perversion of the original idea behind such an exercise.

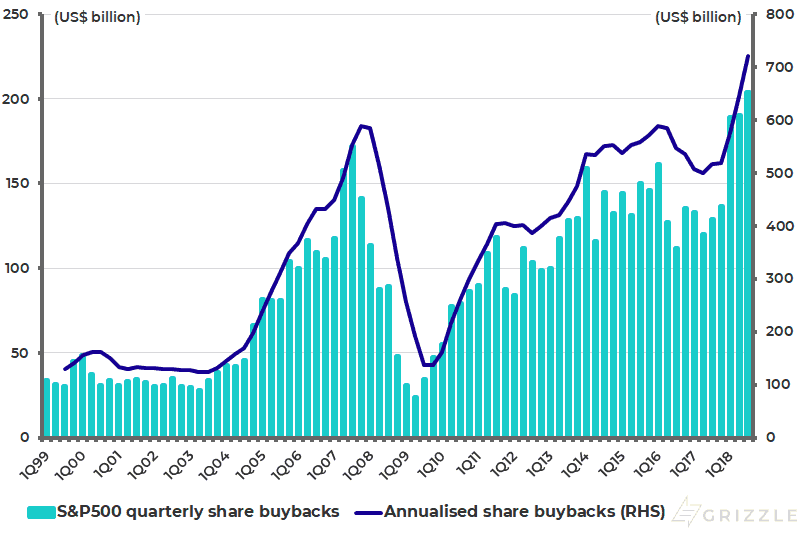

Still, there is no doubt that the share buyback bonanza triggered by last year’s tax cut has now politicized the issue and made such criticism mainstream. After all, there were three consecutive quarters of record share buybacks in the first three quarters of 2018 and the estimates for the fourth quarter are for a further record. S&P500 actual share buybacks rose to US$189 billion in 1Q18, exceeding the previous record of US$172 billion reached in 3Q07, and were US$204 billion in 3Q18 (see following chart). S&P Dow Jones Indices expects 4Q18 buybacks to exceed the 3Q18 level.

S&P500 share buybacks

Share Buybacks Despite Little Business Investment

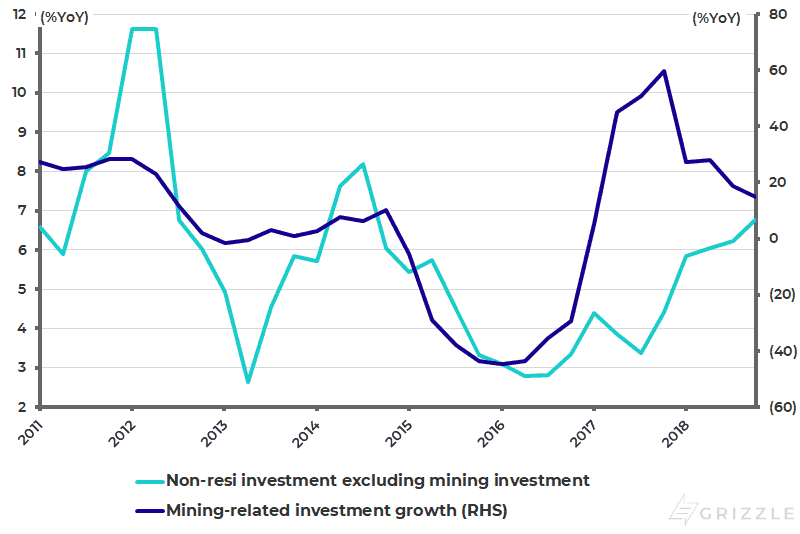

This continuing share buyback frenzy contrasts with the relative lack of a pickup in business investment spending outside the shale energy area despite last year’s massive corporate tax cut. Thus, U.S. real private non-residential investment excluding mining-related investment rose by only 6.2% YoY in 2018, compared with a 21.8% YoY increase in mining-related investment (see following chart).

Meanwhile, nominal private non-residential fixed investment, on a seasonally adjusted annualized basis, increased by US$228 billion in the four quarters to 4Q18. This is equivalent to only 39% of the US$583 billion spent on share buybacks by S&P500 companies in the first three quarters of 2018.

US real private non-residential fixed investment growth excluding mining investment

Share Buyback Legislation Comes as No Surprise

The critique of share buybacks is understandable given the main focus of such an exercise in America has been to boost ROE in an artificial manner and thereby to increase executive compensation.

There is less enthusiasm here about the legislation advocated by Messieurs Schumer and Sanders. That is to “prohibit a corporation from buying back its own stock unless it invests in workers and communities first, including things like paying all workers at least US$15 an hour, providing seven days of paid sick leave, and offering decent pensions and more reliable health benefits”.

