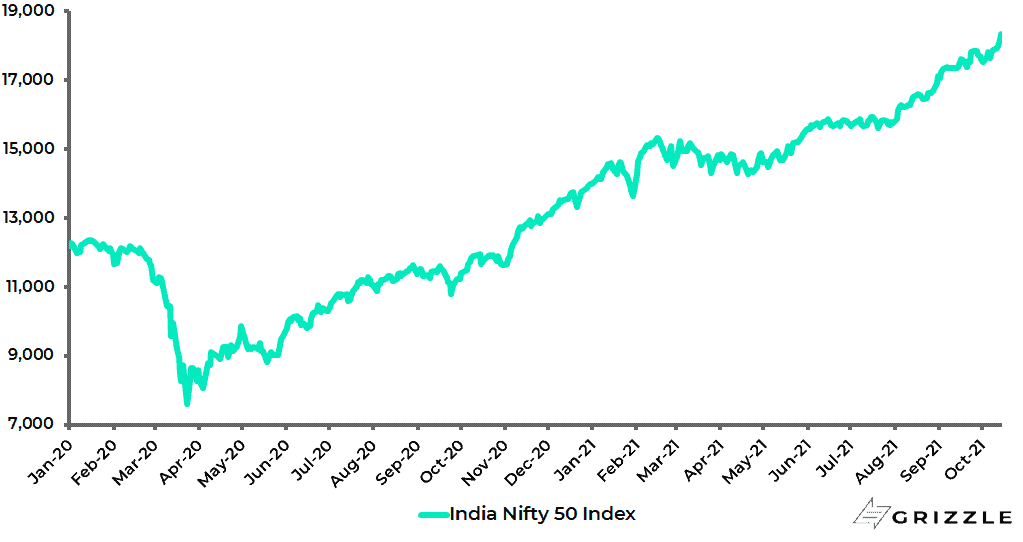

The Indian stock market has remained extraordinarily resilient since the Delta wave peaked in May.

India Nifty Index

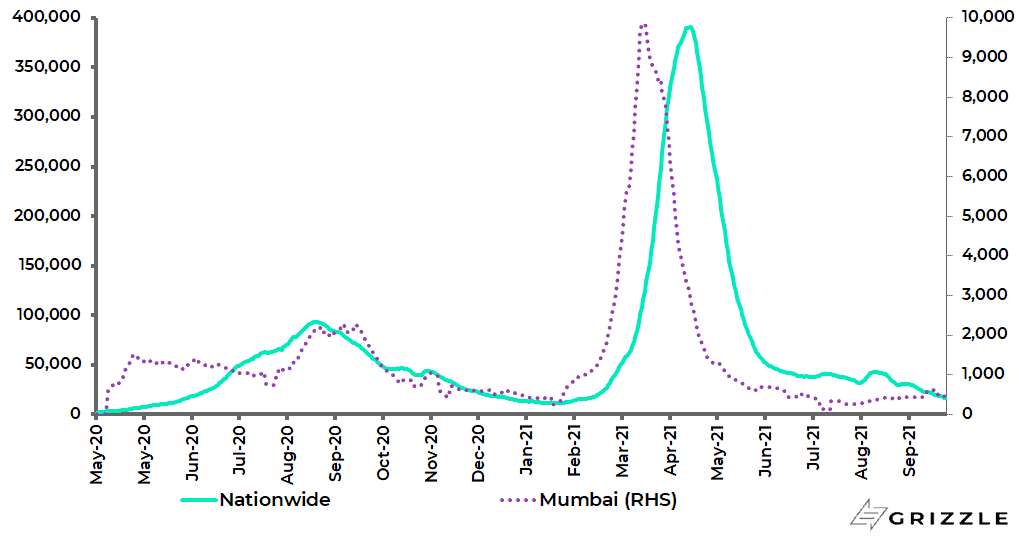

Covid cases remain way off their high while the vaccination rate is now running at around 4m doses daily.

The 7-day average daily new Covid case count has declined by 96% nationwide from the May peak and is also down 96% in Mumbai from the April peak.

A total of 282m or 20% of the Indian population has now received two jabs.

