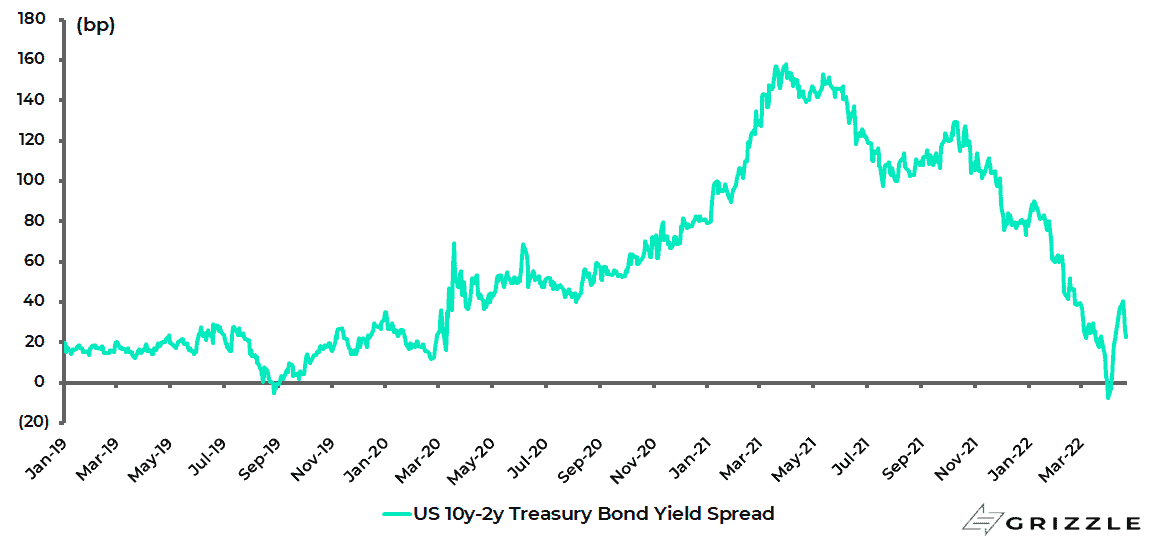

The US yield curve has flattened significantly this year, ever since the release of the Federal Reserve minutes on 5 January opened up the possibility of quantitative tightening happening much sooner than markets were positioned for.

The spread between the 10-year and 2-year Treasury bond yields has declined from 89bp on 4 January to -7bp on 1 April and is now 23bp.

Spread between US 10-year and 2-year Treasury bond yields

Still, if such market action signals a growing risk of an economic slowdown the Fed has had no choice but to start raising rates with a 25bp rate hike in March, and a likely 50bp hike in May, given the latest inflation data combined with the fact that the war in Ukraine, and related commodity price surge, has made it likely that inflation will stay higher for longer.

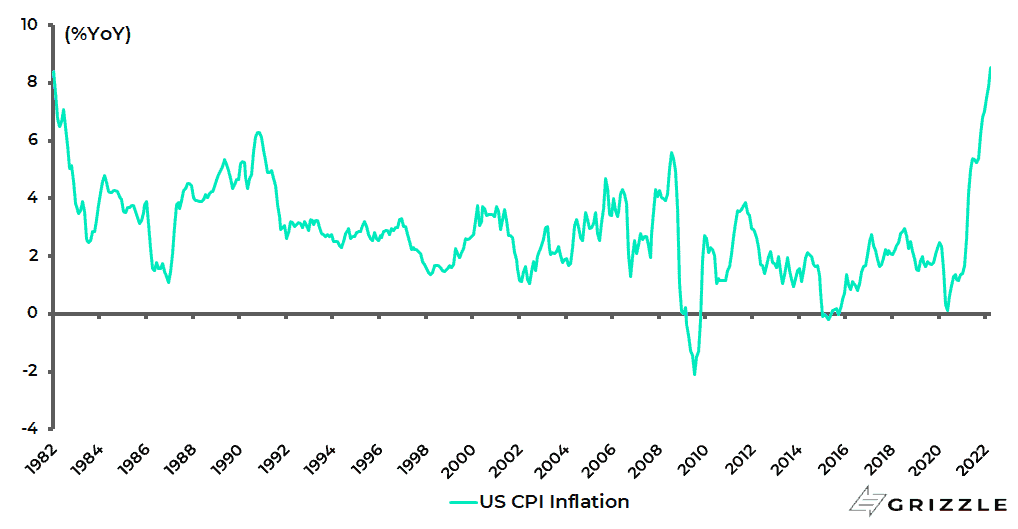

On this point, prior to the Russian invasion, the base effect meant that inflation should have peaked with the February CPI data point.

