Southwest Airlines (NASDAQ: LUV) announced results that missed expectations unlike earnings from peers United and Delta who both beat estimates.

Revenue came in at $5.73 billion, in-line with consensus of $5.74 billion but earnings per share of $0.98 missed the consensus estimate of $1.09 by 10% and were down 16% from the same quarter in 2018.

Even with the announced reimbursement of some 737 Max costs by Boeing, this miss on earnings will likely drag down the stock today.

With the announcement Tuesday that Boeing won’t have the 737 Max cleared to fly again until this summer at the earliest, Southwest is still looking at months of higher maintenance and lost income that will drag on profitability.

Full-year revenue was up 2% compared to 9% growth in 2018 over 2017, due to higher salaries and more spending on maintenance due to the grounding of the Boeing 737 Max.

Investors won’t find much to get excited about in this release, especially with an uncertain timeline for when the 737 Max will fly again.

Like last quarter, even if the stock is up today on this earnings release, it will likely give back these gains with all of the headwinds facing the industry over the next 3-6 months.

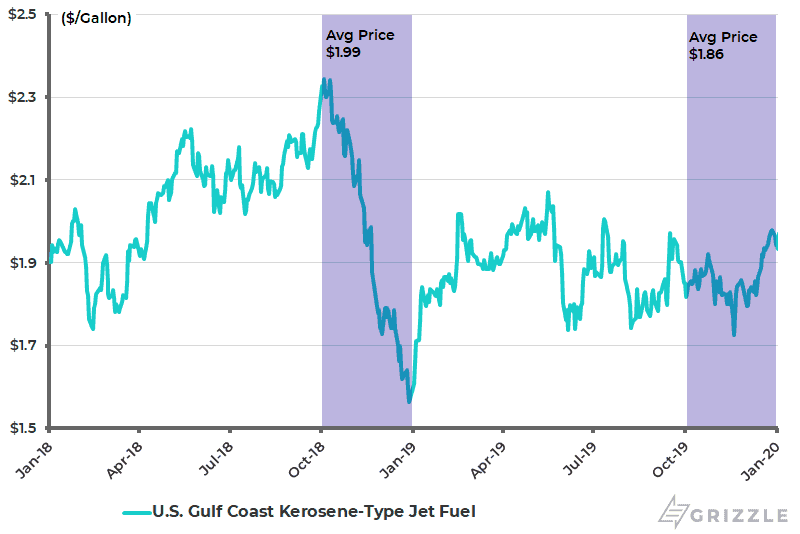

As a slight offset to the problems with Boeing, Southwest and other airline peers are still benefitting from the tailwind of lower fuel prices, with jet fuel prices down 7% compared to last year.

Fuel makes up 23% of these company’s expenses and can be a major driver of cashflow and stock price changes.

Fuel Prices Down Another 7% over Last Year

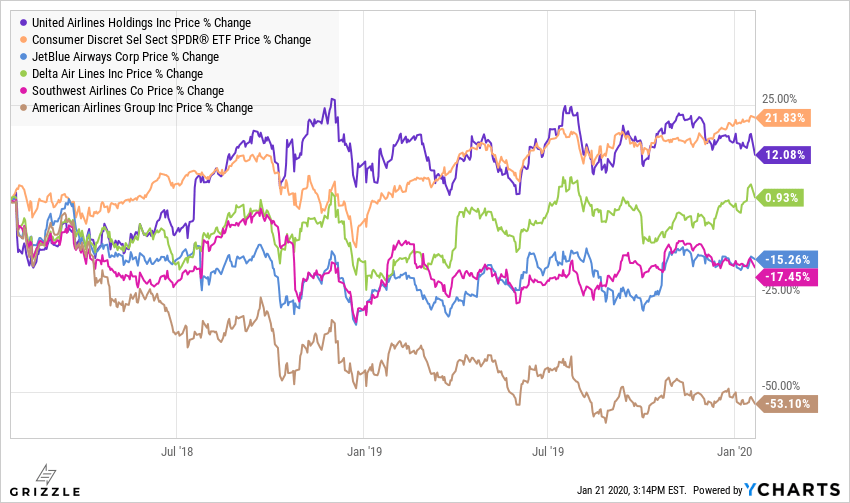

Even though airlines continue to benefit from growing consumer spending and low oil prices, the group is underperforming the consumer discretionary index by a wide margin.

Southwest has been the second-worst performing stock over the last two years likely driven by its disappointing growth and weaker than expected profitability.

Airline Stocks Continue to Underperform the Index

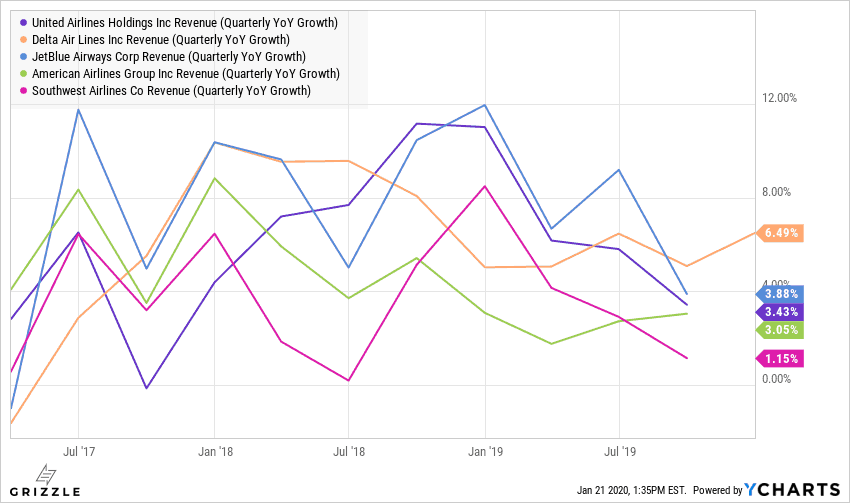

Revenue growth for the group is slowing as the oil price tailwind dissipates and issues with the Boeing 737 Max continue to drag on income.