India and Mumbai 7-day average daily new Covid cases

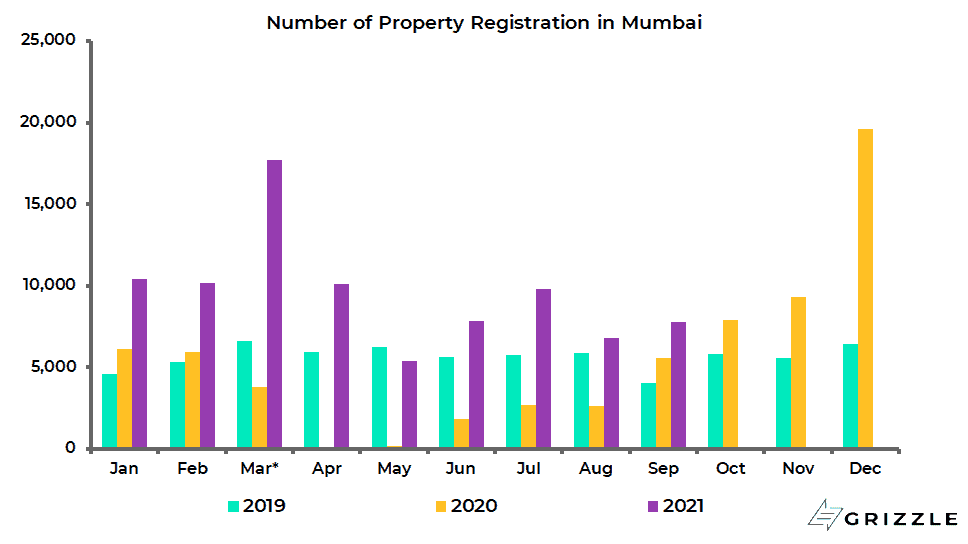

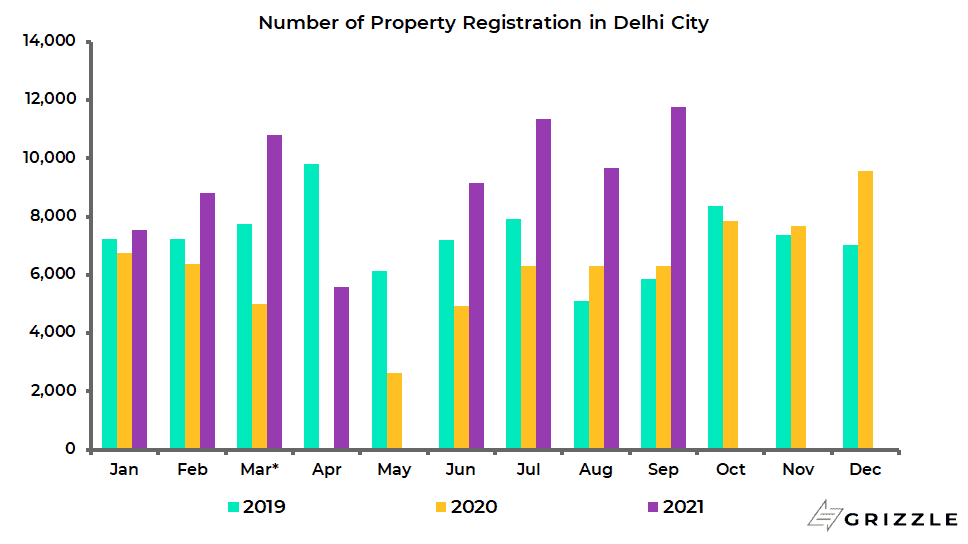

Pre-sales across the top seven cities rose 13% YoY in July-August based on data from PropEquity.

Also property registrations, indicating completed transactions, for the months of July-September were up 56% in Mumbai and 74% in Delhi compared with the levels prevailing in 2019.

Number of property registrations in Mumbai

Number of property registrations in Delhi

Meanwhile, unsold inventory is coming down sharply, most particularly as a large part of this inventory is stalled projects which may never be completed.

The inventory level in the National Capital Region (NCR) in the greater Delta area, after stripping out such stalled projects, has declined from a peak of 50 months of sales in October 2017 to 33 months.

