It is always instructive to see how quickly investor sentiment can respond to market action. Having worked themselves into a deflationary frenzy during the summer as a result of collapsing government bond yields globally, investors are now on the verge of becoming cyclically exuberant.

Will Trump Announce a Deal Before the December Deadline?

I would still give the current “risk on” move the benefit of the doubt; though it is a close call. It is still believed here that The Donald, whatever his verbal blustering of late, will want to announce a trade deal with China before the Dec. 15 tariff hike deadline.

The moment of truth is approaching on this one. America’s 45th president likes to view himself as the ultimate negotiator. But on this occasion he has, as previously written here (Will China and the US sign a ‘currency pact’?, Nov. 5, 2019), overestimated his leverage because he saw China’s stock market decline in 2018 as being driven by his trade war. In this respect, Trump has been ill-served by his economic advisers who should have informed him that the weakness in Chinese equities last year was primarily induced by the PBOC’s squeeze of shadow banking. But apparently they did not understand this basic point too.

In this respect, Beijing has started to “squeeze” Trump, rather than the other way round. Thus, China has commented of late that any trade deal with the U.S. would include a rollback of at least some of the tariffs. On this point, Ministry of Commerce spokesman Gao Feng said at a weekly briefing in early November that if China and the U.S. reach a phase-one trade deal both sides should simultaneously remove existing additional tariffs in the same proportion.

The logical way to interpret this statement is that China will only agree to a deal if there is some reduction in existing tariffs. Most bullish for markets would, clearly, be a removal of all Trump’s tariffs. This is what Trump should do because the tariffs are hurting American entities, though there is a legitimate question whether The Donald understands this. But perhaps most likely, if a “phase one” deal is agreed, is a rollback of the most recent 15% tariffs introduced on Sept. 1 on US$112 billion of Chinese imports.

One point is clear. A deal where America only agrees not to raise tariffs further is already discounted by markets and should be viewed by traders as an opportunity to “sell on the news”. But that assumes Beijing will agree to such a deal which, as already noted, now seems unlikely. If Trump does not like being squeezed, the Chinese will not want to make it too obvious since they will understand the need for Trump to save “face”.

So the issue is whether Trump will listen to Steven Mnuchin and Larry Kudlow, who will be telling him to roll back the tariffs, or to Peter Navarro who will probably not want any deal at all. Ultimately it all boils down to whether Trump will want to run in the presidential campaign as a China-basher or as the man who negotiated the biggest deal with China since its entry into the WTO in 2001. To me, it is obvious that the American president’s personality favours the latter outcome. He would also like a “win” to deflect from the impeachment noise which is now gathering momentum.

