A smart analyst we respect made an astute observation about how Slack chose to go public.

Slack’s decision to use a direct listing made it possible for insiders to sell 50% of shares, up from the typical 15% in an IPO offering.

Management and early investors were comfortable pushing the valuation above a sustainable level because they could still sell stock on day 1 and lock in gains instead of being punished in a typical IPO with a six-month lockup.

During a lockup, an overpriced stock with bad sentiment like Lyft can fall significantly, erasing any gains management would have realized from going public at a premium and selling out.

Sentiment is all-important in IPOs with no public operating history and Slack looks to have pushed the stock too high too fast and burned early public investors in the process as insiders sold.

43% of the shares changed hands on Slack’s first day as a public company.

Now that the stock is retesting the $26 IPO price we think investors should start sharpening their pencils. Insiders who wanted to sell have mostly sold already and the fundamentals of the business are stronger than ever.

Slack is looking just like Facebook in the first 12 months after that company’s IPO.

From May of 2012 to August Facebook fell from $38.00 all the way down to $18.00 before results really started to sing and the stock went on a huge 6-year run of outperformance.

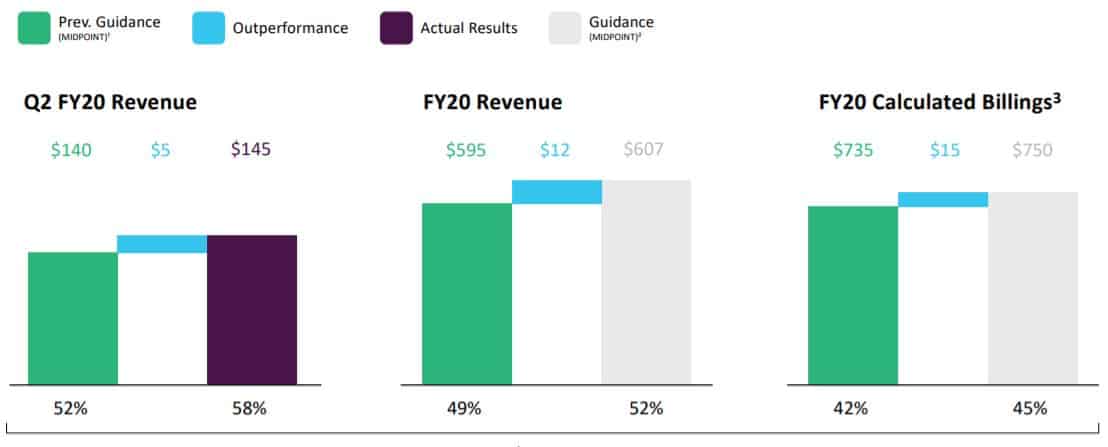

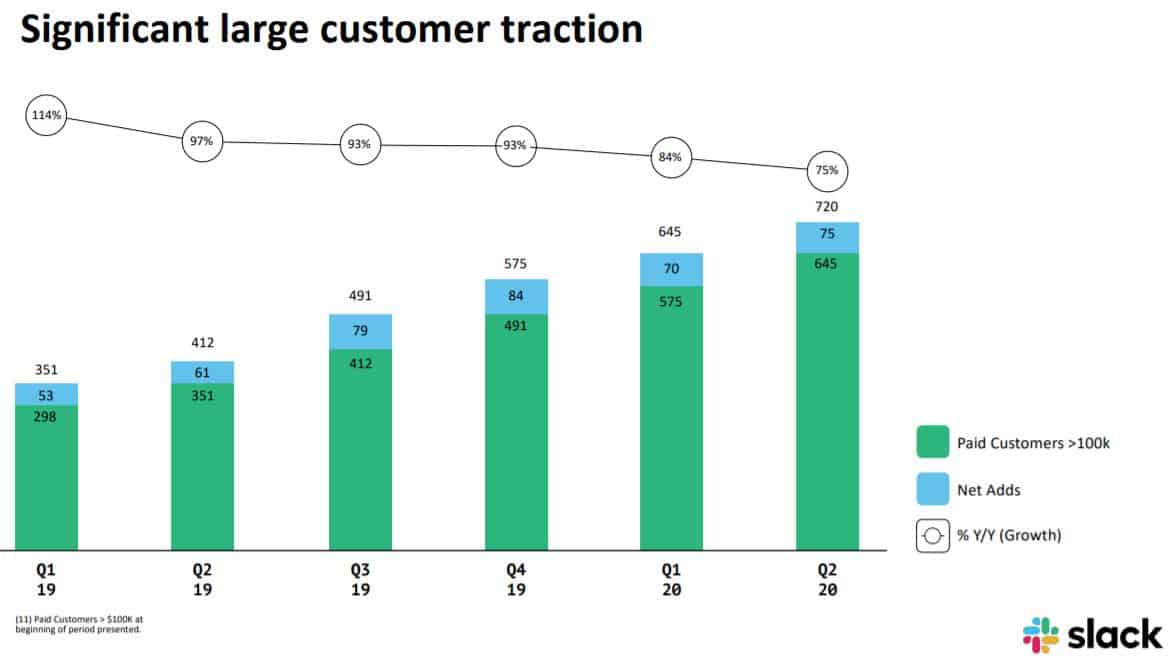

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Analysts and the market are focusing on continued bottom-line losses and a one-off revenue hit from service outages while all we see is a company who beat revenue estimates by 10% and is growing their corporate customer base by 75% year over year. [/su_panel]Investors should begin scaling into the stock based on these earnings results and should look to add more if the company falls into the low $20s or demonstrates the trend has flipped with a move through $35/sh.