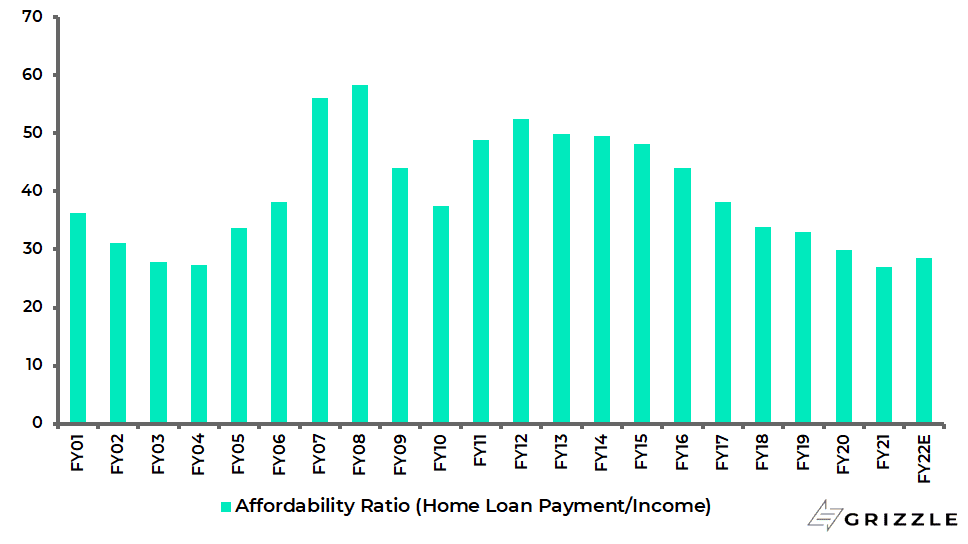

It is also the case that affordability remains at historically attractive levels.

The housing affordability ratio, measured as home loan payment as a percentage of income, has declined from 53% in FY12 to the record low of 27% in FY21 and is estimated at 28% this fiscal year.

This is clearly very different from, say, China.

India housing affordability ratio

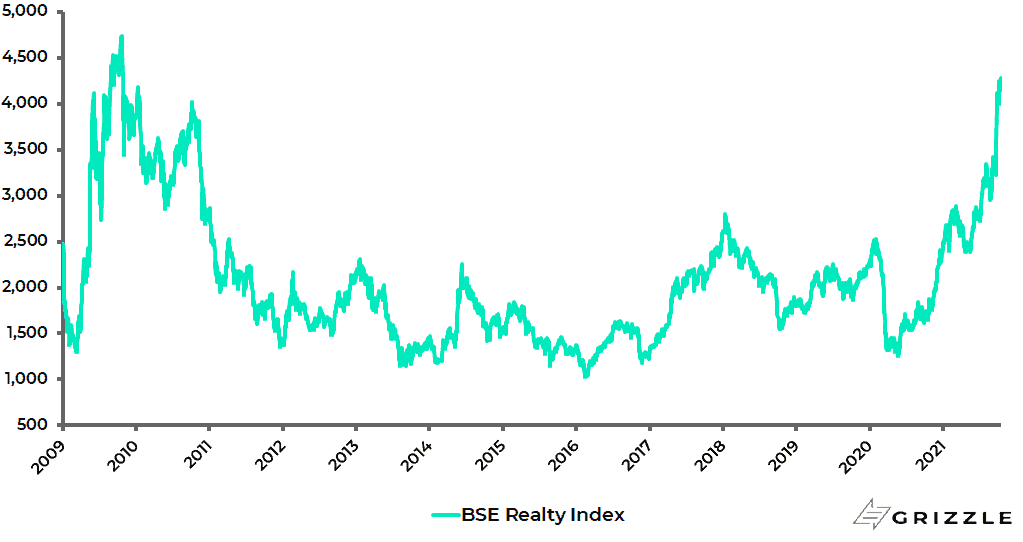

Meanwhile, investors’ growing realisation that Indian property is on the move is shown by Indian property stocks hitting their highest level since October 2009 last week.

BSE Realty Index

A Broader CAPEX Cycle is Only a Year Away

A broader-based private sector-driven capital spending cycle, extending beyond the property sector, is now likely to be only a year away.

The steel sector, for example, has started to see a pickup in capex.

Combined capex plans of major steel companies rose from Rs97bn in FY21 to an estimated Rs281bn this fiscal year.

In the previous capex cycle from 2004-2010, the housing upturn led the broader capex cycle by 12-18 months.

