While strolling the halls of the Prospectors and Developers conference last week we bumped into an intriguing CEO. Marc Bishop Lafleche runs Ecora Resources, a royalty company going through a major transition.

Marc previously ran the investment team at Ecora and has spent over two decades evaluating and investing in mining projects. We filmed our conversation with Marc and have summarized the most interesting pieces of the interview below.

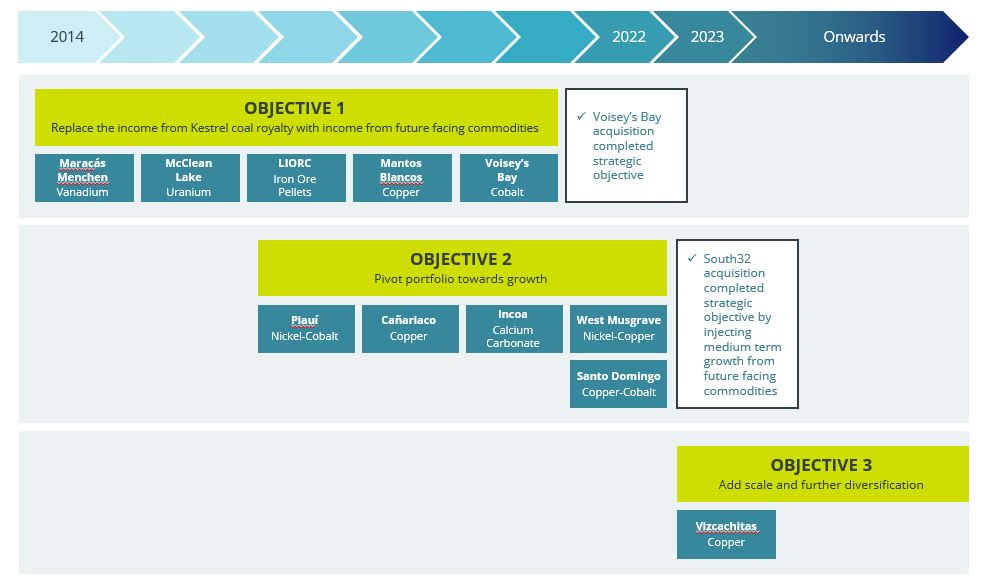

A Big Transition Under the Surface

Marc is sheparding Ecora through a reshuffling of royalty exposure that happens only once a decade at most and reflects the world’s changing demand patterns.

All phases are largely complete and the company is now in the cash harvesting phase of investments made over the last 10 years. The Ecora of 2030 will look completely different than the Ecora of today.

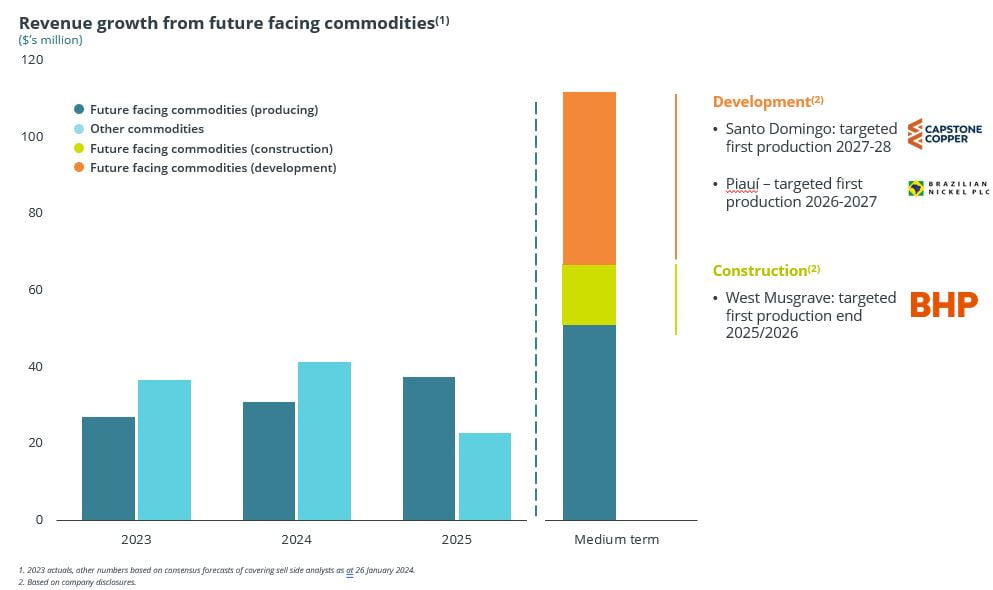

Contribution from Copper, Nickel, Cobalt and Uranium assets are expected to drive a doubling of revenue in the medium term.