Southwest has consistently been the slowest growing airline in the last two years.

Airline Revenue Growth

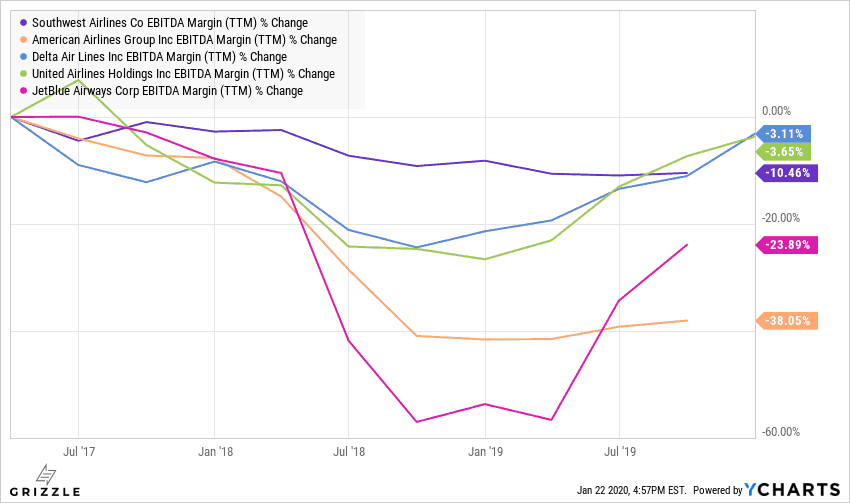

Southwest has the best profit margins of all airlines, but those margins have been falling since 2017, likely explaining why the stock has performed so poorly.

American Airlines and JetBlue have seen worse margin compression and their stocks are down as much or more than SouthWest.

SouthWest Margin Decline Driving Stock Decline

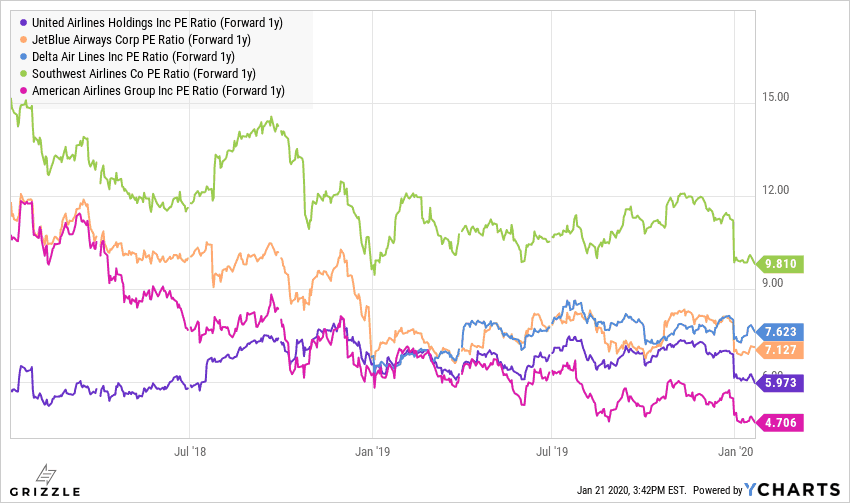

Looking at Airline P/E multiples, Southwest trades at a significant discount to the group which is likely warranted by worse growth and declining profits.

Multiples and Revenue Growth on the Decline, a Bad Combination

What to Do with Airline Stocks

With oil prices unlikely to go much lower in 2020, but consumer spending on the rise, we think airline stocks will go up with the market, but they will continue to underperform higher growth tech stocks and the consumer discretionary index as a whole.

This is a cyclical industry and we are deep into a 10+ year economic expansion.

Not to mention the industry has to deal with rising union costs, lost revenue from the grounding of the 737 Max and a softening of demand.

As if these aren’t enough headwinds, airlines are always at risk of a geopolitical situation spinning out of control, causing a spike in oil prices and taking the wind out of any airline stock rally.

You should own airlines at the beginning of an economic recovery, not at the end of an economic boom.

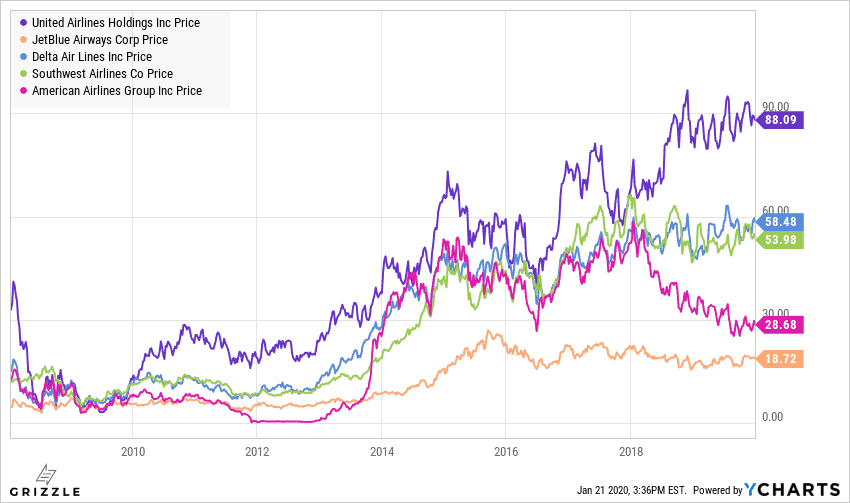

This historical price chart tells the whole story.

Airline Stocks Rebound Hard After Recessions

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.