The age of “hyperconnectivity” has made data a new commodity for consumer-focused businesses. The proliferation of smartphones, wearables, artificial intelligence, and internet of things (IOT) is placing a premium on data analytics to reveal important insights about consumer trends. “Big data” has become a strategic imperative for many businesses looking to make sense of machine-generated data. And there are numbers to back it up.

According to research from Statista, big data spend eclipsed $43 billion in 2018 – a figure expected to reach $103 billion in just eight years. Anytime you hear about a company offering “business intelligence” or “data analytics” services, there’s a pretty good chance they’re involved in big data.

Splunk Inc. (NASDAQ: SPLK) has quickly emerged as one of the most recognizable names in the big data industry. The company develops specialized software for searching, monitoring, and analyzing machine-generated data through an accessible web-style interface. The software helps businesses address their IT, security and customer service needs and can be deployed on-premise or through the cloud.

For investors, Splunk’s value metrics, stock performance, and earnings history reveal a budding company with tremendous upside in an industry that is expected to explode many times over.

SPLK: By the Numbers

Splunk’s third-quarter earnings report was business as usual for the San Francisco-based company. It reported adjusted earnings of $0.38 per share, well above forecasts of $0.32. Its revenue surged 40% year-over-year to $481 million, beating the consensus estimate of $433.3 million. That was the 27th consecutive quarter the company exceeded its guidance.

Fourth-quarter results, which were released Thursday, were nothing short of spectacular. Splunk reported adjusted earnings of $0.93 on revenue of $622 million. That’s a year-over-year gain of 35% and well above the consensus forecast calling for adjusted earnings of $0.76 per share on revenue of $562.5 million.

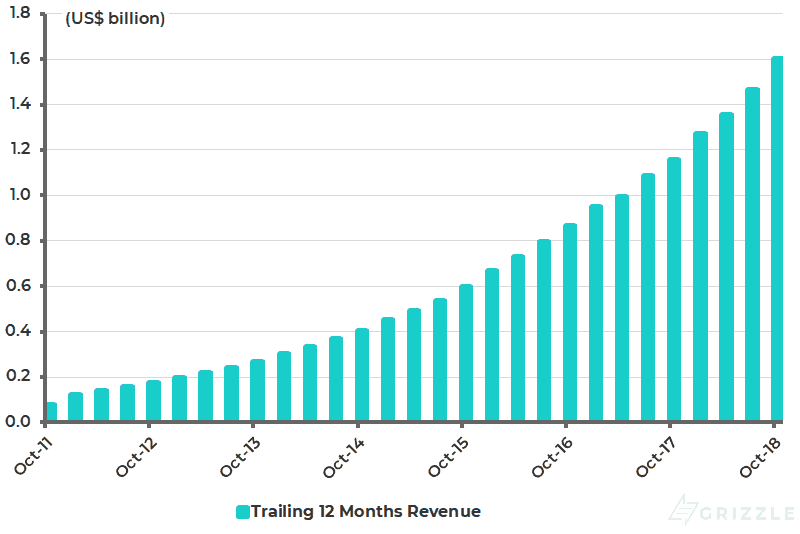

Annual revenues have continued to grow for each quarter stretching all the way back to 2011. The company also raised guidance for fiscal 2020 and now expects sales to reach $2.2 billion for the year.

The company onboarded more than 500 enterprise clients in the third quarter, chief among them being Jabil, Norfolk Southern, Softbank (Japan) and Australia’s Department of Homeland Affairs. By 2017, Splunk had more than 13,000 customers, including 90 of the Fortune 100 companies.

Splunk employs more than 4,000 workers across various locations around the world, including the Middle East, Asia, Australia, and Africa — all this despite being only 15 years old as a corporation.

