The coronavirus clearly represents a formidable challenge for the Chinese government. But if there is one country equipped to meet such a challenge it is probably the command economy model. Still one silver lining is that, with 50 confirmed cases in Hong Kong the health crisis has taken the immediate heat out of the Hong Kong demonstrations.

China Facing One Challenge After Another

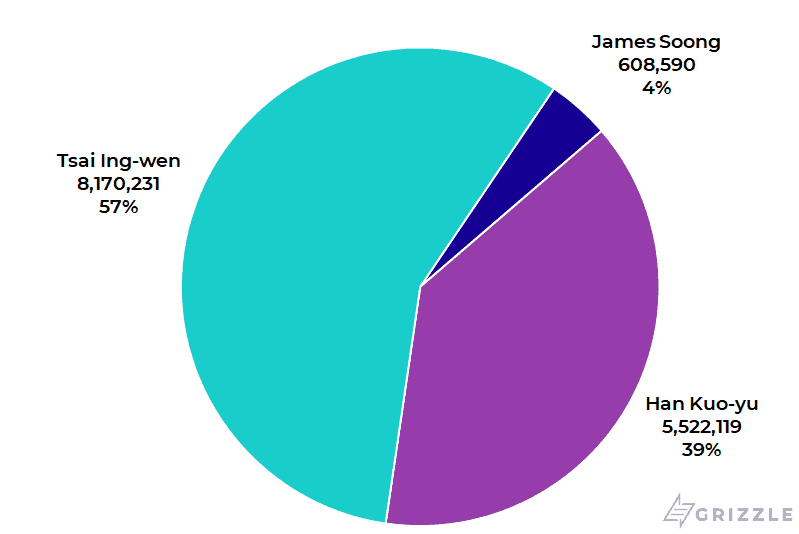

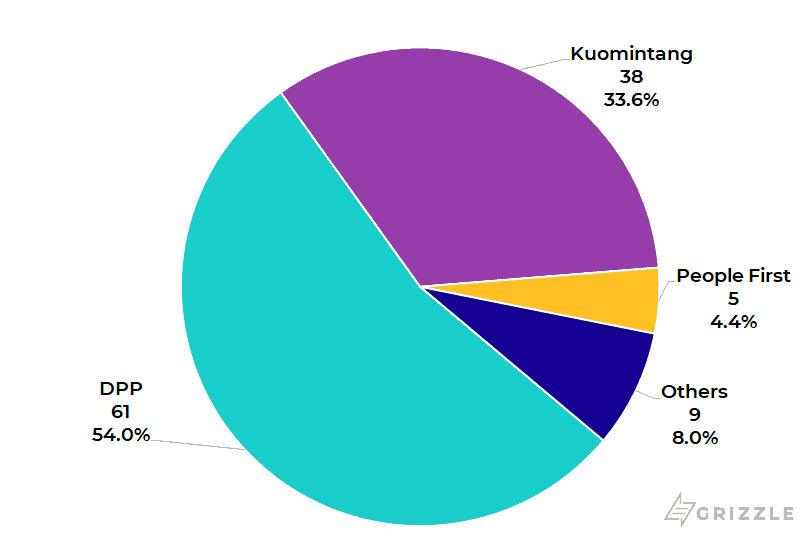

Meanwhile, from Beijing’s standpoint, the Taiwan presidential election in January represented collateral damage from seven months of street protests in Hong Kong. The Taiwan presidential and legislative elections on Jan. 11 went as expected though it is worth noting the sheer scale of the victory. Incumbent DPP President Tsai Ing-wen won a landslide 57.1% of the vote, or a record 8.17 million votes (see following chart), while the DPP won 61 seats in the Legislative Yuan ensuring continuing majority control (see following chart). Turnout was a huge 75%, up from 66% in the last presidential poll in 2016 and the highest since 2008.

2020 Taiwan Presidential Election Results (Number of Votes)

2020 Taiwan Legislative Yuan Election Results (Number of Seats)

There is no doubt that the scale of Tsai’s victory is the direct consequence of events in Hong Kong last year which have endorsed the Taiwan president’s principled opposition to “One Country Two Systems”.