US CPI inflation

As for the March inflation data announced on 12 April, CPI was 8.5% YoY, up from 7.9% YoY in February.

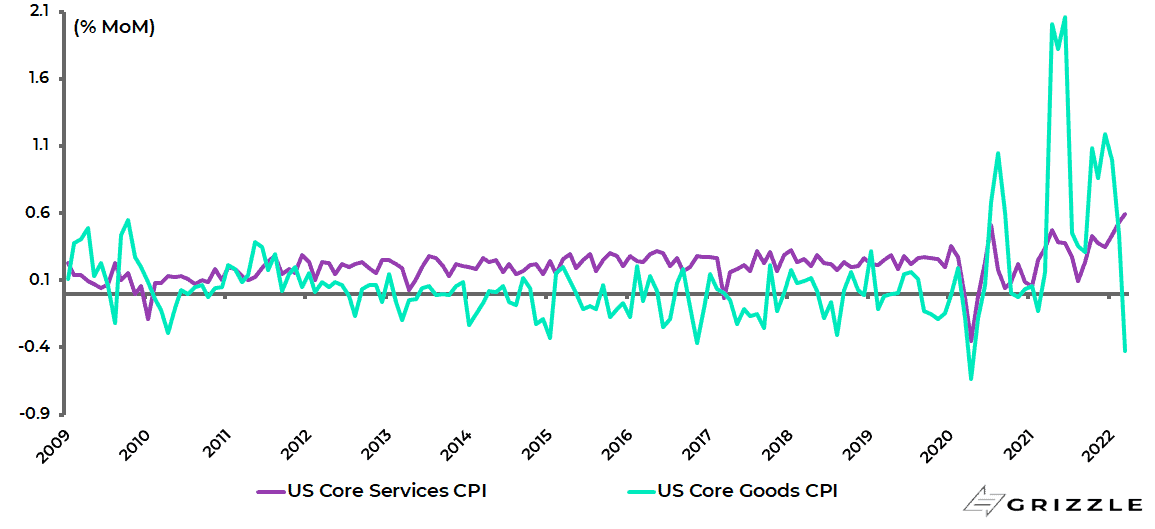

Worryingly, there is evidence of inflationary pressures shifting out of goods to more sticky services.

Core goods CPI declined by 0.4% MoM in March, the biggest decline since April 2020, while core services CPI rose by 0.6% MoM, the largest increase since January 1991.

US core goods and core services CPI inflation %MoM

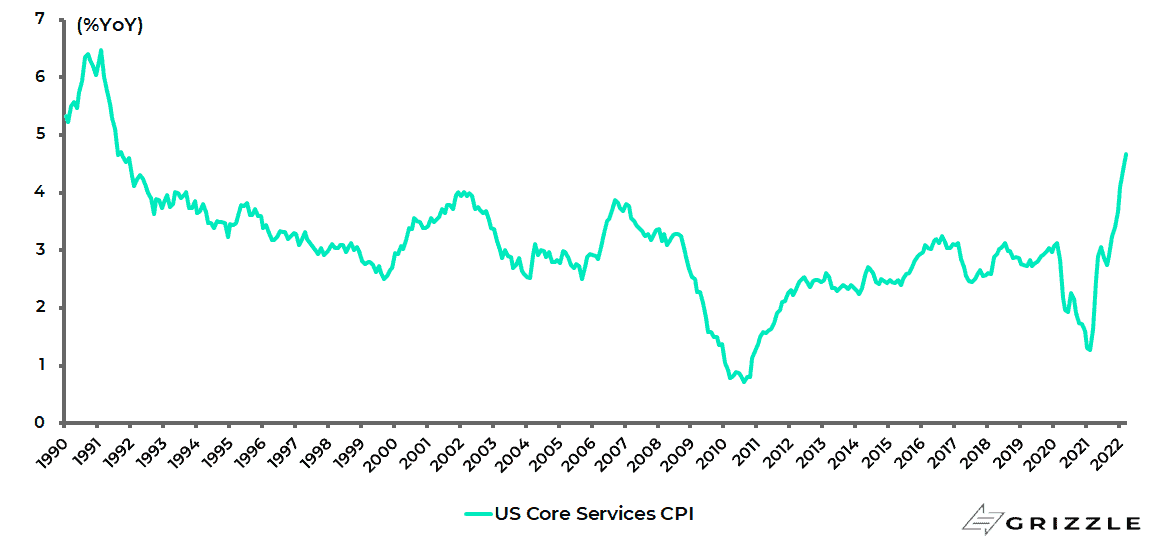

As a result, core services inflation rose to 4.7% YoY in March, the highest rate since September 1991.