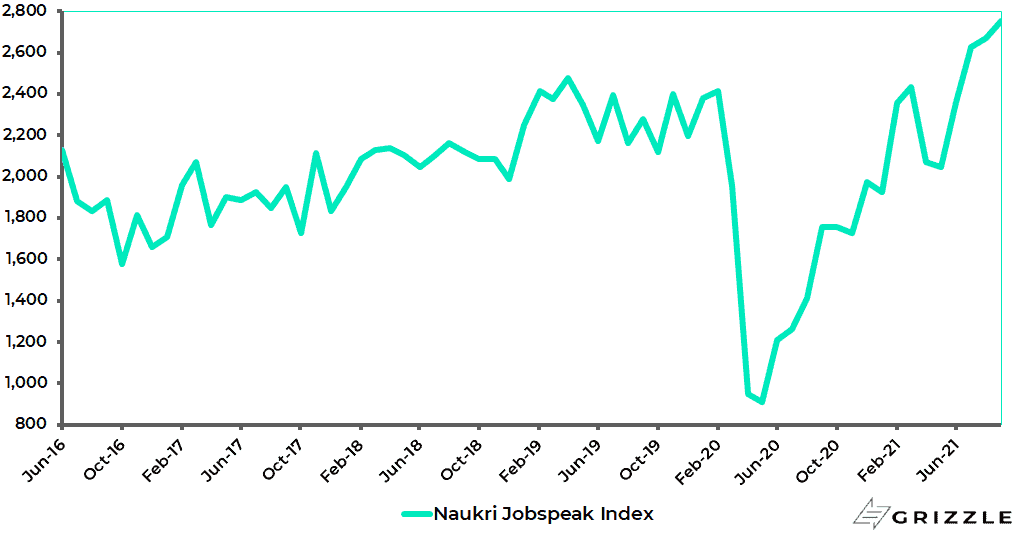

A further positive is growing evidence of job generation.

The top-tier IT service companies hired a net 55,000 people in 1QFY22 ended 30 June and are expected to hire a net 130,000-160,000 this fiscal year.

It is also important, from an employment perspective, that during the Delta wave state governments allowed construction projects to continue.

Construction accounts for 60m people or 12% of the estimated organised workforce.

Meanwhile, hiring activities in India, as measured by the Naukri JobSpeak Index calculated by the leading job listing website Naukri, rose by 57% YoY in September and is now up 21% compared with the pre-Covid level in September 2019.

India Naukri JobSpeak Index

The Bank of India Won’t Stand in the Way of a Stock Market Recovery

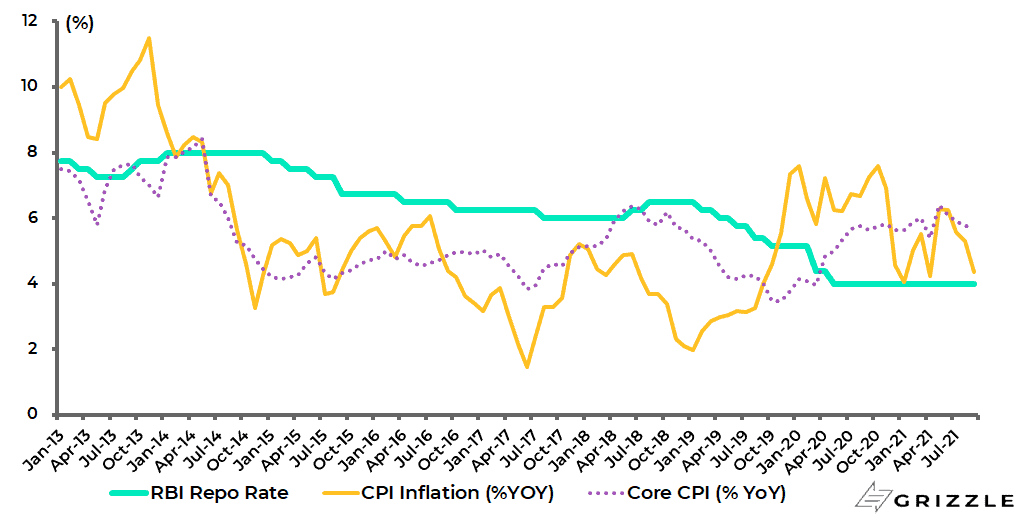

Aside from the risk of another Covid wave, the major domestic risk to the stock market is a change in the Reserve Bank of India’s dovish policy.

The central bank had been raising its inflation forecast in recent meetings but has yet to signal a change in policy.

The RBI increased its CPI inflation forecast for this fiscal year to 5.7% in its policy meeting on 4-6 August, up from 5.1% projected in June, though it lowered its forecast to 5.3% in the latest meeting on 6-8 October.

