It may be a little ridiculous. But Donald Trump’s surprise decision, or threat, to impose a new round of tariffs on China at the start of September has subsequently reignited monetary easing expectations. So after spending barely a day worrying that the Fed rate cut of 25bp on July 31 was only a single “insurance cut”, investors duly herded the other way.

More Monetary Easing on the Way

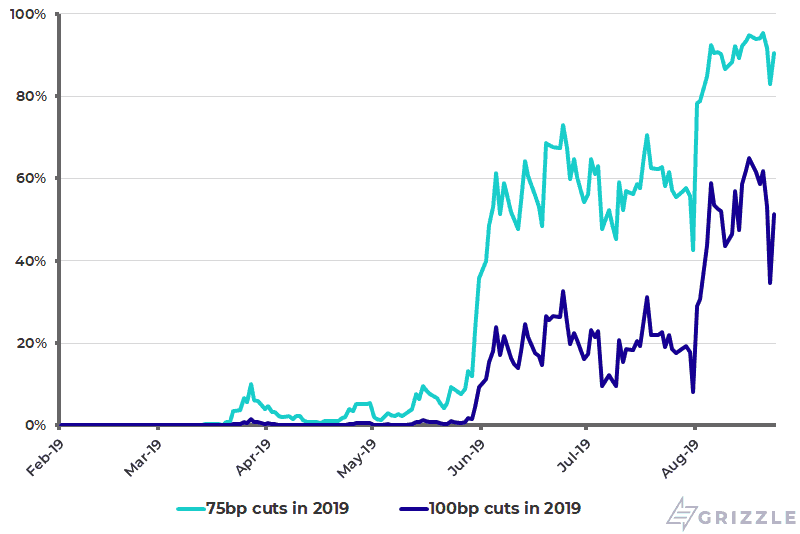

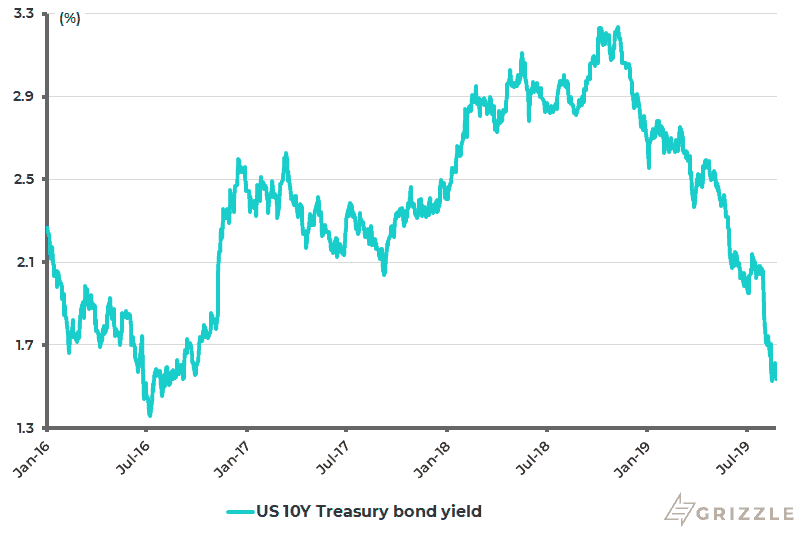

Monetary easing expectations have surged and Treasury bonds have rallied again. The Fed funds futures are now discounting a 90% chance of a further 50bp of rate cuts by the end of this year and even a 51% chance of 75bp of cuts (see following chart). Meanwhile, the 10-year Treasury bond yield has declined by 60bp from 2.07% on July 31 to an intraday low of 1.47% on Aug. 15 and is now 1.54% (see following chart).

