ETFs – Homogeneous Stock Market Slosh For You

After the financial crisis the limited savings millennials tucked away (after paying off student debt) has primarily gone into the homogeneous stock market slosh of ETFs — more specifically the S&P 500 Index. The feel good circular sales pitch goes something like this: ‘everyone wins because the index always wins and we all own the index’ — it’s the we’re all fucking winners kind of participation ribbon euphoria. As Chris Wood rightly characterized in Macro Battleship, this is ETF-induced market socialism at its finest.

The Busted Boomer Brands in the S&P 500

The logical pushback is that the generic S&P 500 Index strategy has been a long-term winner so why mess with such a good thing? In blind faith, pile-on investing strategies (which indexing is) the fact that the performance run has been this good for this long is troubling in itself. The larger glaring issue is the large swathe of the companies within the index that blatantly suck — it’s an index that’s heavily weighted in outdated and broken boomer brands.

Owning broken boomer brands for the long-term is a challenging proposition for one important reason: millennial consumer trends will trump those of boomers at an ever increasing rate. As there are more millennials today than there are boomers, the weight of millennial spending dollars will only increase.

Index Fuglies: Kraft & Walmart

Kraft and Walmart are hallmark examples of the hidden brand rot inside the S&P 500 index, we’ll review the challenged proposition of both these stocks. We’re really just scratching the surface here, the list is exhaustive: Chevron, Exxon, Wells Fargo, Target ….

Kraft

Kraft is run by the wunderkinds at the private equity firm 3G Capital — they acquire shitty brands that only Warren Buffett could love and consume (eg. Burger King, Kraft), slash costs down to the bone and thus optically inflate earnings. The problems arise when revenue growth becomes nonexistent (as it is now).

In an effort to convince unhappy shareholders that growth could be found around the corner, they corralled all their garbage brands on one slide within their investor deck and unequivocally stated these are ‘unparalleled’ — like come on really? The likelihood that Kool-Aid remains a $500 million brand 10 years from now is pretty much zero.

Walmart

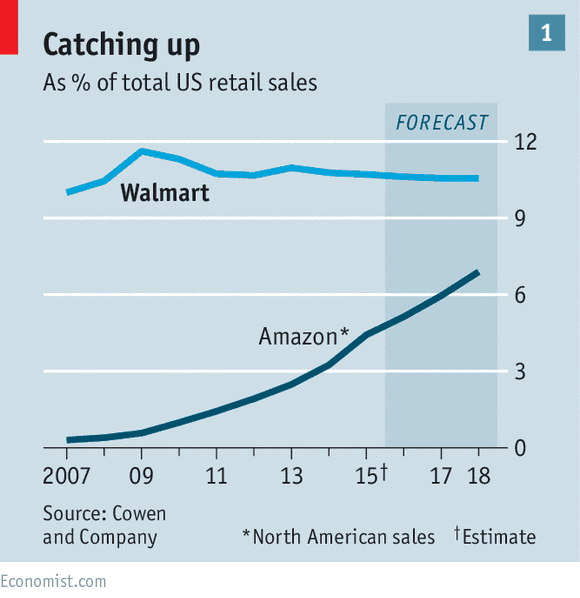

Suburban big box shopping, this is as close to dead on arrival as you get in retail, this is Walmart. When your traditional business model is in decline and your online presence is ‘jet.com’, sometimes it’s best to just say truth out in the open and cross your fingers. Neil Saunders, GlobalData Retail managing director, did exactly that for investors:

Since the market bottom (February, 2009), Walmart has underperformed the S&P 500 by a mind boggling 180%. The following chart shows the stagnating level of Walmart sales as a percentage of all US retail sales over the last decade, while the online shark (Amazon) has kept circling its prey…