US core services CPI inflation %YoY

This is potentially highly significant.

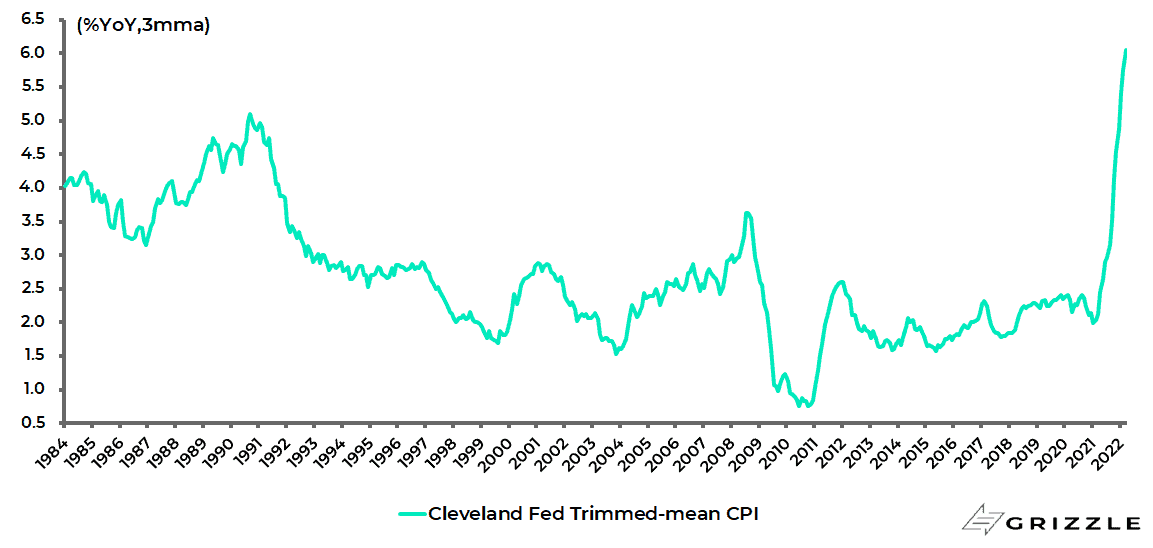

It is further the case that the Cleveland Fed’s trimmed-mean CPI also continues to send the same signal of spreading inflationary pressures.

This measure excludes the inflation components each month which have shown the most extreme moves in either an upward or downward direction.

The trimmed-mean CPI inflation rose from 5.75% YoY in February to 6.05% YoY in March, the highest level since the data series began in December 1983.

Cleveland Fed US Trimmed-mean CPI inflation

As for the labour market, the Atlanta Fed’s wage growth tracker continued to accelerate in March.

The tracker shows that US median hourly wage growth increased from 5.8% YoY in February to 6.0% YoY in March, also the highest level since the data series began in 1997.

