Tactically, the benefit of the doubt has been given here to the resumption of the stock market rally in the U.S. and a re-test of last year’s double top in the S&P500. That is despite the seemingly negative signal of the inversion of the yield curve late last month.

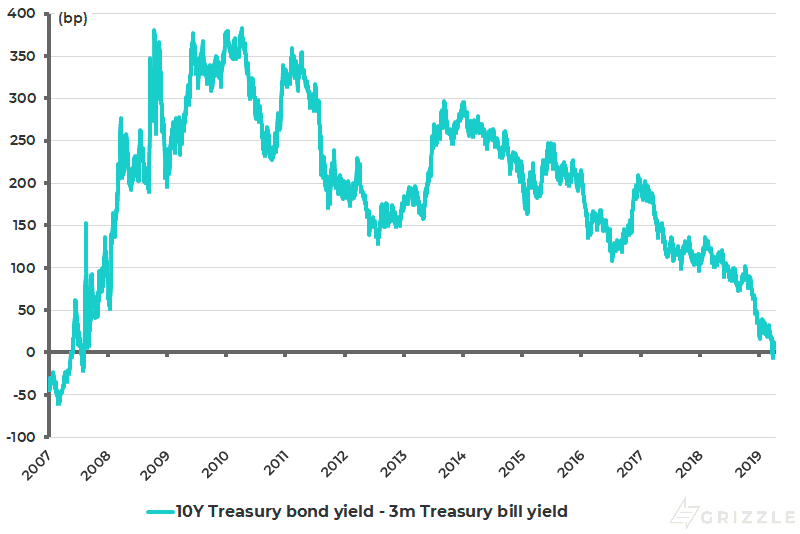

The 10-year Treasury bond yield fell below the three-month T-bill yield on March 22 for the first time since 2007 (see following chart). The spread declined to a negative 5bp on March 27 though it has since risen to 8bp on April 5.

U.S. 10-year Treasury bond yield spread over 3-month Treasury bill yield

Will the Donald Score a Deal?

The base case here remains that a Sino-US trade deal will be agreed and the positive news here is that the two sides continue to talk. Still for a deal to happen will require the Donald to tell his chief trade negotiator, U.S. Trade Representative Robert Lighthizer, to dilute his proposed monitoring and enforcement mechanism. Too aggressive an approach on the enforcement front will be a deal breaker from Beijing’s standpoint.

Meanwhile, the Donald’s room for manoeuvring to “make a deal” has undoubtedly been improved in late March by what must have been the most satisfying week of his presidency personally. That is the Mueller inquiry’s failure to make a case that he “colluded” with Russia during the presidential campaign. And it was presumably not for want of trying given the 22 months this inquiry was in existence.

Instead, the inquiry generated a lot of mostly gratuitous noise on the activities of the private side of Trump’s businesses. If the Democrats are smart, they will “move on” and focus on issues of more concern to the electorate. But that is probably wishful thinking.

Tightening Could Be a Possibility

With money market futures now signalling rate cuts in both 2019 and 2020 and the Fed having changed its stance much more dramatically since the start of this year than justified by the actual U.S. economic data, there is an obvious risk that the American central bank is now whipsawed by the markets. The Fed funds futures are discounting a 25bp cut this year and another 25bp rate cut in 2020.

