Synopsys (NASDAQ: SNPS) reported fiscal Q1 2020 earnings which beat analyst estimates but slowing growth in one of the business segments has driven the stock lower after hours.

Sales for the Electronic Design Automation (EDA) firm came in at $834.4 million which beat consensus estimates of $821.3 million.

Analysts had been expecting revenues basically flat (+0.11%) to the same quarter the previous year, however Synopsys managed to grow revenues by 1.7%.

Synopsys posted earnings of $1.01 per share which came in above Wall Street expectations of $0.92 per share.

While the bulk of Synopsys’ sales comes from their EDA Semiconductor and System Design segment (90% of revenues), the company also has a Software Integrity business. That business had been the growth driver for Synopsys last year, growing revenues 19% in 2019 compared to 2018. However, this quarter growth slowed significantly with revenues up only 3.8% compared to the same quarter the previous year. The EDA segment also showed slowing growth with revenues up 1.5% year over year.

While the Software Integrity business unit had been growing revenues, margins in the business are not nearly up to par with the EDA software which is a much more mature market. Synopsys’ Software Integrity segment reported operating margins of just 9.4% compared to operating margins for the EDA segment of 23.9%.

Great point! If only someone could find ways to disrupt this… #EDA #semiconductor #electronics

— Don (@d0nweaver) February 12, 2020

The EDA market is comprised basically of 3 major players: Synopsys, Cadence (NASDAQ: CDNS), and Siemen-owned Mentor (ETR: SIE). As we discovered when we took a closer look at Cadence after their recent earnings report, business has been good for this software segment.

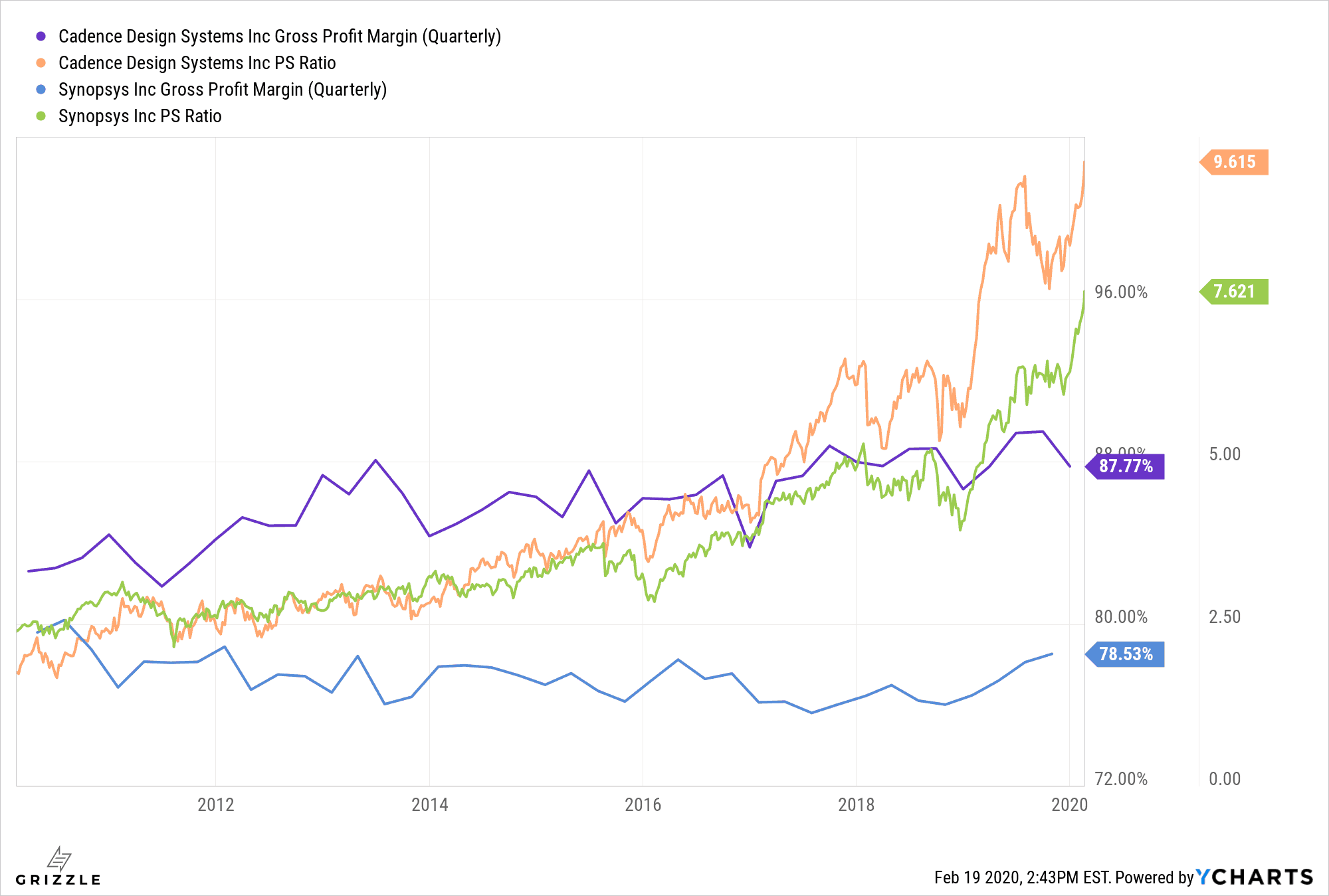

What do you get when 3 big players control a market for 30 years with little innovation or disruption? Well you get those companies printing amazing margins and appreciating PS ratios.

Synopsys stock has been on a strong run recently, growing more than 65% over 2019 and adding another 17% in 2020 thus far. In fact, the stock has outperformed that of rival Cadence by more than 10% over the past 12 months. Leading in to the earnings report the stock gained another 1.4% and after releasing earnings Synopsys stock was down 2.5% in after market trading as of the time of publishing.

Full Disclosure: The author owns shares of Cadence.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.