Collaboration software provider Slack (NYSE:WORK) reported strong results after the close, however, the stock is down 20% after hours likely driven by revenue estimates for next quarter that were lower than the market was expecting and guidance for 2020 that only met expectations.

Slack also guided to $20 million of negative free cash flow in 2020 compared to $62 million burned this year.

This is an improvement for sure, but while the market is melting down, investors absolutely hate the idea of another 12 months of losses.

Revenue of $182 million beat by 4% compared to analysts estimates of $174 million.

Slack generated an adjusted EPS loss of -$0.04/sh beating estimates of a -$0.07 loss by 38%.

The cashflow deficit generated after reinvesting in the business, also called free cashflow, was -($835,000) this quarter, a big improvement from (-$19) million last quarter.

Most importantly Slack is generating positive cashflow from operations this quarter, a first step to truly becoming profitable.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Slack has created a killer platform and we think the stock is worth at least $30/sh as a North American story. If Slack can become a global player, there is upside to $80/sh over the next five years though this outcome is far less certain. Slack is a buy for us in the low $20s or below. [/su_panel]

Why Slack has Been Weak since the IPO

High visibility PR releases from Microsoft, touting user growth of their competing software offering has hurt sentiment in Slack badly.

But in reality, Slack is simply a better platform.

Management is having no trouble signing contracts with large corporations who already get Microsoft Teams for free as part of their Office 365 subscription.

CEO Stuart Butterfield said on last quarter’s conference call that 70% of his largest customers are also Office 365 customers.

We will let you in on a little known secret Microsoft doesn’t want you to know….

Microsoft is essentially counting customers who do the absolute bare minimum in teams as an “active” user compared to Slack active users who spend 90 minutes a day typing, chatting, and interacting with the service.

Our takeaway is that Slack is building a more robust ecosystem and will have no problem growing its paying users even in the face of stiff competition from Microsoft.

But What is Slack Worth?

Our discounted cashflow value of Slack comes to $30.00/sh if the company grows to 24 million active users by 2030, from 12 million today, representing 40% upside.

Using multiples instead, if Slack trades at the price-to-earnings multiple of Microsoft longer-term (25x), the stock is worth $30-$33/sh.