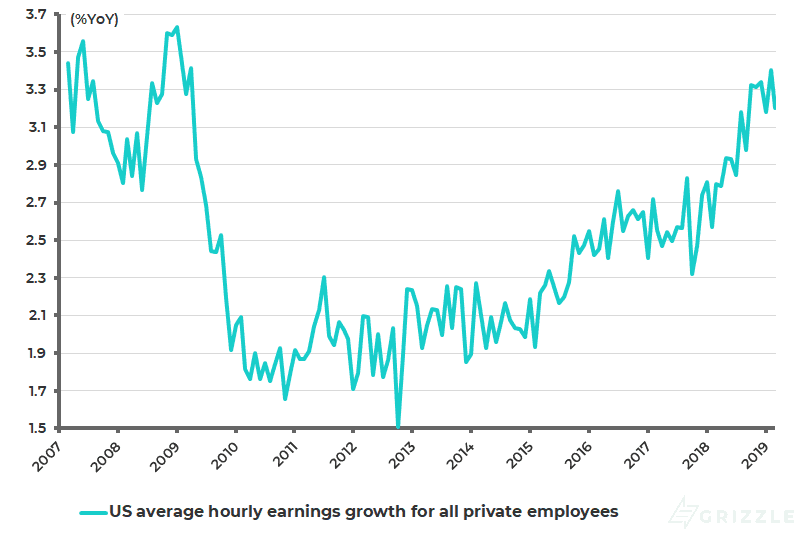

All it would likely take for U.S. tightening expectations to come back into money markets would be a successful trade deal, which I would define as one where existing tariffs are dropped, and a continuing pick up in U.S. wage data. On this point, the latest wage data released on Friday showed that U.S. average hourly earnings growth slowed from 3.4% YoY in February to 3.2% YoY in March (see following chart).

US average hourly earnings growth for private employees

Stocks Testing New Highs

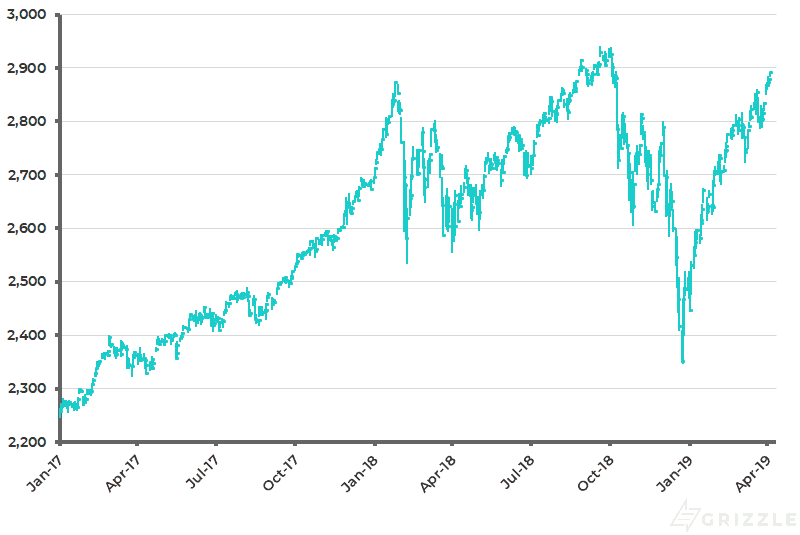

The S&P500 is now in the process of testing last year’s highs. The S&P500 closed last Friday 1.6% below the late September/early October 2018 highs but already 0.7% above the January 2018 high (see following chart). But a further rally from here means the stock market is likely to be “capped” by a resumption of monetary tightening expectations and in such circumstances a likely stronger U.S. dollar. This is why there is a much greater likelihood of an only temporary resumption in tightening expectations than an actual rate hike in the U.S.