Revenue Growth Outlook by Type of Commodity

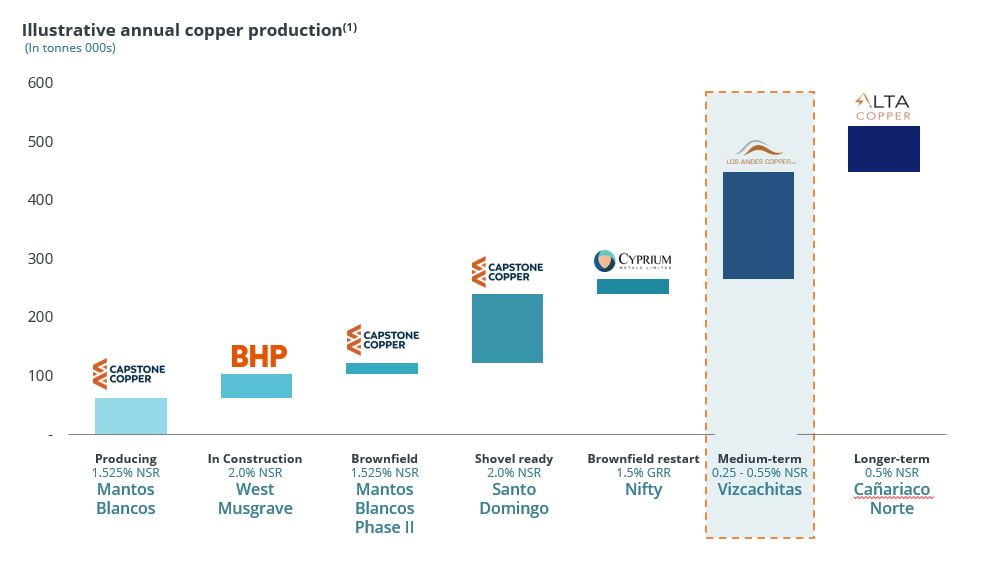

Ecora has a particular focus on copper due to the fact it plays a critical role in all the renewable energy technologies of the future.

The company has royalties on less than 100,000 tonnes of copper at the moment but will be generating revenue on over 550,000 tonnes of production by the end of the decade.

Production Outlook of Copper Royalty Projects

The Importance of a High Quality Team Behind the Scenes

Marc discussed his long history building the royalty portfolio that will shepard Ecora into the next decade. He has now handed off investment duties to a team with similar levels of experience doing deep due diligence on mines across the commodity spectrum.

Ecora’s team has strong industry relationships gained from years of doing deals. This helps them get a first look at royalty opportunities and potentially negotiate more favorable terms.

On copper in particular the team focuses on the quality of the ore body overall and second to that the probability the project will see the light of day. The ability to do this comes from years of analyzing projects all over the world and by becoming a student of history. The team studies past failed and successful projects to figure out what the key determinants of project success look like.

Marc also mentioned that while now may be a more difficult time for commodity companies to raise funding, it is a very attractive time to put money to work. Demand for copper, nickel, cobalt and uranium are accelerating, while prices are trading down or sideways. In the near future the market will realize the coming risk of supply shortages and the prices and activity in these commodities is forecast to increase significantly.

A Transition Underappreciated by the Market

Ecora is right in the most acute segment of their commodity transition curve. Falling revenue from coal is masking significant investments and future revenue from commodities with strong demand outlooks.

Because of all the moving parts, investors are having trouble correctly valuing the future cashflow potential of the business, an opportunity for anyone who is willing to do the work to truly understand the Ecora story.

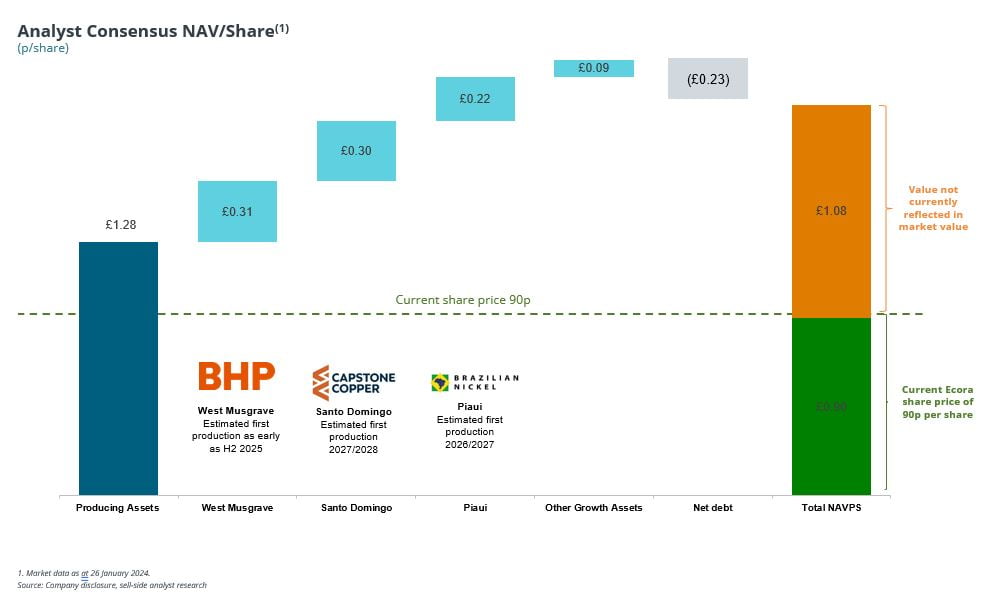

Ecora currently trades for £0.75, a 60% discount to the consensus value of the royalty portfolio. On top of that, the market is giving the company £0.09 of value for most of the growth portfolio. This growth portfolio includes Vizcachitas, a copper project with 4 times the production potential of West Musgrave, a project currently being valued 3 times higher than the entire growth portfolio.

It certainly seems like Ecora has an opportunity to better educate the market on its true potential as a royalty company highly levered to the commodities of tomorrow.

Ecora Discount to Consensus NAV (£0.90/sh)

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.