Atlanta Fed’s wage growth tracker

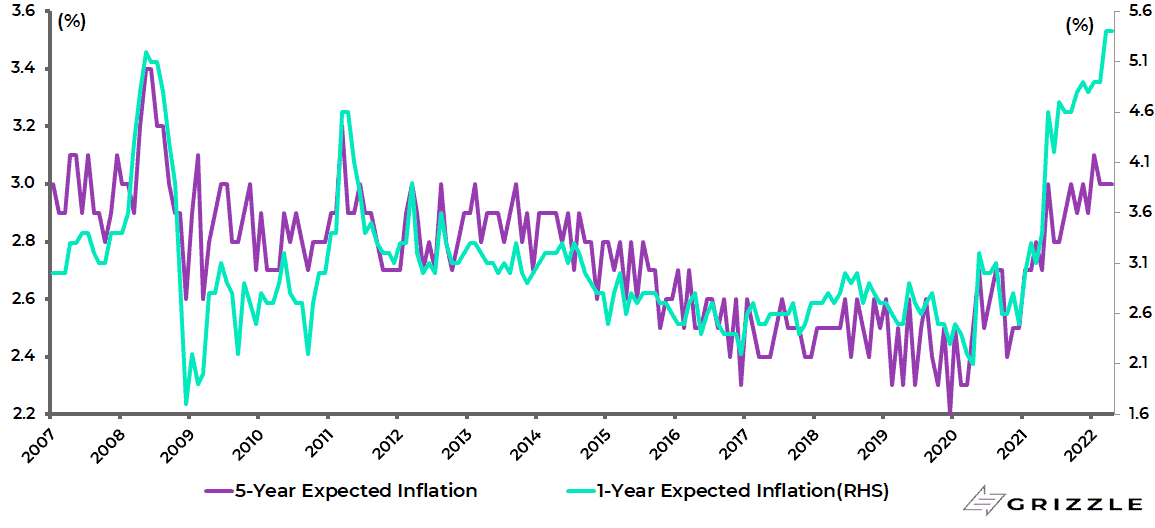

Meanwhile, the University of Michigan’s survey of consumer inflation expectations continues to rise.

The one-year expected inflation rate rose from 4.9% in February to 5.4% in both March and early April, the highest levels since 1981, while the 5-year expected inflation rate rose from 2.9% in December to 3.1% in January and was still 3.0% in early April.

University of Michigan consumer survey: 1-year and 5-year expected inflation

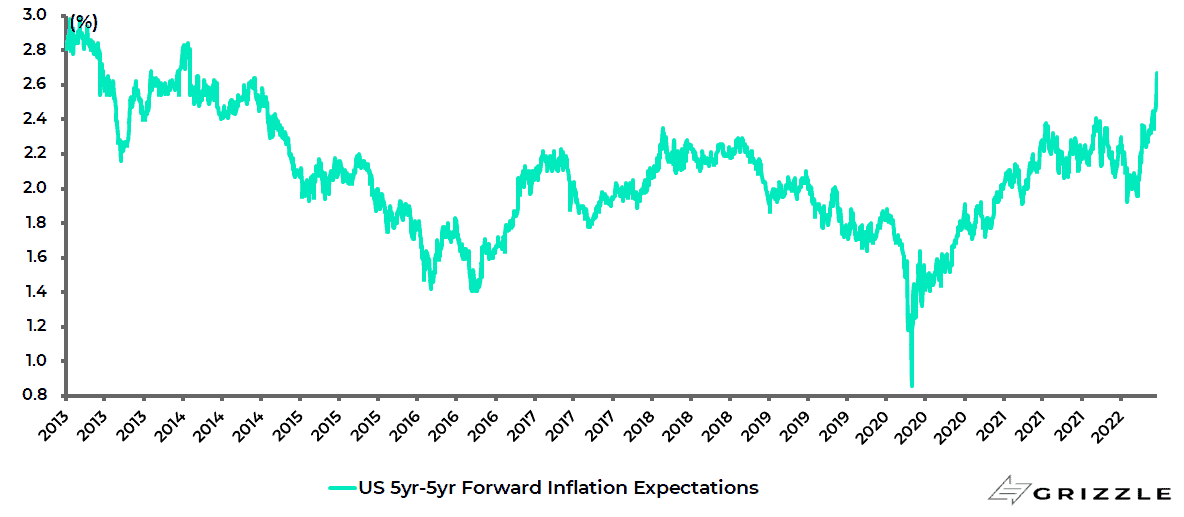

As for market-driven inflation expectations, the US five-year five-year forward inflation expectation rate has of late risen above the key 2.50% level.

It rose from a recent low of 1.92% reached in January to 2.67% on 21 April, the highest level since January 2014, and is now 2.59%.

US five-year five-year forward inflation expectation rate

Still, it remains the case that the American economy is more resilient than Europe’s given the much stronger labour market.