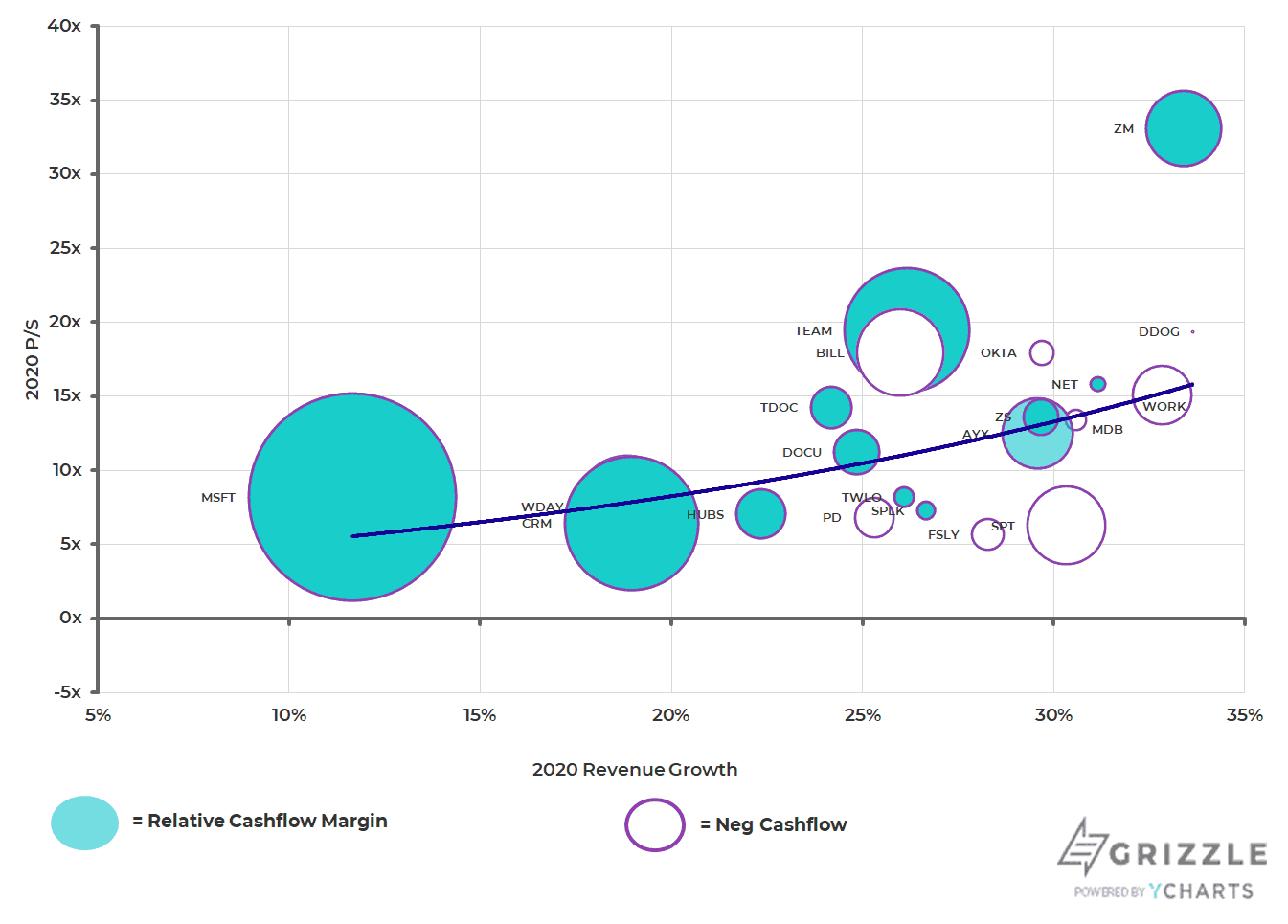

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Bottom Line: If Slack can’t grow beyond North America it’s a $30 stock, offering decent upside after the recent selloff, however if email 2.0 is truly a global product, there is upside to $80/sh in five years.[/su_panel]Slack is one of the fastest-growing SaaS companies today and the only thing holding the multiple back from reaching the high teens (currently at 15x) is the uncertain path to profitability.

We know personally how effective and sticky the Slack offering is, as we use it in the office everyday and with significant potential upside if the company can execute we think the stock is worth owning today.

If you don’t have a position yet, start to nibble, investing your total preferred amount over 30 days at minimum, so you don’t start with big coronavirus-driven losses.

We think this company has real potential being fully priced in by the markets.

Slack is Not Expensive Even on Today’s Multiples

Customer Adds Bolster Recurring Revenue Streams

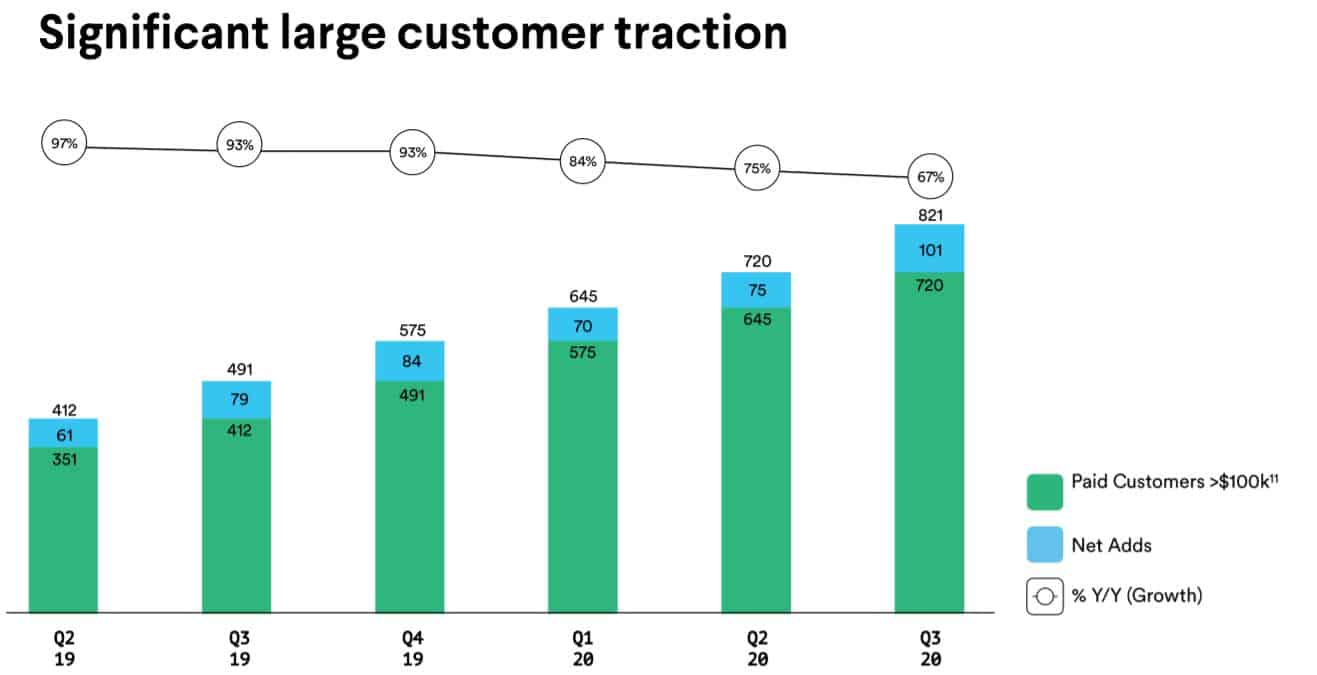

A major part of what makes Slack so appealing from an investment standpoint is the company’s ability to lock in recurring revenue streams from some heavyweight customers.

In the last quarter alone, it added 72 paid customers that generate more than $100,000 in annual recurring revenue for the company.

This brought its client base in this key growth segment to 893 paid customers, 55% more than it had at this time last year.

As management asserted, this shows that large businesses are turning to Slack as their main collaboration platform and doing so at a rapid pace. Slack exited the quarter with 30% year-over-year paid customer growth with more than 105,000 customers worldwide.

The company’s net dollar retention rate was a remarkable 134% in the recent period. Net dollar retention rate is a key metric in evaluating software-as-a-service (SaaS) firms because it measures how much an existing client base is upgrading its commitment level relative to downgrades.

A figure north of 100% suggests healthy growth from existing customers.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.