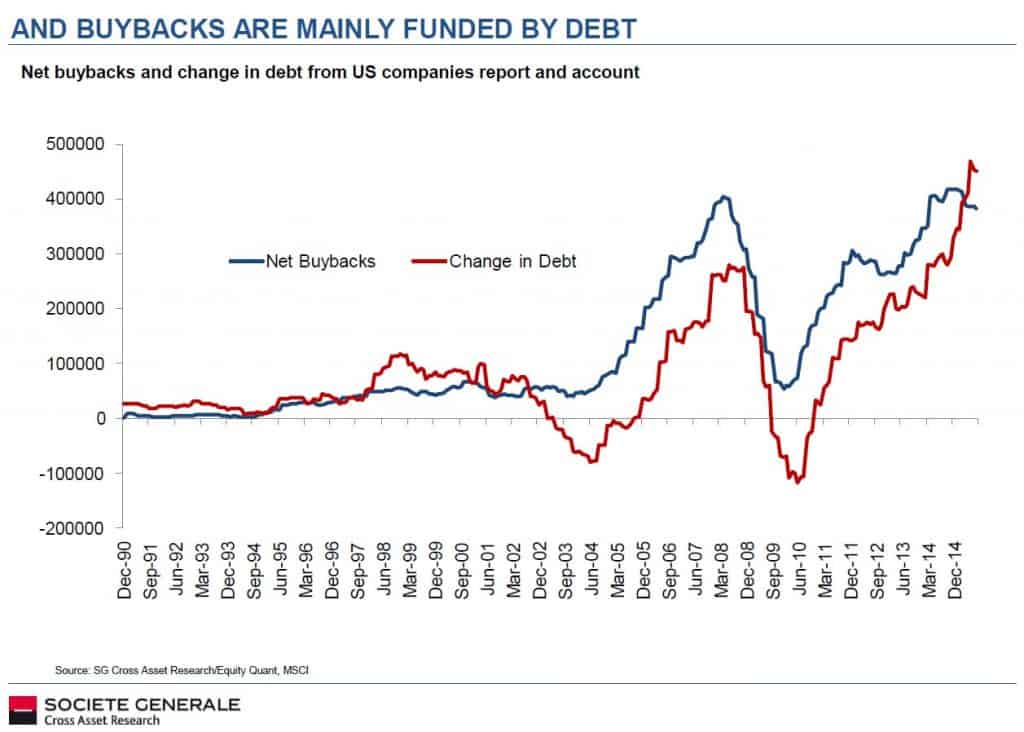

Buybacks are the Botox Injections for These Ugly Brands

Companies that aren’t as pretty as the high-flying growth stocks (Google, Amazon et al) have historically purchased their own shares (buybacks) to prop up their share prices and enhance earnings per share (through share count reduction), and they’ve always done it by issuing debt.

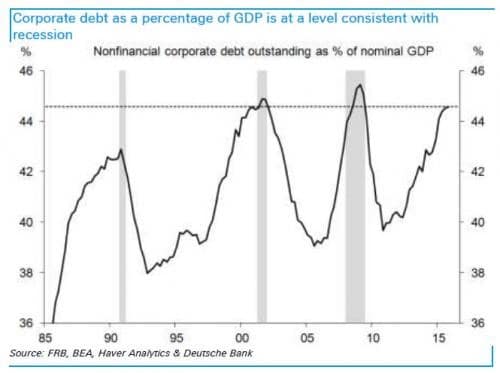

The buyback orgy has been so prolific over the last 10 years that total US corporate debt as a percentage GDP is back at ’08 financial crisis levels (~45%).

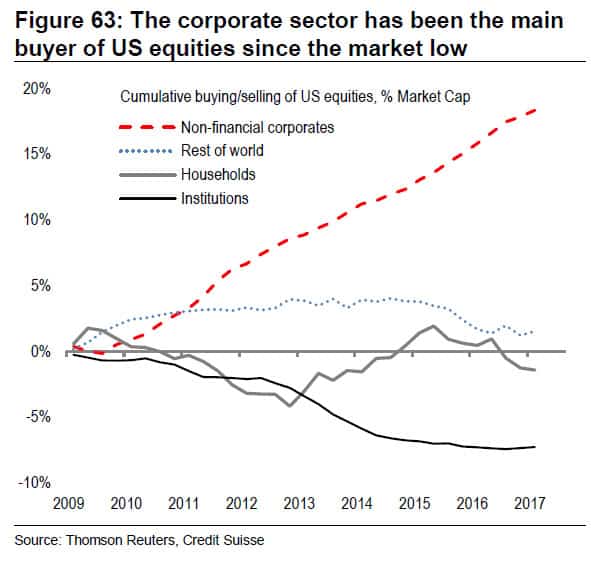

More troubling is the chart below, which shows corporations as the main buyers of their own stocks (US equities) since the financial crisis. All other categories (rest of world, households, institutions) were either flat or net sellers.

In a recessionary environment the unravel of all of the above will be messy to say the very least, having no financial flexibility because of all the debt they’ve taken on to buyback shares, the next logical step for these cash-strapped companies in a recession, well you got it, is to issue shares!

Buybacks Amplify Income Inequality

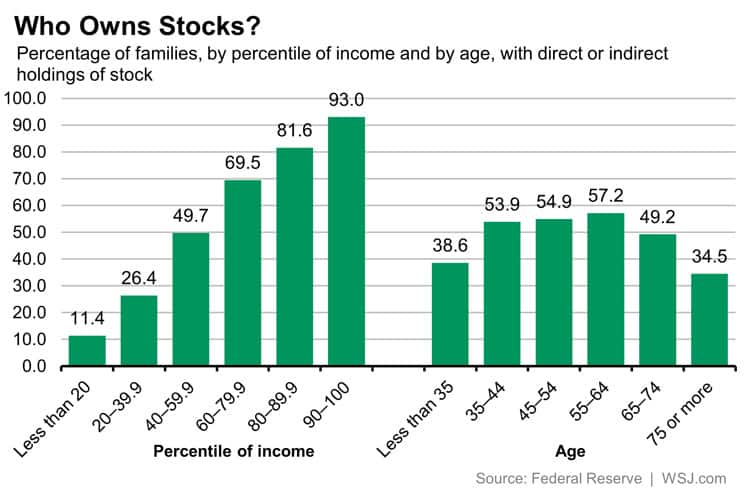

The purpose of buybacks is to increase the underlying share price of the stock. By definition this increases the wealth of those that own stocks: rich boomers.

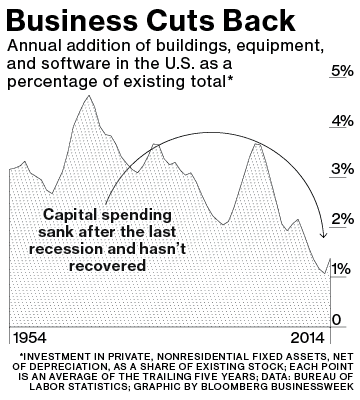

Corporations have been so laser focused on financially engineering earnings growth through share buybacks that the concept of actually investing in their underlying business (see following chart) has become an entirely foreign concept. The lack of capital investment in their businesses directly impacts the job prospects (or lack thereof) of the working class.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.