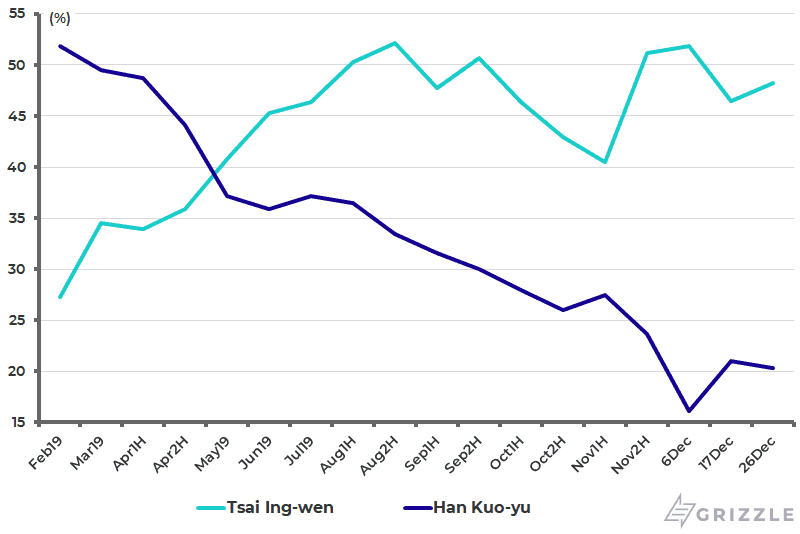

In February 2019, Tsai was running more than 20 percentage points behind the pro-China Kuomintang presidential candidate Han Kuo-yu (see following chart). The key slogan in the Tsai campaign, “Hong Kong today, Taiwan tomorrow” appears to have been even more effective than Britain’s Boris Johnson’s “Get Brexit done”. In this respect, the election result represents more collateral damage for Beijing from Hong Kong Chief Executive Carrie Lam’s ill-fated attempt last year to amend Hong Kong’s extradition bill.

Taiwan Presidential Election Opinion Polls in 2019 (Tsai Ing-wen vs Han Kuo-yu)

Taiwan’s Growing Onshoring Boom

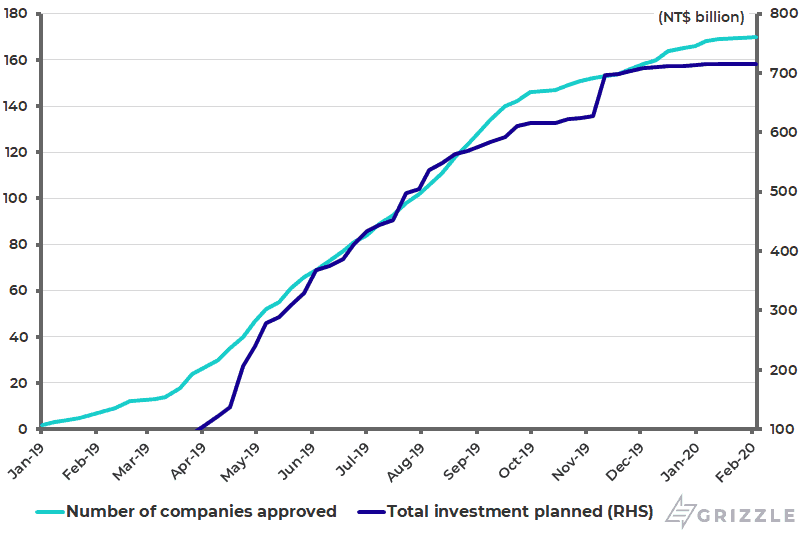

Still, the incumbent DPP government is also benefitting from growing evidence that Taiwan’s onshoring boom, the consequence of U.S. tariff hikes and export controls targeting China, is having positive ripple effects in the domestic economy. The onshoring boom, in terms of production moving from China back to Taiwan, continues to show up in growing evidence of a domestic capex cycle.

So far, 170 companies’ reshoring plans had been approved by the government as of Feb. 6, with approved investment projects totalling NT$716 billion or US$24 billion (see following chart). These investments are expected to create potentially 59,183 new jobs, while real gross fixed capital formation rose by 4.3% YoY in 3Q19 and was up 7.3% YoY in the first nine months of last year.