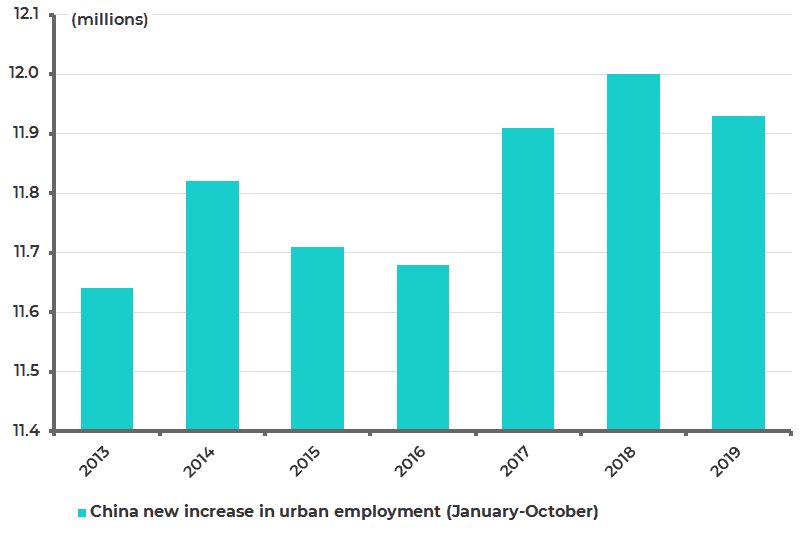

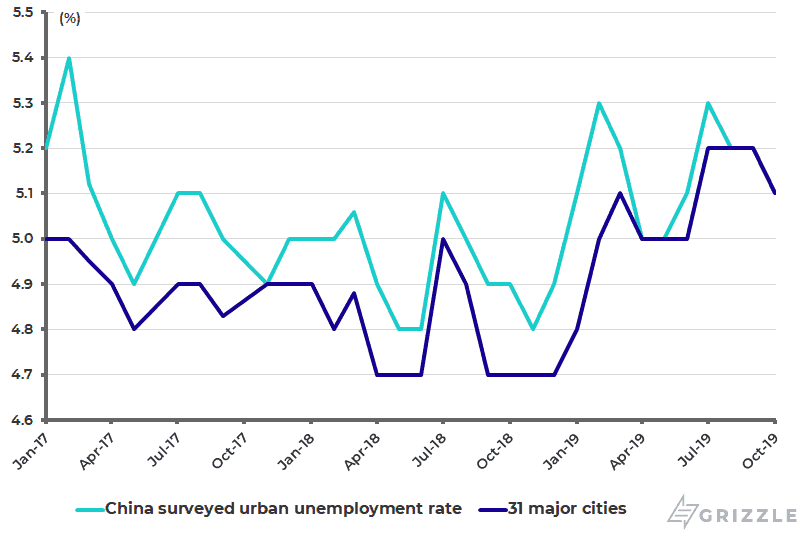

China would also clearly prefer a deal to no deal, which is also why it has still not published its “unreliable entities list” 15 weeks after saying it would do so. The Ministry of Commerce first announced the idea at the end of May and said on Aug. 22 that it would release the list in the “near future”. Still Beijing is not desperate to do so since its labour market, while weak, is far from collapsing. The new increase in urban employment declined only 0.6% YoY to 11.93 million in the first ten months of 2019, while the surveyed urban unemployment rate fell from 5.2% in September to 5.1% in October.

China New Increase in Urban Employment (January-October)

China Surveyed Urban Unemployment Rate

The Effect of a Trade Deal on Markets

Returning to the impact of the trade issue on markets, I also continue to believe that any trade deal would have a much more positive impact, particularly on emerging markets, if it contains a currency angle in terms of some sort of verbal agreement where China agrees not to engage in competitive devaluation.

For a trade deal with a currency component and a reduction in existing tariffs should send equities higher, led by Asian equities. But once that has all happened, assuming bravely it does happen, it is only a matter of time before markets start worrying about whether this means the end of Fed easing. At that point, the attention will return to the “late cycle” risk in an American economy driven almost entirely by consumption, and where the situation of the average consumer is simply not as healthy as the macro data implies because of the extreme income distribution.

Trump vs. Bloomberg

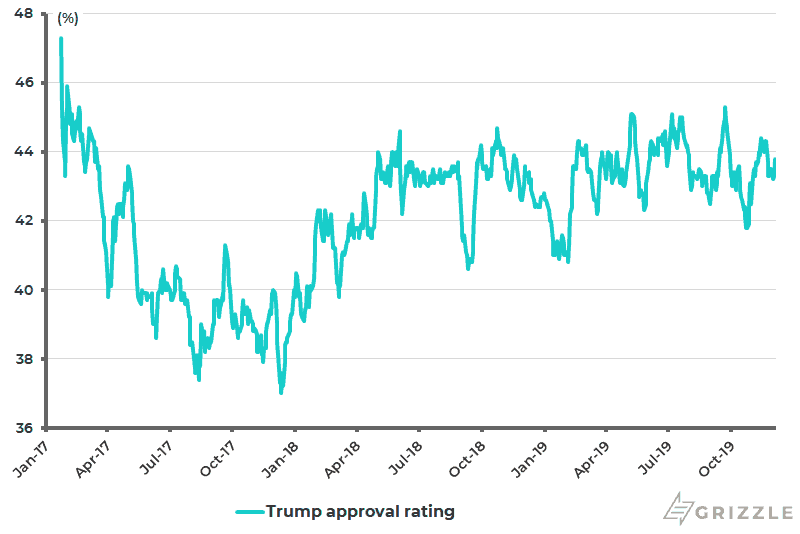

Speaking of unequal wealth distribution, excitement has been generated over the past two weeks by former New York mayor Michael Bloomberg entering the presidential race. Bloomberg officially launched his presidential campaign on Nov. 24. This will please many voters in the coastal cities. But I would, for now at least, back Trump to beat the billionaire in a tight race. The key point here remains how solid Trump’s approval rating has remained throughout his presidency.

Trump’s approval rating has been running in a range of 37-47% since his presidency began in January 2017 and has averaged 42.1% over this period (see following chart). This reflects the reality that Trump is actually trying to implement the policies he campaigned on. The strong base is also the reason why Republican senators will support Trump in the impeachment process unless, of course, there is a sudden collapse in the approval rating which at present seems unlikely in the extreme. In fact it has risen from a recent low of 41.8% in late October to 44.4% in mid-November and is now 43.7% (see following chart).

President Donald Trump’s Approval Ratings

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.