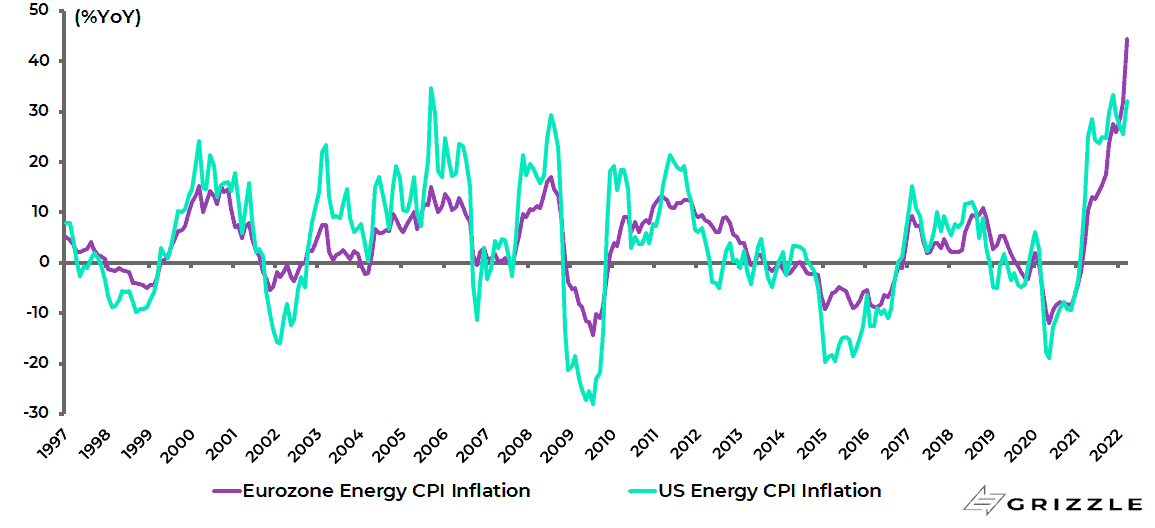

It is also the case that the energy price shock is much less in America.

Thus, US energy CPI rose by 32% YoY in March, compared with 44.4% YoY in the Eurozone.

US and Eurozone energy CPI inflation

In America, energy costs accounted for 8.29% of the CPI basket in March, compared with 10.93% in the Eurozone.

As a result, energy inflation contributed an estimated 4.9ppts to Eurozone’s headline inflation rate of 7.4% YoY in March, compared with the 2.7ppt contribution to US CPI inflation of 8.5% YoY.

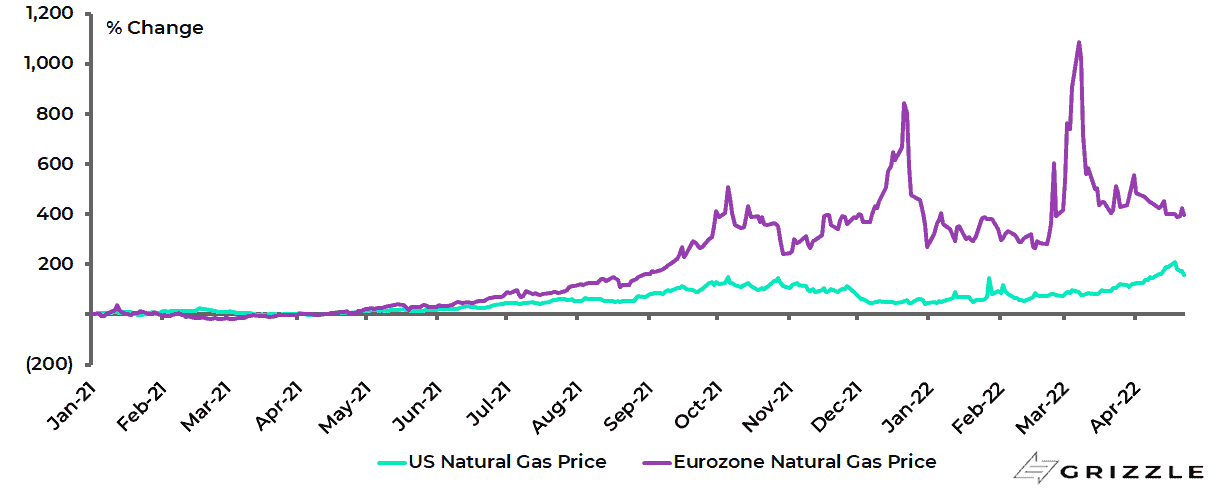

While natural gas prices in America have risen by “only” 157% since the start of 2021, compared with the 396% surge in the Eurozone

US and Eurozone natural gas prices: % change since the start of 2021

Naturally, the Biden administration has been quick to blame the surge in prices at the petrol pump on Russian President Vladimir Putin.

That may just work politically.