Taiwanese Companies’ Action Plans to Invest Back in Taiwan

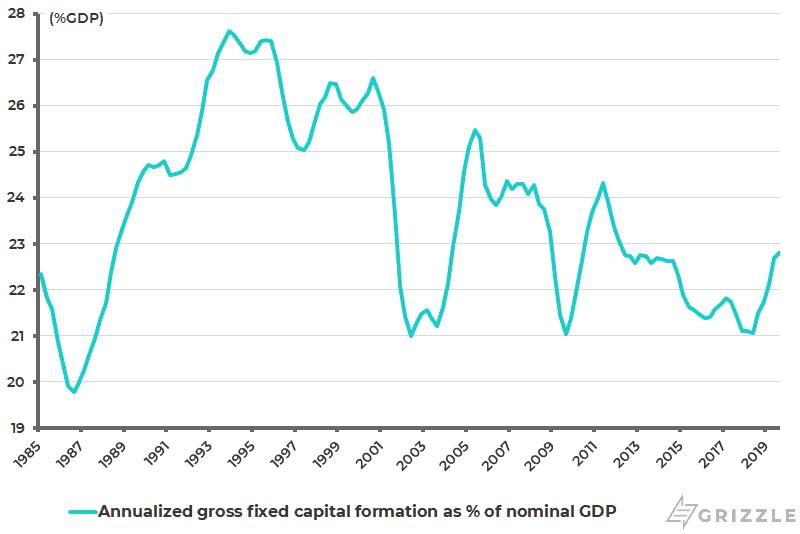

Taiwan Annualized Gross Capital Formation as % of Nominal GDP

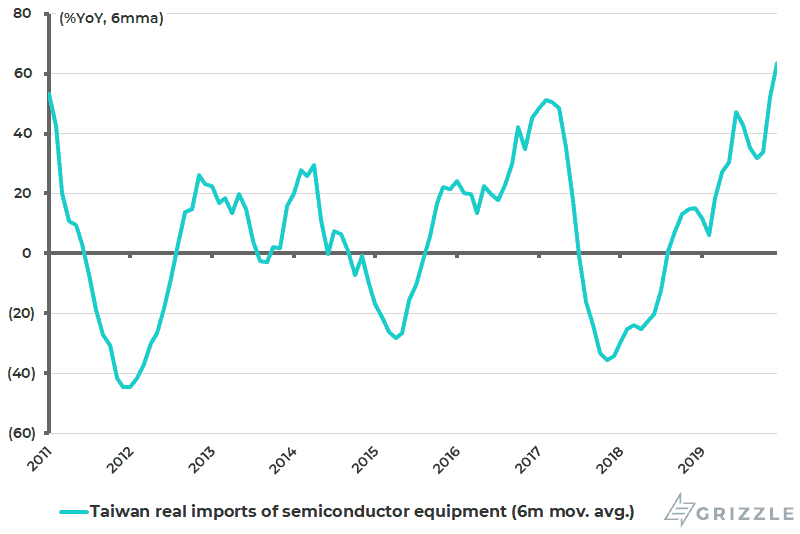

As a result, Taiwan’s annualized gross fixed capital formation to nominal GDP ratio bottomed at 21.1% in 2Q18, the lowest level since 3Q09, and has since risen to 22.8% in 3Q19 (see previous chart). There was also a 56% YoY increase in real imports of semiconductor equipment last year (see following chart).

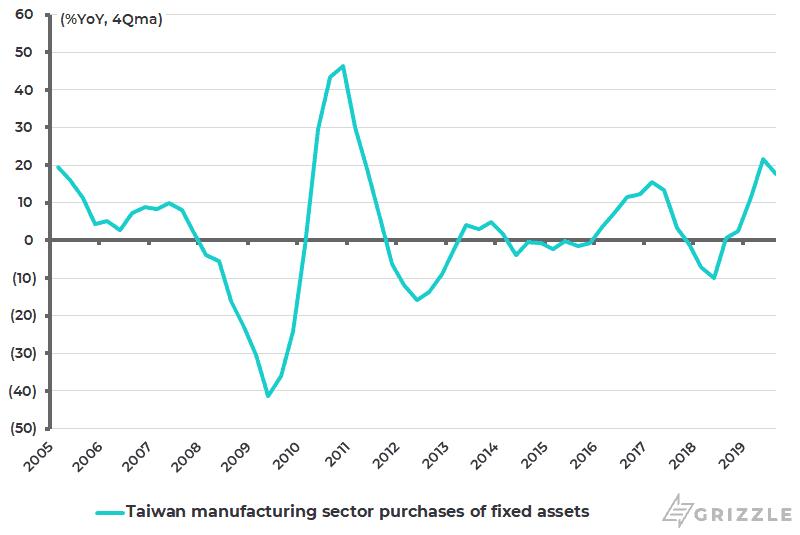

Finally, the Ministry of Economic Affairs’ latest quarterly survey on manufacturing investment, published in December, shows that manufacturers’ purchases of fixed assets were up by 23.7% YoY in the first nine months of last year. This contrasts with only an annualized 0.1% increase in the previous eight years (see following chart).