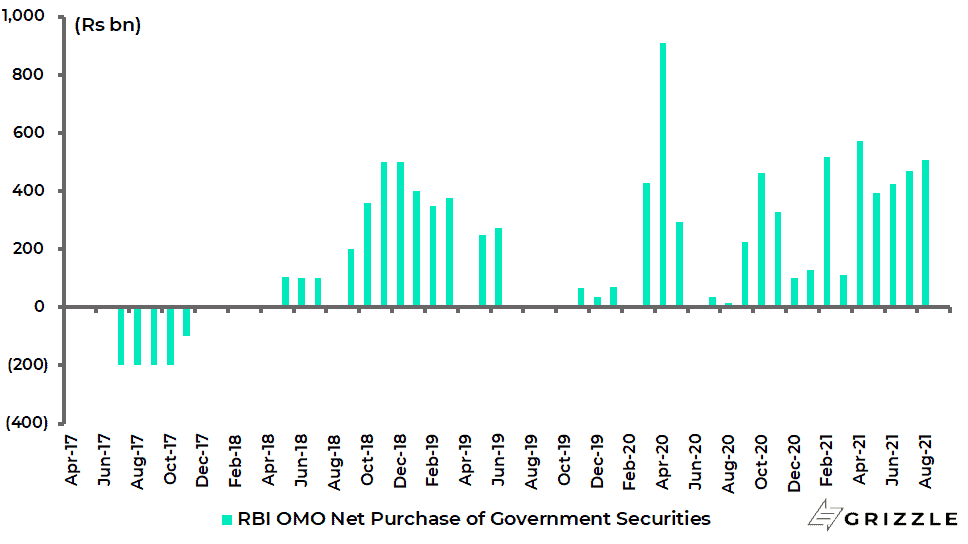

Still the RBI’s bond purchases under the Open Market Operations (OMO) programme have continued.

The RBI OMO net purchases totaled Rs978bn in 3Q21 and Rs3.13tn year-to-date.

RBI OMO Net purchases of government securities

While there is no talk as yet of rate hikes, the policy repo rate is currently 4.0%.

The next RBI meeting is on 6-8 December.

Meanwhile, headline CPI inflation has slowed from 6.3% YoY in June to 4.3% YoY in September while core inflation is running at 5.8% YoY.

India CPI inflation and RBI policy repo rate

The RBI is likely to start to slow its bond purchases before the end of the year, with the first rate hike probably coming in the first half of next calendar year.

But any changes in policy should be very gradual.

The easy money stance has clearly been one key driver of the stock market rally.

But India also seems to be at a major inflection point in earnings with the corporate profits to GDP ratio bouncing off a 20-year low of 1.9% in FY20 to 3.5% in FY21.

Foreign Interest is Just Beginning to Pick Up

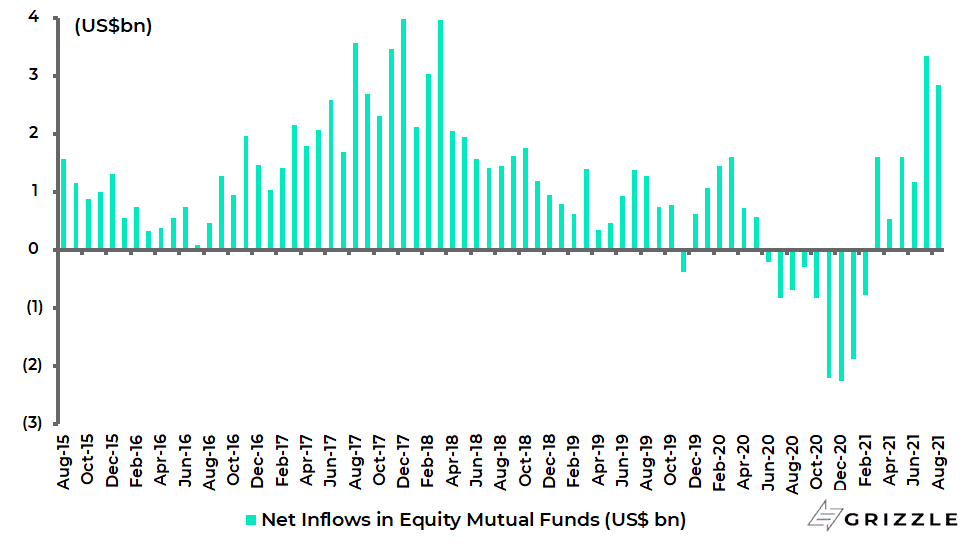

Meanwhile from a flow of funds perspective, there have now been six consecutive months of inflows into equity mutual funds.