It is no surprise that such legislative initiatives are now being publicly advocated in America given the admittedly grotesque divergence between executives’ compensation and that of general employees.

Indeed, the only surprise is that it did not happen several years ago. Meanwhile, it is not only the Democrats who want to address the issue of share buyback excesses. Republican Senator Marco Rubio also signalled last month that he would soon introduce legislation that would treat corporate share buybacks as dividends for tax purposes, thereby creating equality of treatment.

Also, in a bid to encourage more investment, Rubio said he would seek to make permanent a temporary tax code provision from last year’s tax reform that allows companies to write down capex in the year they spend the money (see Reuters article “US Republican Senator Rubio pushes plan to tax stock buybacks”, Feb. 14, 2019).

The Challenge to the U.S. Stock Market

Both proposals seem eminently sensible and would in the long term create a much healthier American economy. They would, however, constitute a challenge for the American stock market since corporates have been by far the biggest buyers of shares since the most recent bull market began in 2009. To be precise, U.S. non-financial corporations’ net buying of corporate equities has totalled US$3.67 trillion since 2009, compared with net buying of US$1.74 trillion by mutual funds and ETFs.

Indeed this has been a bull market driven by corporate buying, much of it on leverage. It is also important to highlight that this corporate buying has not just been about companies buying their own shares with borrowed money. It has also been about buying other companies’ on leverage via M&A or, via the booming private equity industry, through leverage buyouts.

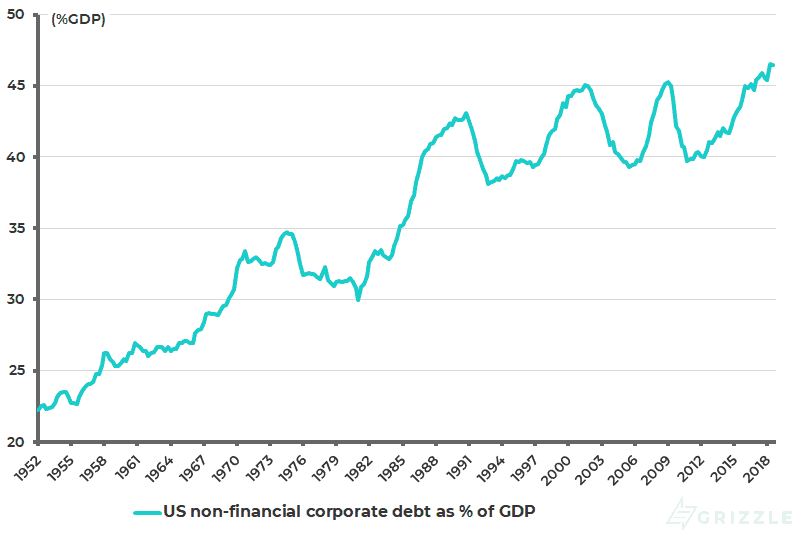

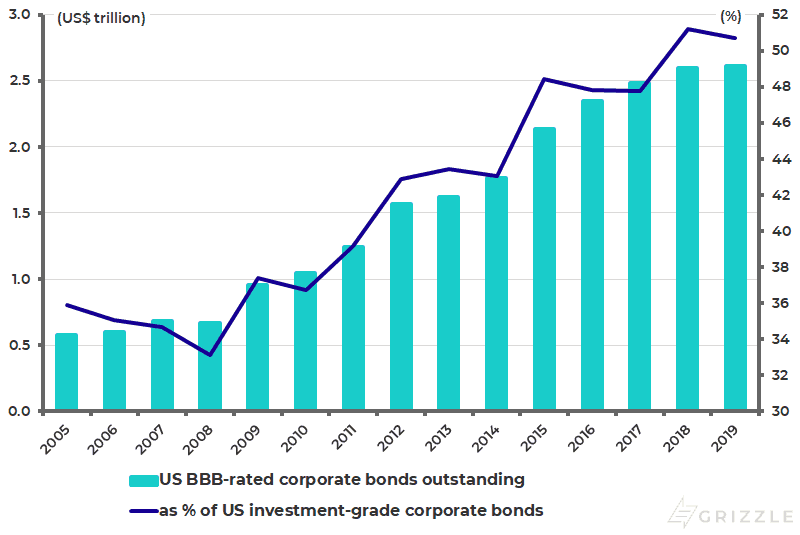

The consequences of a decade of this activity are now clear from the rise in non-financial corporate debt to record levels as a percentage of GDP (see following chart), from the scale of Triple-B corporate bond issuance (see following chart) and from the explosion in leveraged loans.