Growth in Taiwan Real Imports of Semiconductor Equipment

Taiwan Manufacturing Sector Purchases of Fixed Assets

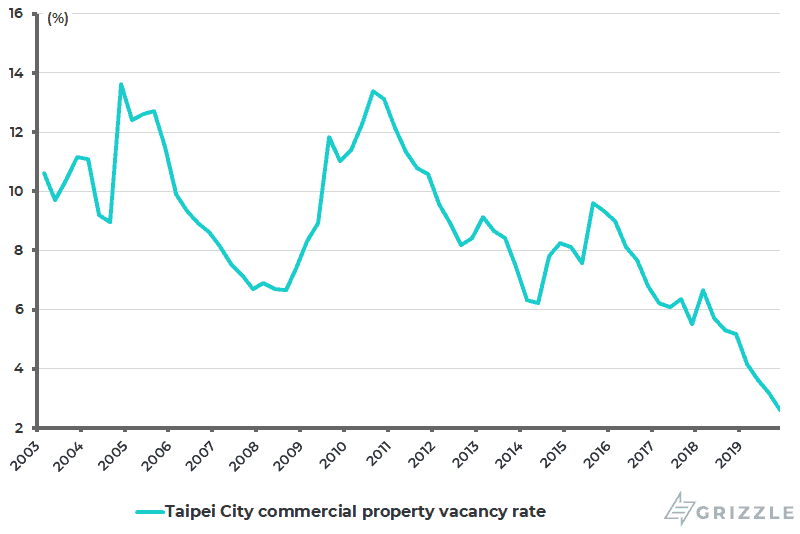

The same positive dynamic is reflected in ongoing evidence of a pickup in the local property market after several years in the doldrums. Taiwan’s six-city housing transactions rose by 24% YoY to 22,300 units in December. There is also a commercial real estate cycle to play given both the catalyst to development provided by onshoring and the collapse in the Taipei commercial property vacancy rate to a record low of 2.6% in 4Q19 (see following chart).

Taipei City Commercial Property Vacancy Rate

Still, the long-term risk to Taiwan, and the world’s leading semiconductor foundry TSMC in particular, remains the island’s acute strategic vulnerability in a world where US-China strategic rivalry intensifies. For the risk is that the American national security lobby puts pressure on TSMC to stop supplying China and Huawei in particular. Huawei currently accounts for an estimated 11% of TSMC’s total revenues of US$34.6 billion in 2019 and China customers in general 20%. After all, Taiwan is a U.S. ally. Still, this should not be a short-term consideration with the “phase one” trade deal between the U.S. and China signed last month.