Treading the Floods

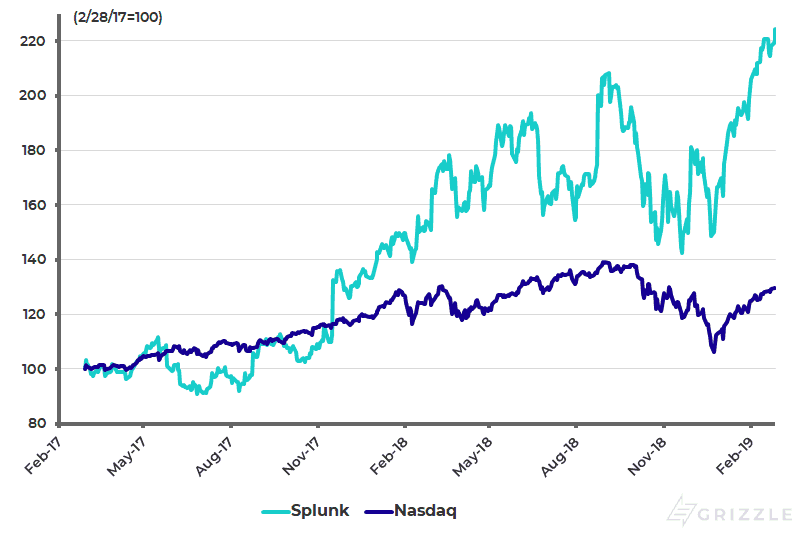

You may be thinking, so what? Technology stocks routinely outperform their counterparts during bull markets. Well, a comparison of SPLK against some of its peers and the Nasdaq Composite Index as a whole reveals market-beating returns across virtually every time frame.

The following chart compares SPLK’s performance against the Nasdaq Composite Index over the past two years. Splunk has not only outperformed the Nasdaq during the latest recovery but has returned a whopping 128% in the last two years compared with 28% for the Nasdaq.

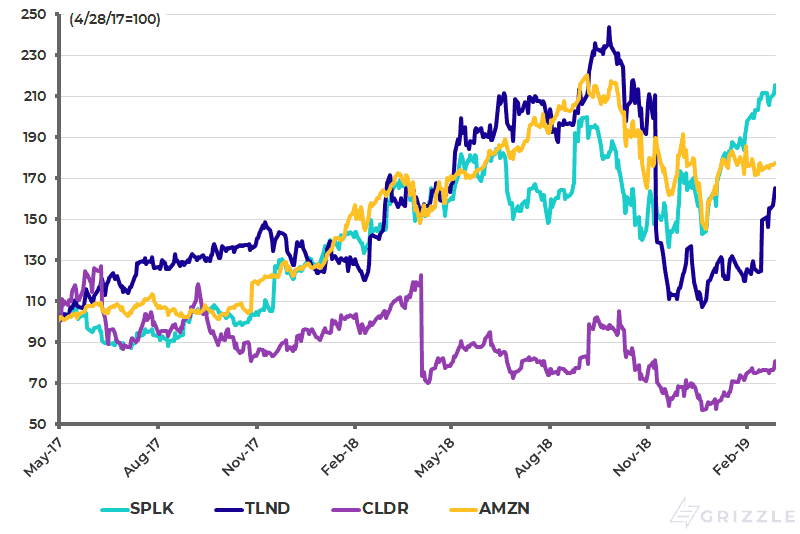

SPLK has also outperformed many of its technology and big data peers over the past two years. The following chart compares Splunk’s share price against emerging big data players like Talend (NASDAQ: TLND), Cloudera (NASDAQ: CLDR), and e-commerce juggernaut Amazon (NASDAQ: AMZN), where you can see Splunk has even surpassed Amazon’s 92% growth.

Clearly, Splunk has managed to maintain its leadership pace amid fierce competition for big data services from newer and more established tech brands. Combined with impressive guidance and strong industry fundamentals, the company appears poised to continue on its impressive growth trajectory. Splunk will remain in the driver’s seat so long as businesses continue to converge on data. Since we are on the cusp of the IOT revolution, that appears to be a foregone conclusion.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.