Slack is Exceeding Revenue Expectations

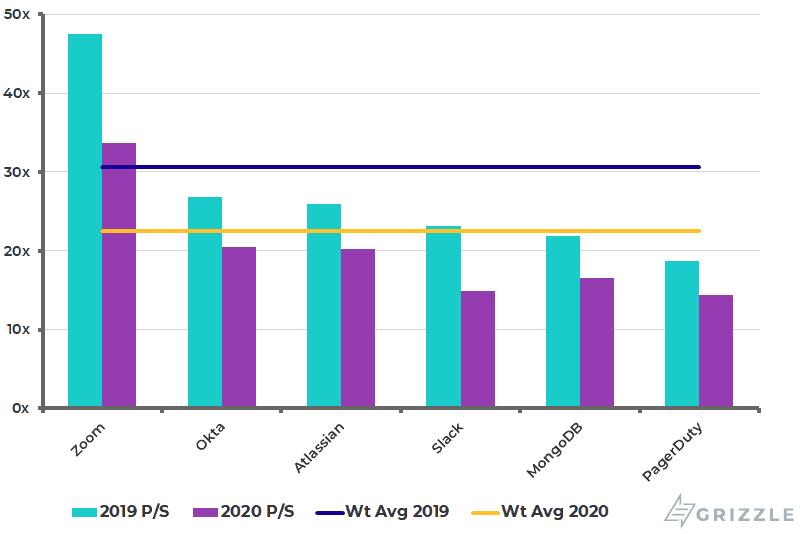

Valuation is High, but So is the Growth

Most of Slack’s detractors have been pointing to the above-average price to sales as the reason not to own the stock.

With the recent stock weakness bringing the multiple down to 24x, we think the valuation is no longer a reason to sit on the sidelines.

Slack is now trading at a 15% discount to other tech peers while growing 25%-50% faster than even Zoom, a company trading at twice Slack’s multiple.

All you need to understand about valuation is that Slack will quickly look very cheap if growth continues as we expect.

By next year the multiple will have fallen to 15x and to a legitimately cheap 10x the year after that if the stock stands still.

Price to Sales Multiples of Slack Peers

Start Buying in, the Upside is Substantial

With a huge cash runway of more than 8 years, Slack has the luxury of aggressively going after market share without worrying about raising capital or conserving cash.

The most powerful vindication of Slack’s value came from a recent comment made by the CEO about a large enterprise customer win.

We think the market is totally missing the true power of the Slack product offering vs its main competitor Microsoft Teams.

On paper there are as many Team’s customers as Slack customers, however, we guarantee anyone on Teams only has the software as part of a Microsoft 365 bundle.

Until we see usage data proving otherwise, Teams is really an afterthought to most customers.

Slack offers a compelling alternative that has already matched Microsoft’s market share and the service will continue to take over the market directly under the nose of big M.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.