Fed Funds Futures Implied Probability of Rate Cuts in 2019

US 10-year Treasury Bond Yield

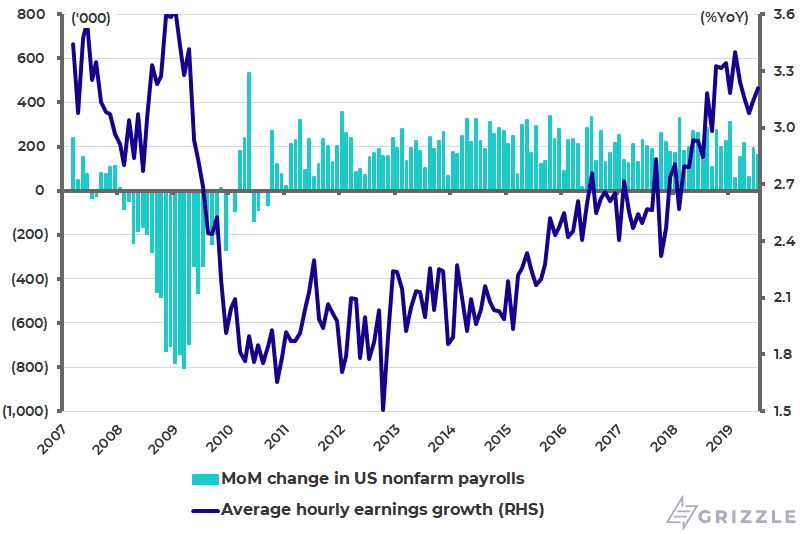

Financial markets are, therefore, assuming that the Federal Reserve will respond in the manner the Donald would like. And, on this point, markets are probably correct, which means the Fed will continue to enable Trump’s protectionist agenda as regards China. Still, it should be noted that there was little in July’s payroll data to encourage renewed easing expectations. True, the wage data has now not made a new year-on-year high for five months. But otherwise the data was quite satisfactory from a growth perspective. Average hourly earnings growth rose from 3.1% YoY in June to 3.2% YoY in July, while U.S. non-farm payrolls increased by a seemingly healthy 164,000 jobs in July (see following chart). The next payroll data is next Friday.

U.S. Change in Non-farm Payrolls and Average Hourly Earnings Growth

Trump’s New Round of Tariffs

What about Trump’s latest tariff moves? I have to admit to having originally being surprised by the threatened 10% increase in tariffs on the remaining US$300 billion of Chinese imports made on Aug. 1. More worryingly, the American president announced, by tweets, last Friday more tariffs hikes.

The existing tariffs on US$250 billion of imports from China will be raised from 25% to 30% on Oct. 1, while the threatened 10% increase in tariffs on the remaining US$300 billion of Chinese imports will be increased to 15%. It should also be noted that the 15% tariffs are scheduled to impose on about half of the US$300 billion products starting Sept. 1, with tariffs on the remaining goods being delayed to Dec. 15. Trump’s move came hours after China unveiled retaliatory tariffs on US$75 billion worth of imports from America earlier on Friday.

All this will be bad news for the American economy and the global economy, if implemented, and would clearly mark an escalation in the trade war. With markets now increasingly assuming escalation of the trade war, I would still not give up all hope of a deal because ultimately such a deal is in Trump’s own political interest. But his recent actions have certainly now made that harder to negotiate.

If the Donald wants a deal with China, he needs to understand that the counter-party is an entity with inordinate patience, not a short-term seller of a piece of real estate. In this respect, Trump’s actions continue to suggest that he thinks he has more leverage than he actually has in terms of the supposed weakness of the Chinese economy. Yet on this point it is quite clear that the Chinese government is preparing its population for slower growth, with its references to The Long March, and remains extremely reluctant to engage in a destabilizing mega stimulus or for that matter a destabilizing devaluation.