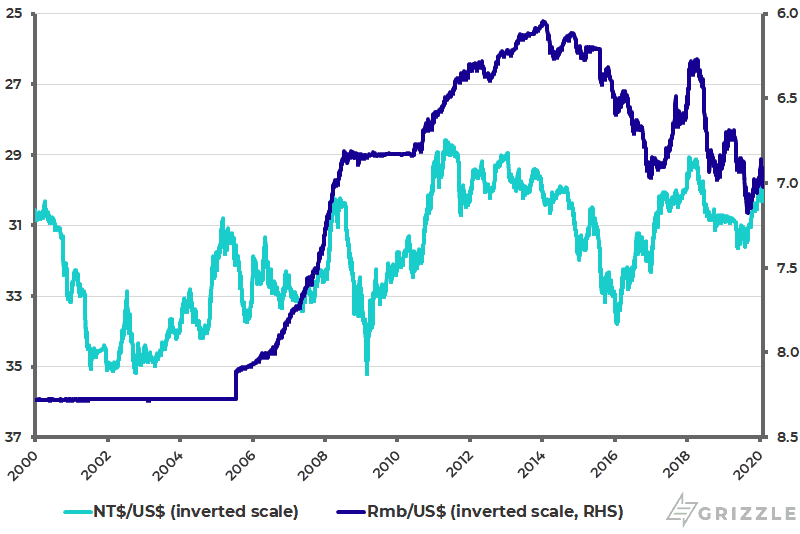

Meanwhile, with the U.S. finally stopping last month labelling China a “currency manipulator”, it is worth noting the lack of appreciation of the NT dollar in stark contrast with the renminbi in the past 15 years. The NT dollar has appreciated by only 2% against the U.S. dollar since March 2005. By contrast, the renminbi has appreciated by 18% against the U.S. dollar since 2005 (see following chart).

Taiwan NT Dollar/US$ and Renminbi/US$ (Inverted Scale)

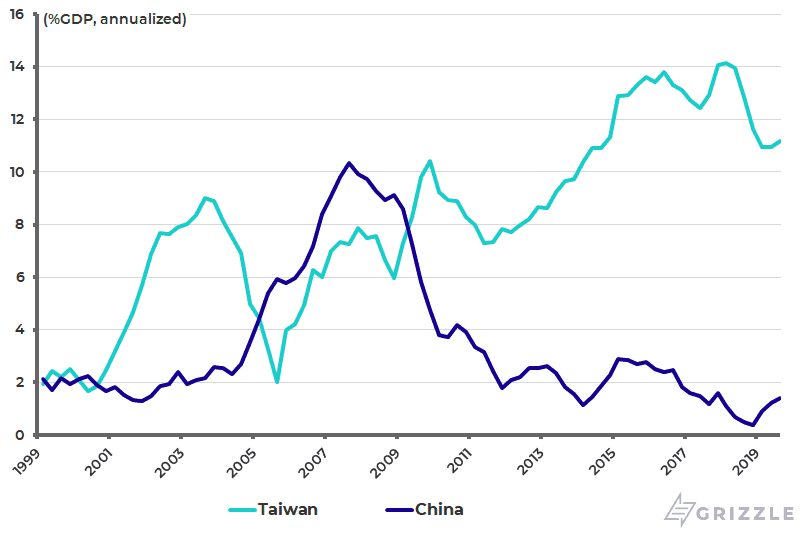

This is despite the fact that Taiwan has continued to run large current account surpluses during a period where China’s current account surplus has declined dramatically. Taiwan’s annualized current account surplus has risen from 2% of GDP in 3Q05 to 11.2% of GDP in 3Q19, while China’s annualized current account as a percentage of GDP declined from 10.3% in 3Q07 to 0.4% in 4Q18 and was 1.4% in 3Q19 (see following chart). This, naturally, raises the issue of who is the biggest mercantilist of them all!

Taiwan and China Annualized Current Account Surplus as % of GDP

If the Taiwan election result was a blow for Beijing, it was not an unexpected one. And if anyone can take a long-term view it is the PRC, with Xi Jinping having made it clear in a speech at the start of 2019 that he intends to sort out the Taiwan issue before the end of his term in power, the length of which is clearly undefined.

Will Xi’s Loyalist Restore Order in Hong Kong?

Meanwhile, there has been an important development in Hong Kong of late. That was the appointment in early January of a political heavyweight and a loyalist of Xi, Luo Huining, as the new head of China’s Central Government Liaison Office in Hong Kong. At first sight, this looks ominous for Hong Kong’s aspirations for a more liberal political system. This is because Luo has a track record of enforcing Beijing’s mandate in the provinces he ran, be it cracking down on Tibetan dissidents when he was in charge of Qinghai province between 2013 and 2016, or cracking down on notoriously corrupt local officialdom in Shanxi province, which he ran from June 2016 until November last year.

Aged 65, Luo was given the Hong Kong job despite having reached the formal retirement age for his level of seniority as a provincial party chief. But there again the same applied to Wang Qishan who has run Xi’s highly effective anticorruption campaign since its start in late 2012 and is now Vice President aged 71.

The message seems to be that the 66-year-old Xi wants to give important jobs to those with established track records. Meanwhile, the issue for Luo is that he will no longer be running a province but will have to work with the weak and demoralized Hong Kong government with only seven months left before the Legislative Council elections. Still, he will presumably be the boss in all but name given the lack of basic political skills displayed by Hong Kong Chief Executive Carrie Lam.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.