The consumer retail giant, Target (NYSE:TGT) reported earnings per share of $1.69 in its 4Q, versus the $1.65 Wall Street estimate.

Revenue for the period came in $23.4 billion, slightly below analyst estimates of $23.45 billion.

The earnings surprise this quarter seems to have foregone its track record by coming in at the low end of the spectrum at 2.4% and -2.1%, respectively.

In the wake of the coronavirus, Target lowered revenue guidance for FY2020.

The stock is basically flat in early trading today.

At current levels, the stock is trading around 14.3x earnings.

This is a big discount to Costco and Walmart, but is it justified?

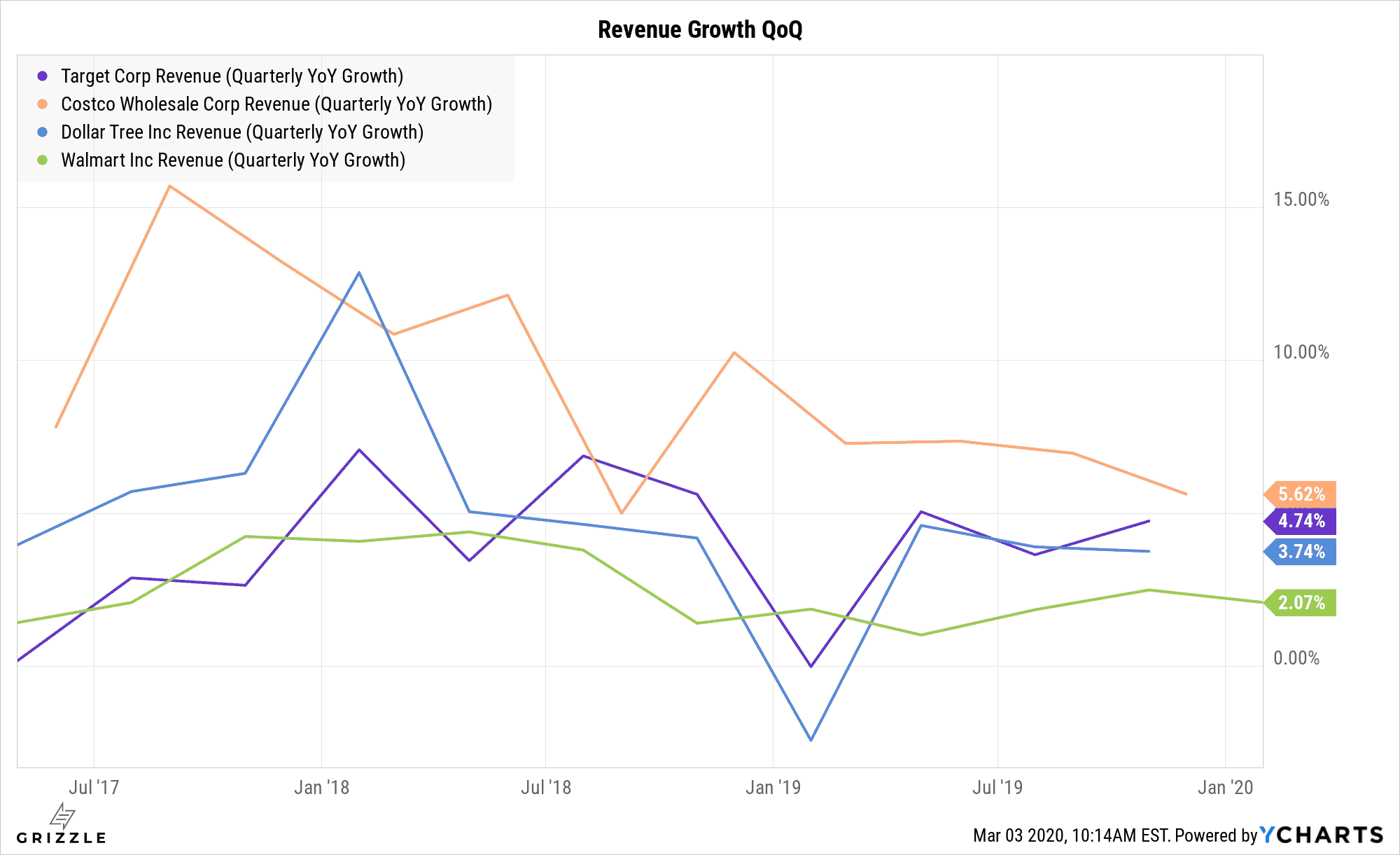

If we look at Growth, Target has historically grown slower than Costco, but the growth rates are converging and only a 1% difference separated the two last quarter.

Target is doing an excellent job maintaining revenue growth and the huge P/E discount to Costco more than offsets the difference in growth between the two.

Lets move on to profitability next.

Target screens very well on profitability compared to peers.

Target’s operating profit margin of ~5.9% is 50% higher than Walmart and 88% above Costco.

So based on profit margins, Target should not be trading at such a big multiple discount to peers.

Overall, Target looks like an attractive stock compared to Walmart and Costco.

Though the market expects Costco to continue growing faster than Target, Target is priced far cheaper and generates more cash for each dollar of sales.

After the recent selloff in Target, the stock looks poised to continue outperforming Costco and Walmart driven by the profitability advantage and reasonable price.

After the recent selloff in Target, the stock looks poised to continue outperforming Costco and Walmart driven by the profitability advantage and reasonable price.

Growth & Shareholder Returns

2019 has shown investors that Target has the capacity to keep pace with industry standards, as well as continue its differentiation strategy.

Despite revenue being shy of Wall Street estimates, the consumer retail giant behemoth reported digital sales growth of 20% YoY, with same-day services (order pick up & Shipt) contributing to more than 80% of comparable digital sales growth.

On another positive, return on invested capital (ROIC) for 2019 was 16%, compared to 14.7% in 2018.

EBITDA margin ticked up to 8.1% in 2019, compared to 7.8% one year ago.

The company has been diligently continuing its share repurchase program, along with just about every other company in the S&P 500.

The latest earnings report mentions that there is only $100 million left in its share repurchase program from 2016.

The company’s board of directors initiated an additional $5 billion share repurchase program in September 2019, which will take effect after the current share repurchase program is finished.

Share repurchases for 2019 sat at $606 million, reducing the shares outstanding by 5.1 million.

The company chose to keep its dividend expense the same, despite the reduction in share count which resulted in a 3.1% increase in dividends per share.

Differentiation

Target launched 8 new private label brands this year, such as Everspring, All in Motion, and Good and Gather.

Private label brand strategies can greatly improve a company’s overall productivity due to cost efficiencies and the omittance of royalties if executed correctly.

Within the last year, Target has also launched its own loyalty program, Target Circle, and customer interest-targeted third-party marketplace, Target Plus.

Target Plus can be attributable to the rising competition from Amazon.

Target is known for having friendly staff and for the exorbitant amounts of money they invest into payroll and training.

In 2019, Target raised its minimum wage to $13/hour with the goal of reaching $15/hour by the end of 2020. For comparison, Walmart’s current wage sits at $11/hour.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.