S&P500

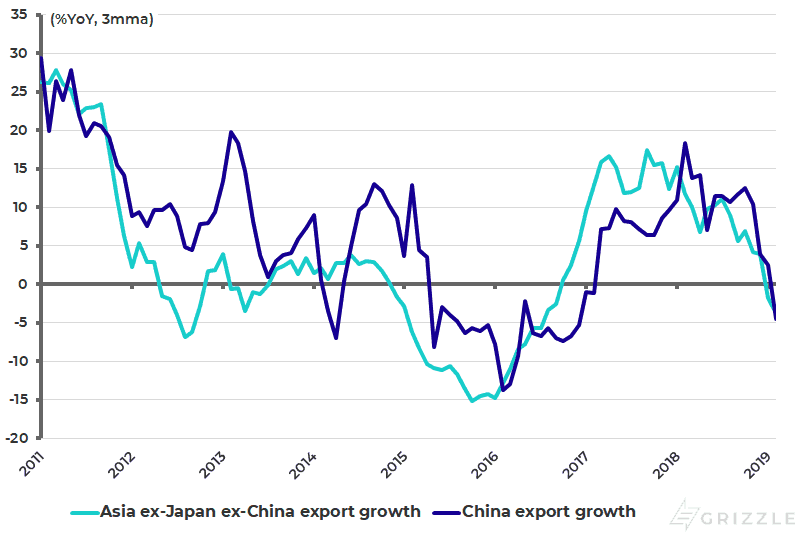

If the view on the trade deal is wrong, and there is a total failure to reach an agreement, then there is plenty of downside risk for stock markets from current levels. After all, there is scant sign, as yet, of Asian export data having improved.

Asian exports, excluding Japan and China, declined by 4.3% YoY in January-February, compared with a 7.3% YoY growth in 2018 (see following chart). In this respect, there is a tricky issue of how much the recent weakness in trade-related data has been caused by the trade dispute and how much by normal cyclical factors. There is certainly an element of cyclicality, for example the 30% decline year-to-date in DRAM prices caused primarily by the sharp decline in data centre capex. Interestingly, this is the first DRAM cycle driven primarily by a capex cycle, not by demand for a consumer durable, be it a personal computer, laptop, or smartphone.

Asia ex-Japan ex-China export growth in US dollar terms

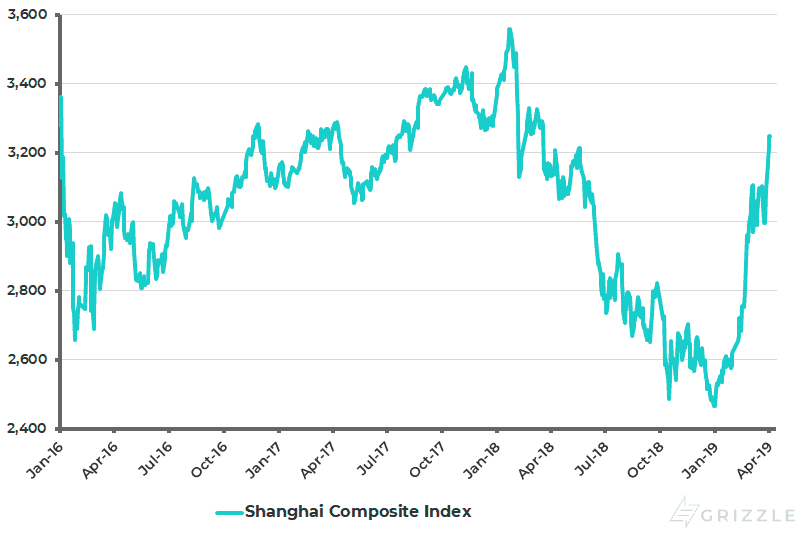

Meanwhile, I remain constructive on Chinese equities and advise investors to add on pullbacks. The key driver of the rally in the Shanghai market this year, already up 30.2% year-to-date on the Shanghai Composite Index, has been a growing realization that deleveraging pressures peaked out late last year in the mainland economy. As a result, there has been a significant decline since late last year in the total value of pledged shares due and corporate bonds refinancing. It was this combination of rising pledged shares and a related surge in bond refinancing which proved so lethal for A-shares in 2018, when the Shanghai Composite Index declined by 24.6% (see following chart).

Shanghai Composite Index

Meanwhile, Chinese equities remain much cheaper than the U.S. counterparts. Chinese stocks quoted in Hong Kong and the U.S. now trade at 9.6x 2019 forecast earnings. It is also the case that Chinese stocks quoted in Hong Kong ended the past quarter trading at a 20% discount to their Shanghai “A-share” quoted counterparts.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.