Legal cannabis producer Supreme Cannabis (TSE:FIRE) reported dissapointing results.

Revenue came in at C$9 million, 10% worse than consensus of C$10.1 million.

Revenue was down 10% from last quarter and 52% from June 2019 when the company hit peak sales of C$19.1 million.

Supreme is going through a difficult transition.

Sales were too reliant on the wholesale market where pricing has collapsed and management is now trying to pivot to the recreational channel where pricing is falling as well, but more slowly.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]The transition from wholesale to retail has meant a big fall in sales, but sales in the retail channel are on the rise and are matching the growth of the overall market at 14% which is a sign Supreme is not losing market share like Aurora or Canopy.[/su_panel]

Wholesale in Decline, Recreational Sales on the Rise

The earnings loss of -C$0.05 significantly missed consensus estimates of a -C$0.01 loss.

The EBITDA loss of -C$10.4 million missed badly as well. Consensus was looking for only a (C$5.2) million loss.

Supreme’s now has an EBITDA loss of C$15 million halfway through the year, which they have to make up in the back half to meet their guidance of flat to positive EBITDA for the year.

This guidance will likely have to be cut unless sales explode in the April-June quarter.

Costs were up 9% from last quarter and even with the 15% cost cuts recently announced, costs must fall a further 40% for the company to have any hope of meeting their guidance for positive EBITDA by June.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Supreme historically had something the other large producers didn’t, good weed, however, their production and headcount is still too large for the amount of cannabis they are selling. Costs need to fall another 40% at the current level of sales for the company to generate a profit. Once costs come down this may be a stock to own for the long term, if they haven’t lost their skills in the greenhouse that is. [/su_panel]

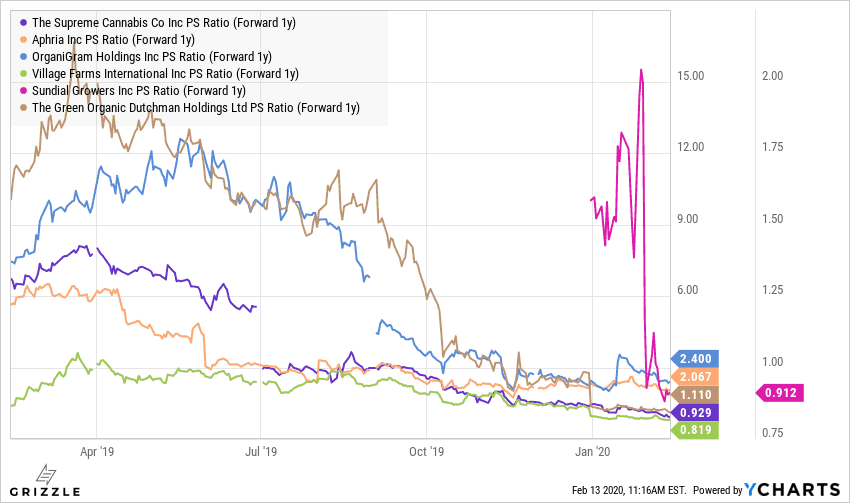

Supreme is Not an Expensive Cannabis Stock

Supreme is currently trading at about 1x sales, which is in-line with the peer group at 0.8x-1.1x.

Though Supreme looks fairly valued just on multiples, its cash position is far superior to peers.

Estimates Price to Sales Multiple of the Group

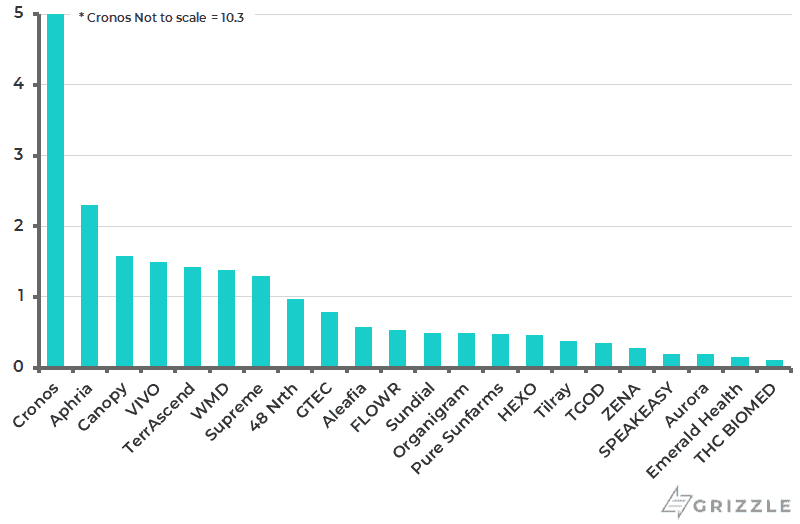

Supreme has more than a year of cash left compared to peers like TGOD and Sundial with less than six months.

Even Village Farms’ cannabis subsidiary Pure Sunfarms had only six months of cash left as of September 30th due to big spending on construction, which is eating up all the positive cashflow of the business.

Unlike larger LP’s, Supreme has time to get the transition right as they cut headcount and shift to recreational sales over wholesale.

Years of Cash Left

Even though Supreme looks undervalued, value stocks can stay value stocks for a long time without a catalyst.

Supreme will at a minimum have to show accelerating revenue growth for anyone to get interested in this stock.

But realistically, the company will have to start generating at least enough EBITDA to pay the interest expense on its debt before we can say the company is on sound financial footing.

We recommend investors wait on the sidelines until they see EBITDA approaching C$14 million annualized.

At that point, the company will be in a strong financial position and would be a bargain below $0.50.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.