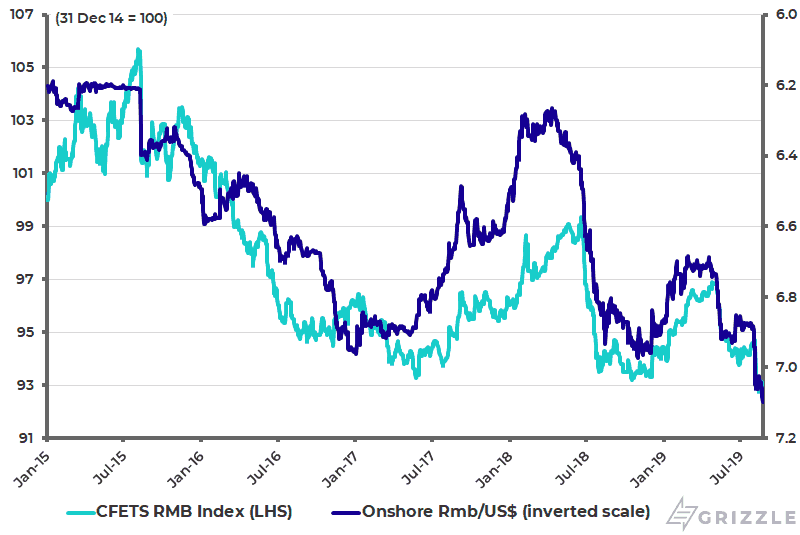

This raises the issue of the Chinese currency. The base case remains that the PBOC will continue to manage the currency around its trade weighted index, as it has done since late 2015 when China moved off the managed dollar peg. The correlation between the renminbi-dollar exchange rate and the trade-weight renminbi index has been 0.74 since Dec. 2015 (see following chart). This remains an entirely sensible strategy while a big devaluation would be contrary to China’s own interest since, as a domestic demand-driven economy, it would undermine Chinese consumers’ dollar purchasing power.

China Trade-weighted Renminbi Index and Rmb/US$ (inverted scale)

Lower Interest Rates in the U.S. Helps China

Meanwhile China’s real vulnerability remains the same as it has always been. That is the risk of capital outflow and managing the closed capital account. In this respect, the Donald is doing Beijing a favour by bullying the increasingly hapless Jerome Powell to cut interest rates because such monetary easing makes it less likely that the U.S. dollar will surge higher precipitating more pressure on China’s capital account. Those pressures have picked up of late as reflected in the rising errors and omissions item in China’s balance of payments.

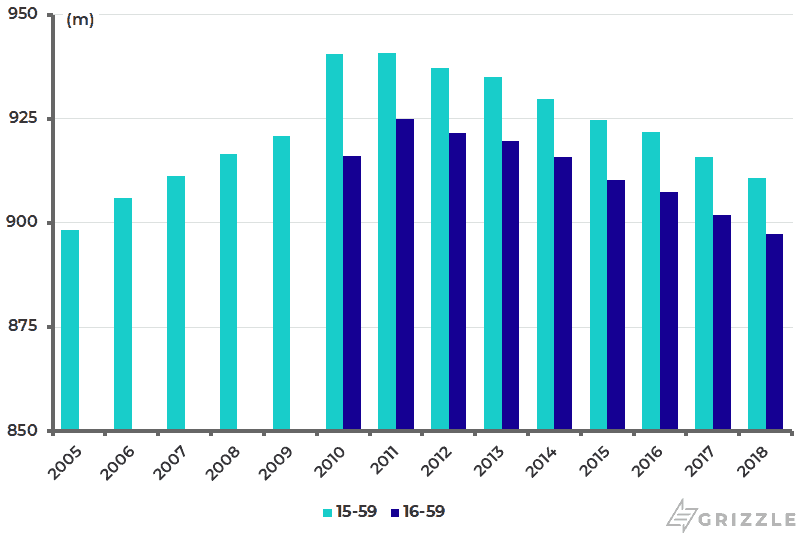

For such reasons, if the increasingly aggressive national security lobby in Washington is really determined to prevent China’s further rise, it would be best advised to put pressure on China to open its capital account completely. For the command economy, and indeed the mainland political system, would no longer be viable in such a liberalized context. However, the best time to have done that was back in 2001 by making China’s access to the WTO subject to a fully open capital account. In this respect, the horse has long since bolted while the pressure on China to generate jobs is now much less than it was then since the working age population peaked in 2011 (see following chart).

China Working-age Population

Meanwhile, if there is no deal in coming months, and the tariff increases are duly implemented, China will still not back down. That in turn will raise the risk of more aggressive measures, most particularly given Washington’s proven appetite for sanctions and related dollar “weaponization”. In the narrow context of financial markets, this could even mean pressure on American institutional investors to stop investing in Chinese equities or bonds, and pressure on index vendors such as MSCI to stop including China in benchmark indices. While still unlikely, such policies are no longer impossible. But, hopefully, the Donald’s dealmaking instincts will ultimately prevail.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.