Net inflows into domestic equity mutual funds totaled US$11bn in the six months to August, compared with net outflows of US$10bn over the previous nine months (see following chart).

Net inflow into India domestic equity mutual funds

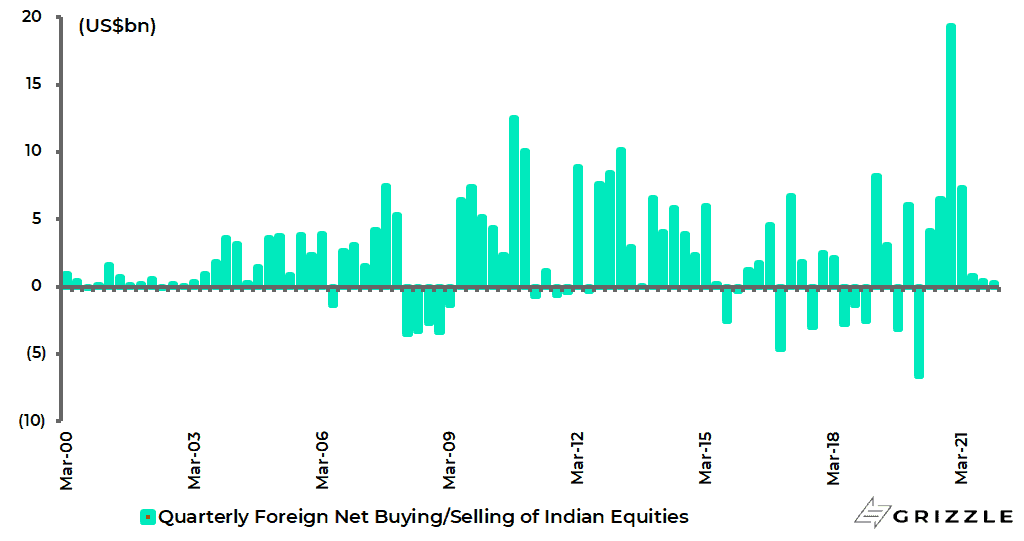

That has also helped support stocks given the lack of net foreign buying of equities.

Foreigners have bought only a net US$1.2bn over the past six months, compared with net buying of US$7.3bn in 1Q21 and a record quarter of US$19.3bn in 4Q20.

Quarterly foreign net buying/selling of Indian equities

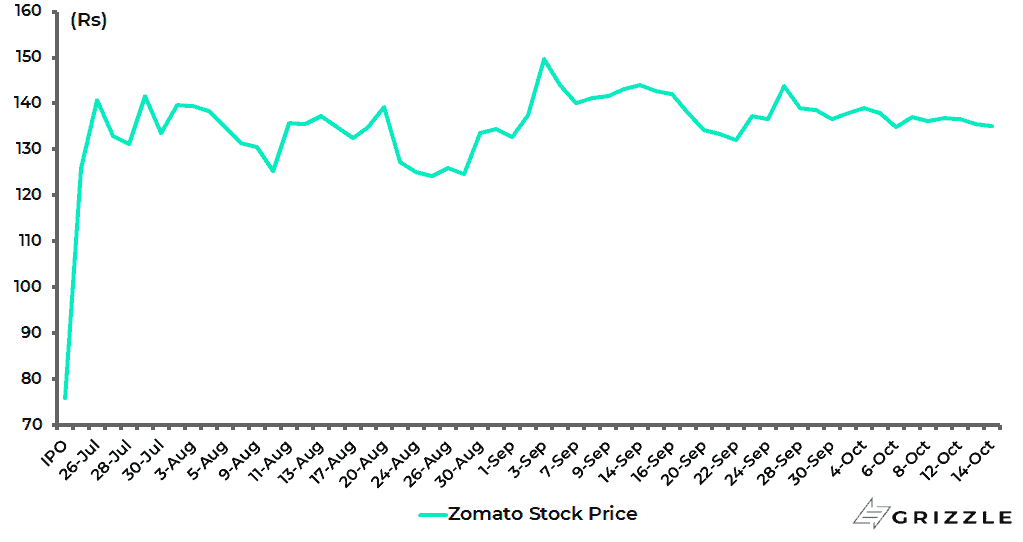

The pattern has been for foreigners to sell existing stocks to fund investments in primary offerings with unicorns coming to market, following on from the success of the Zomato listing in August.

Zomato, India’s Meituan, is now 78% above its IPO price.

Zomato share price

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.