It is also clear from the increase in goodwill in corporates’ balance sheets and the resulting decline in tangible book value on the S&P500. S&P500 tangible book value per share has declined by 30% since peaking in 2014, while S&P500 goodwill per share is up 60% over the same period, according to Bloomberg data. Bloomberg calculates tangible book value as total common equity less goodwill, patents and other disclosed intangible assets.

US non-financial corporate debt as % of GDP

US BBB-rated corporate bonds outstanding

There is no need to go into all the details again of the above corporate debt excesses, save to say that the political attack on share buybacks is coming too late to prevent a nasty hangover in the next economic downturn. In this respect, the only hope must be that the “Powell Pivot” will delay that downturn. It should also be remembered that monetary tightening works with a lag and the Fed has been tightening since December 2015.

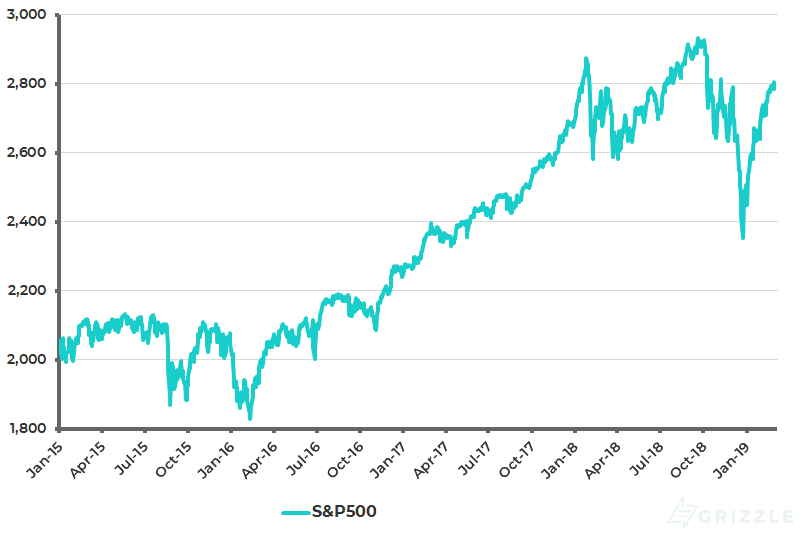

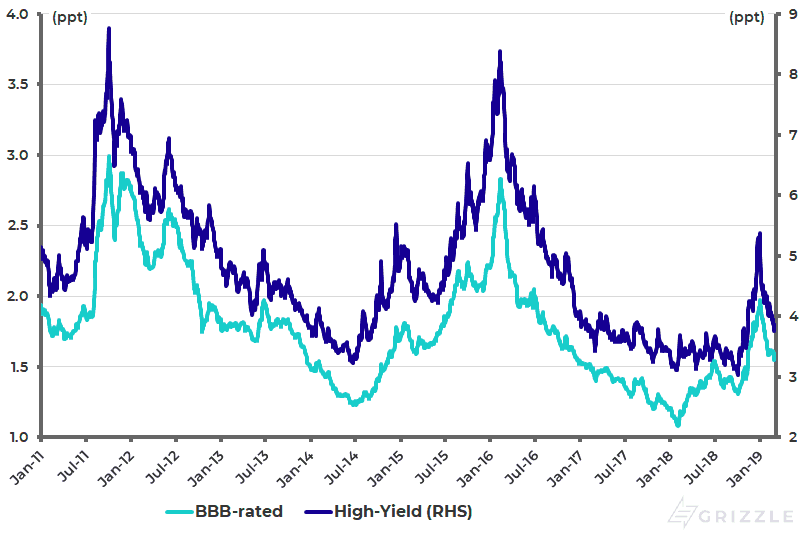

Meanwhile, the more US-correlated world stock markets rally, and the more credit spreads come in, the less pressure perhaps on the Fed to stop balance sheet contraction. The S&P500 has risen by 19.5% since bottoming on Dec. 26 (see following chart), while U.S. BBB-rated corporate spreads and high-yield corporate spreads have declined by 42bp and 161bp respectively since peaking in early January (see following chart). That said, it will be hard for Jerome Powell to do another U-turn having now essentially told markets that balance sheet contraction is ending sooner rather than later. Indeed the Fed chairman said in his Congressional testimony this past week that the Fed is close to announcing plan to end the balance sheet “runoff”.

S&P500

US BBB-rated and High Yield corporate bond spreads

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.