Atlassian Corporation PLC.(NASDAQ: TEAM), a leading provider of team collaboration and productivity software reported fourth-quarter fiscal 2020 earnings that disappointed analyst expectations.

Shares are 7% lower in after-hours trading.

The company generated $430.5M of revenue, above street consensus by 4.7%, and 28.7% higher than the same quarter last year.

This was well within management’s revenue expectations for the quarter of being between $400M-$415M.

Atlassian’s subscription revenue segment rose by 43.3% year-over-year to $257.52M.

Earnings per share came in at $0.25/sh, 19% higher than analyst expectations of $0.21/sh.

This was also well above management’s guidance of $0.17/sh to $0.22/sh.

Management disappointed the market however with guidance for next quarter that fell short of expectations.

With the stock price run Atlassian had since last quarter’s earnings the market needed to see strong guidance to keep the stock flat.

Valuation Analysis

Atlassian’s share price performance is much weaker than its peers as shown below.

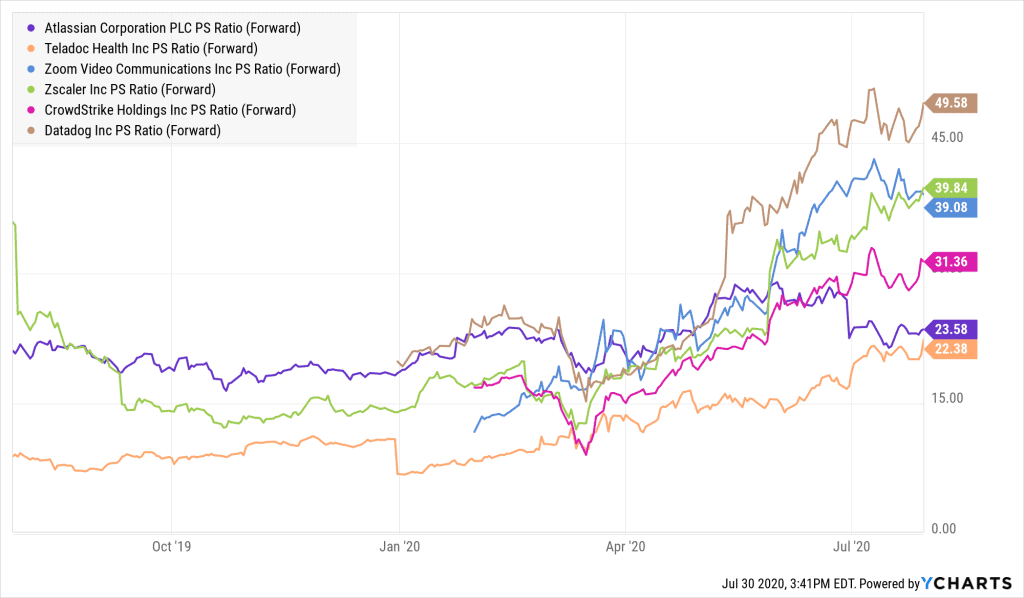

Its price to sales multiple of 23.7X is amongst the lowest of the bunch as well.