But this writer doubts it. The reality is that the inflation genie was already out of the bottle long before the invasion of Ukraine was launched on 24 February and opinion polls showed that Americans were already focused on the issue.

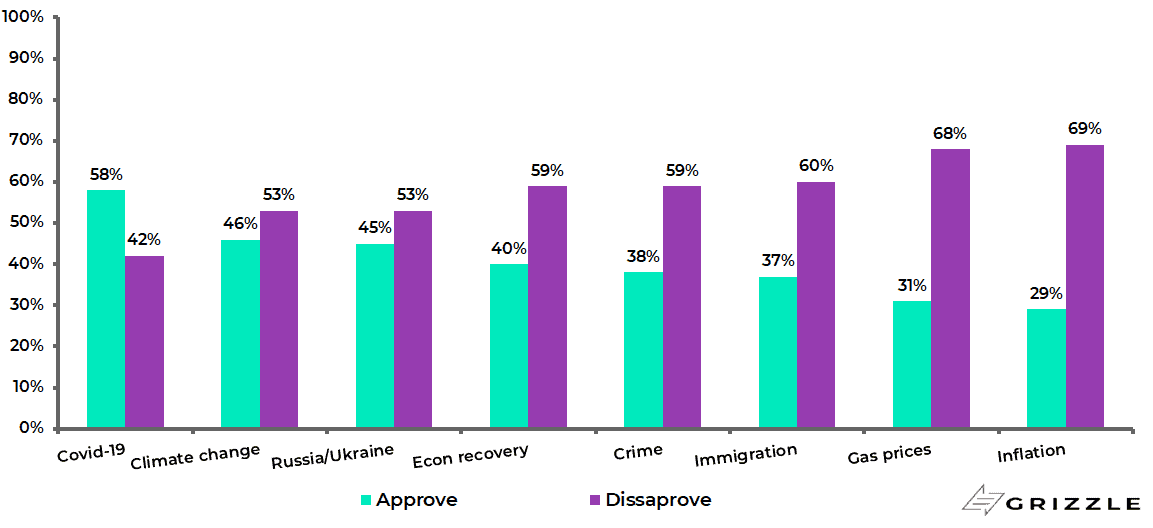

They remain so now. The latest ABS News/Ipsos poll conducted on 8-9 April, or six weeks after Russia’s launching of the invasion, showed that 69% of Americans disapprove of Biden’s handling of inflation, the same as in late January, though down from 70% in mid-March.

ABC News/Ipsos poll: Do you approve/disapprove of the way Joe Biden is handling …

All this suggests that the political pressure is still on the Fed to be seen to be doing something about rising prices. Indeed, in many respects, the Fed’s credibility is on the line.

Europe Has U-Turned on Fighting Inflation – Rate Hikes Could Begin This Year

Meanwhile, in Europe, the ECB has also done its own U-turn in terms of admitting there is an inflation problem.

The ECB now plans to end quantitative easing in the third quarter subject to the data.

