That a mass roll-out of vaccines is now on the horizon, on a six-month view, remains a reason to stay focused on the cyclical “back to normal” trade; though there is an obvious growing tension from a market standpoint with a continued rise in Covid cases and deaths in the US.

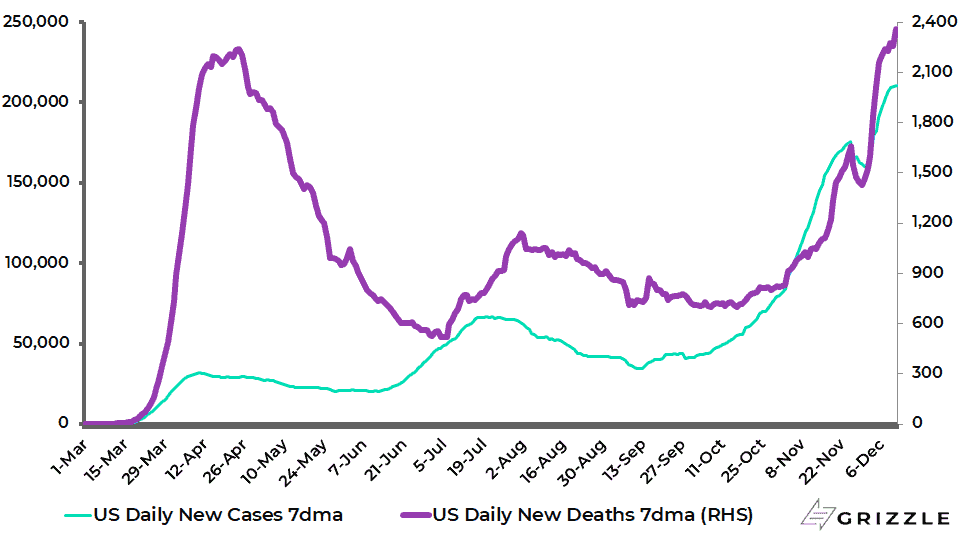

The 7-day average daily Covid new cases and deaths have risen by 31% and 61%, respectively, so far in December to a new record high of 210,765 and 2,360.

US Covid-19 7-day Average Daily New Cases and Deaths

Vaccine news aside, the G7 central banks remain decidedly committed to the doveish approach providing further support to the cyclical trade.

Consider a speech by ECB President Christine Lagarde at the ECB’s virtual Sintra conference last month.

The speech marks a further defence of the growing convergence of fiscal and monetary policy.

This may be to be expected from a lady who remains essentially the Eurozone’s unofficial finance minister in waiting.

Still, it is also of note given that monetary financing of governments is technically against the founding rules of the ECB.

Thus, Lagarde said

She also stated that “concerns about ‘zombification’ (i.e. zombie companies) impeding creative destruction are misplaced” without, of course, saying why.

The above is why it was no surprise when the ECB announced a further increase in its so-called Pandemic Emergency Purchase Programme (PEPP) at the ECB monetary policy meeting last week.

The ECB decided on 10 December to increase its asset purchases under the PEPP by €500bn to a total of €1,850bn, while extending the horizon for net purchases under the PEPP from the end of June 2021 to at least the end of March 2022.

The PEPP is a “temporary” asset purchase programme of private and public sector securities initiated in March when the pandemic hit.

The ECB’s actions, and as also suggested by Lagarde’s rhetoric, will encourage governments to continue to run sizable budget deficits, while at the same time sending the signal that the ECB government bond buying will absorb much of that debt issuance.

Still, some European governments have been less fiscally expansive in response to the pandemic because they understandably did not think they had the same room for manoeuvre.

After all, it was not so long ago that Berlin and Brussels were demanding that Eurozone governments meet the arbitrary Maastricht Treaty criterion of a maximum fiscal deficit of 3% of GDP.

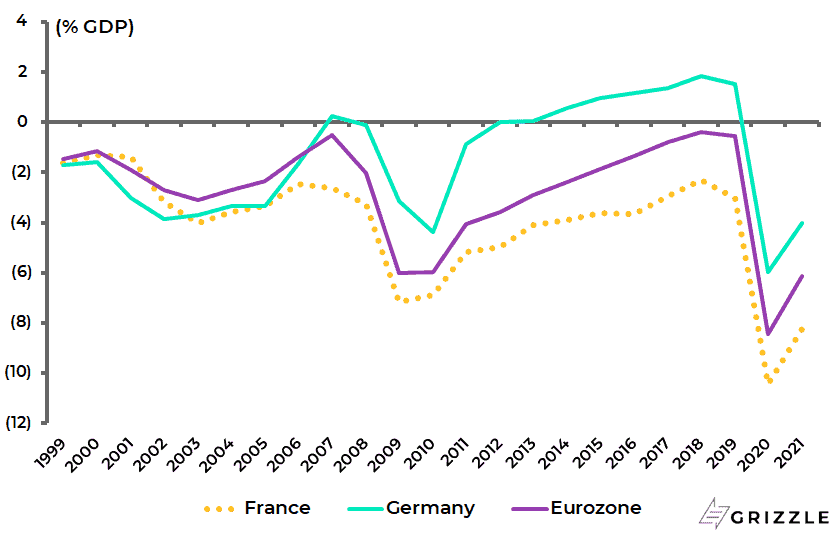

That has now been abandoned with Germany expected to run a fiscal deficit of 6% of GDP this year and France 10% of GDP.