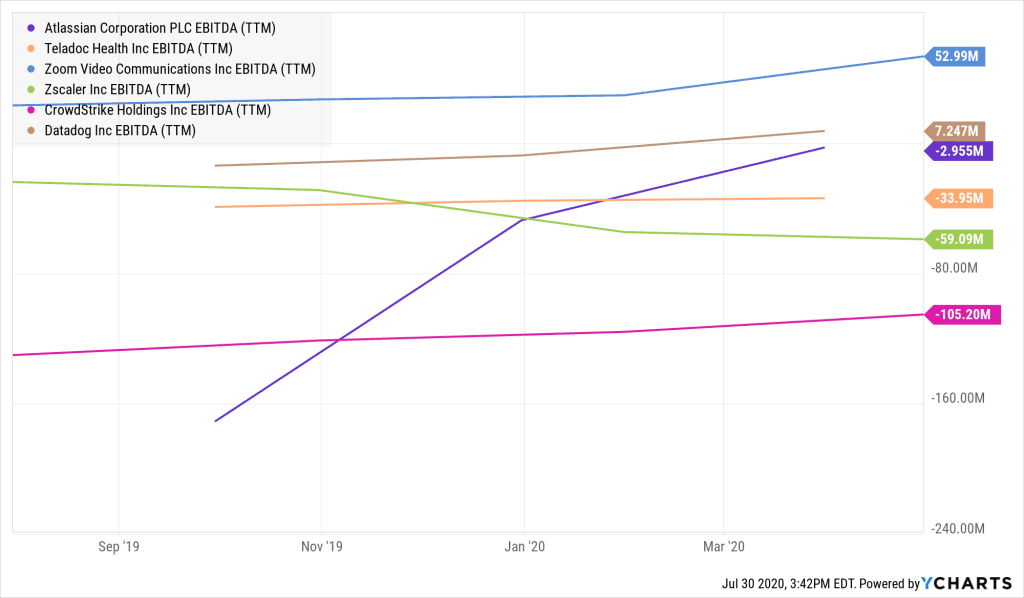

However, a closer look at the company’s trailing twelve months EBITDA indicates that it is growing well and is ranked one of the top three, better than Zscaler and CrowdStrike. But if you didn’t notice, the latter two company’s PS multiple is higher than Atlassian’s.

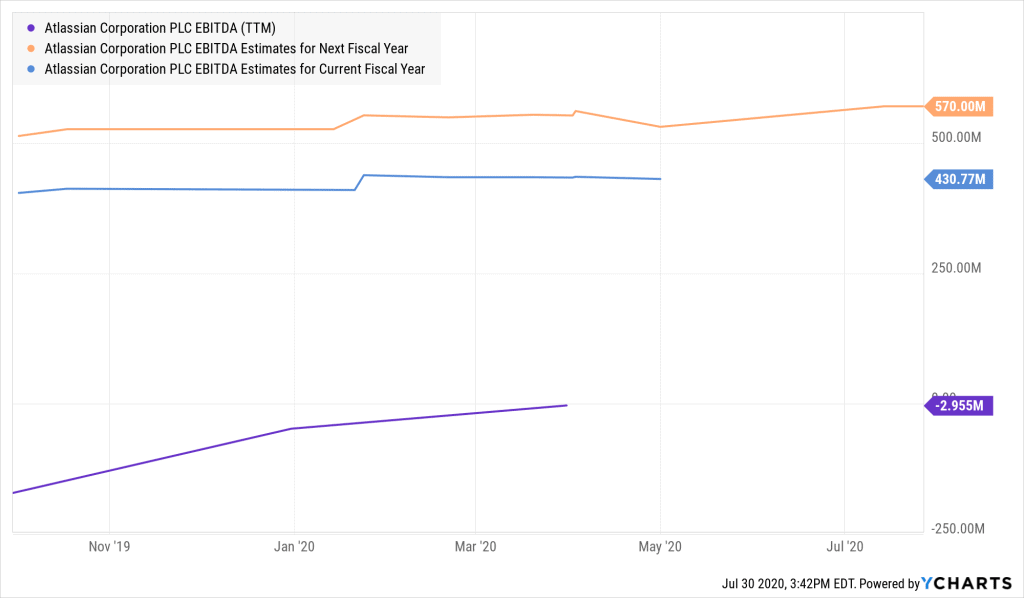

Furthermore, when comparing Atlassian’s, trailing twelve months EBITDA with EBIDTA expectations of analysts, it is clear that the company is highly likely to see advanced growth in the coming quarters.

Therefore, we believe that this presents a value opportunity, where the share price of Atlassian would rise to a levels where until at least its PS multiple is somewhat more closer to that of either Zscaler’s and CrowdStrike’s.

Additionally, management’s higher revenue guidance for the next fiscal year’s first quarter being between $430M to $445M, suggests that the company is capable of gaining more value in the near term.

As a result, it is evident that Atlassian could see an enhancement of its share value in the near future, thus making it a potential buying candidate worth paying attention to.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.