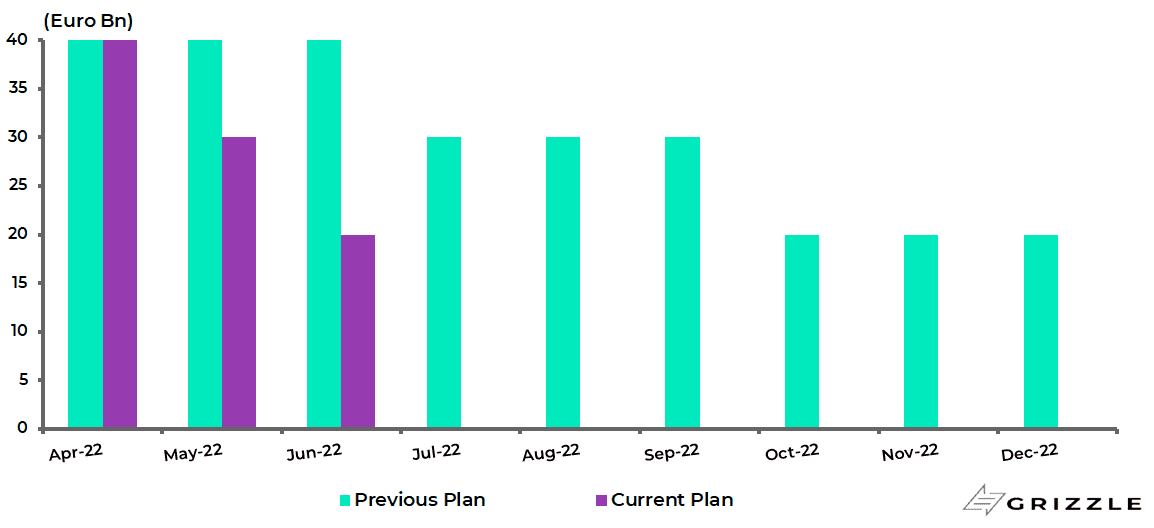

It is also the case that the pace of tapering has been accelerated. Monthly net asset purchases will decline from €52bn in March to €40bn in April, €30bn in May and €20bn in June, while net purchases in the third quarter will be ’data-dependent’.

By contrast, the previous plan was to reduce monthly net purchases to €40bn in 2Q22, €30bn in 3Q22 and €20bn in 4Q22.

ECB tapering plan: Monthly net asset purchases under the APP

That could open up the path for a rate hike in Europe before the end of this year.

The ECB’s new guidance, based on the “sequencing” approach, is that rate hikes will take place “some time” after the ending of net purchases under its Asset Purchase Programme (APP).

The continuing possibility of rate hikes, and therefore relief from the insane policy of negative rates, is a positive for European banks in spite of the growing recession risk.

The ECB’s renewed hawkishness is understandable given the dramatic surge in inflation and indeed the more dramatic surge in longer-term inflation expectations where the rise, albeit from a lower level, has been much greater than has been the case in America.

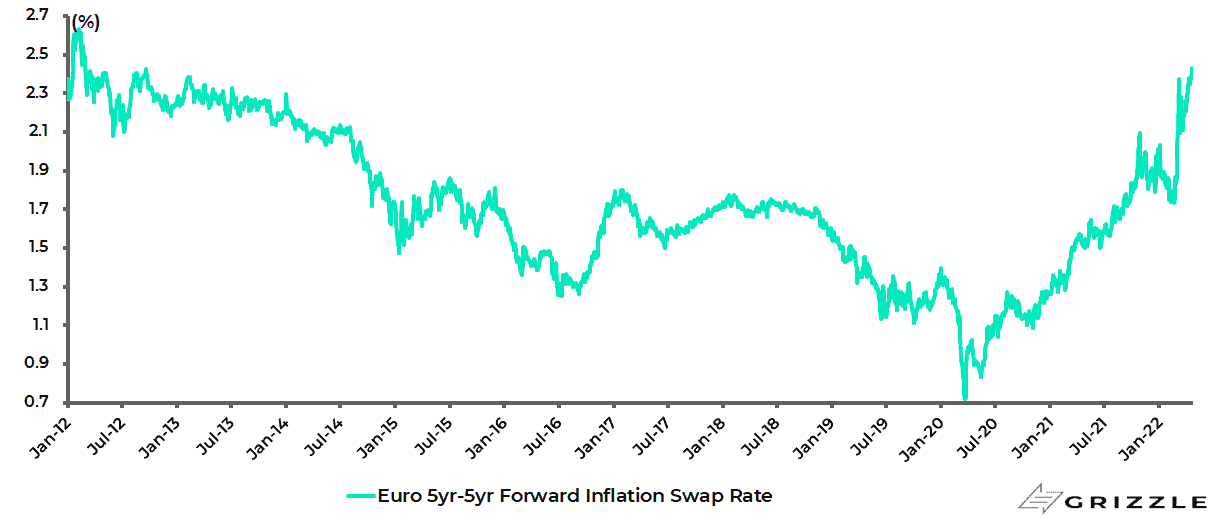

The Eurozone 5-year 5-year forward inflation swap rate has risen from a low of 0.72% in March 2020 to 2.43%, the highest level since February 2012.

Eurozone 5-year 5-year forward inflation swap rate

It is also the case that the ECB seems to be taking the view that, with fiscal policy now due to become much more expansionary in the Eurozone as a direct result of the Ukraine conflict, it makes sense to focus more on addressing inflation.

This writer refers to reported plans for the Eurozone to issue “joint” bonds to finance energy transition and re-armament.

On this point, EU leaders issued the following statement after a summit held last month in Versailles, France: “We agreed to phase out our dependency on Russian gas, oil and coal imports as soon as possible”.

They also agreed in the meeting to “increase substantially defence expenditures”.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.