Eurozone, Germany and France Fiscal Deficit as % of GDP

Still, the ECB is technically not meant to own more than 33% of a government’s outstanding bonds under its earlier public-sector purchase programme (PSPP) which began in March 2015.

Still, such constraints do not apply under the pandemic-triggered PEPP, which is why the so-called capital key framework is likely to be jettisoned sooner or later.

The capital key reflects the respective country’s share in the total population and GDP of the Eurozone, and is used to calculate national central banks’ shares in the capital of the ECB.

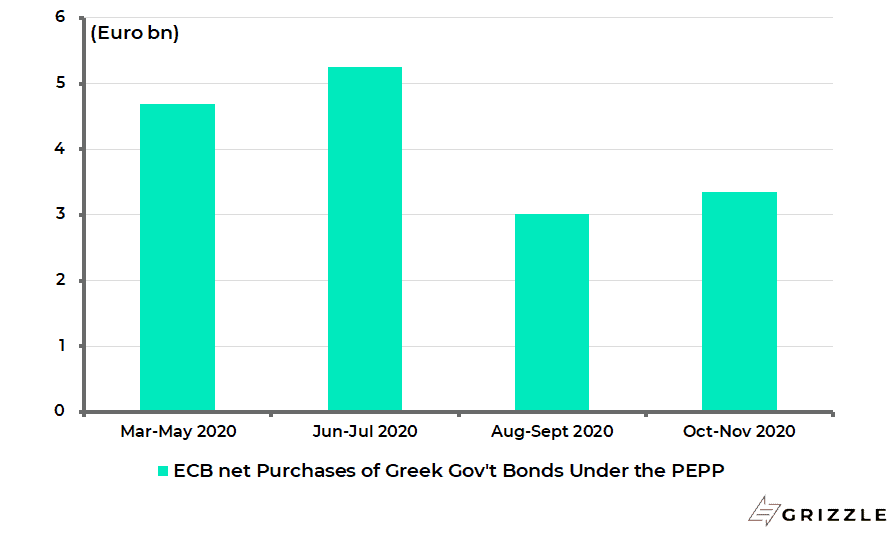

For example, the ECB never bought Greek government debt under the PSPP programme.

But the ECB has so far bought €16.3bn of Greek government bonds under the PEPP.

ECB Net Purchases of Greek Government Bonds Under the PEPP

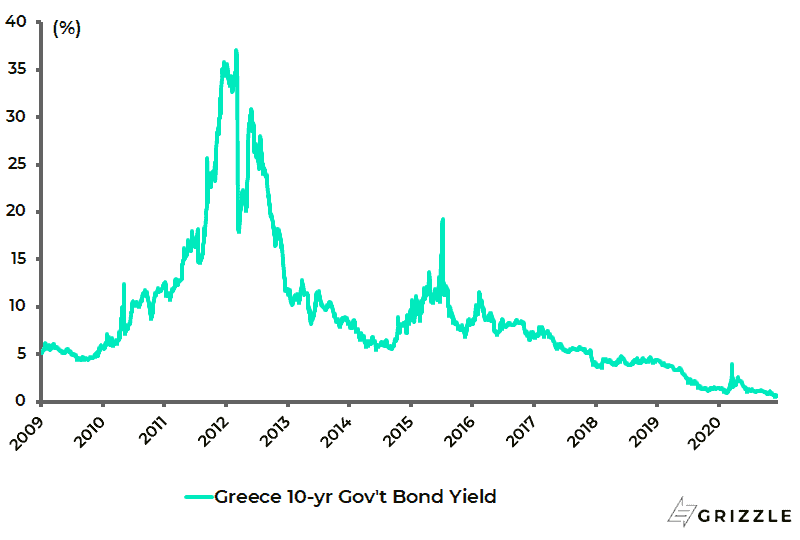

As a result, ten-year Greek government bonds now yield only 0.60%, down from 3.94% in March and a peak of 37% at the worst point in the Eurozone Crisis.

Greek 10-year Government Bond Yield

The above explains why the ECB is on the same path to monetization as the Fed.

In that context, the growing convergence of fiscal and monetary policy in the Eurozone will also be made more possible by the incremental move towards fiscal integration in the Eurozone symbolised by the proposed €750bn EU Recovery Fund which was agreed to at the EU summit on Thursday.

The key point here has been the German political establishment’s support for the Recovery Fund, a development directly associated with the political renaissance of German Chancellor Angela Merkel.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.