Mainstream media has always fawned over its Silicon Valley superheroes — they were mission driven, uber-liberal, pansexual, and ethical. Their narratives represented ‘America-the-good’, the antithesis to a cheeseburgers-in-bed, porn star banging President.

The gushing and fawning has now come to an abrupt halt. The fanboys are dismayed and betrayed — their heroes were supposed to ‘cure the world of all disease’, but instead their personal data was sold to the highest bidders in seedy tech back alleys. It’s all fifty shades of Elizabeth Holmes — a pinch of ‘real’ technology, and heaps of new age PR chasing techno-healer.

Facebook — What’s the Value of a Pathological Social Network?

Mark Zuckerberg has proved time and again that he’s as sociopathic as you feared, whether it’s screwing over early investors, or selling your data to a pink-haired troll. You simply don’t pay a premium multiple for this kind of ‘special and unique’ pathology:

So, umm. This is what Mark Zuckerberg said in 2009… pic.twitter.com/XPWE3ORoXJ

— BBC Three (@bbcthree) March 25, 2018

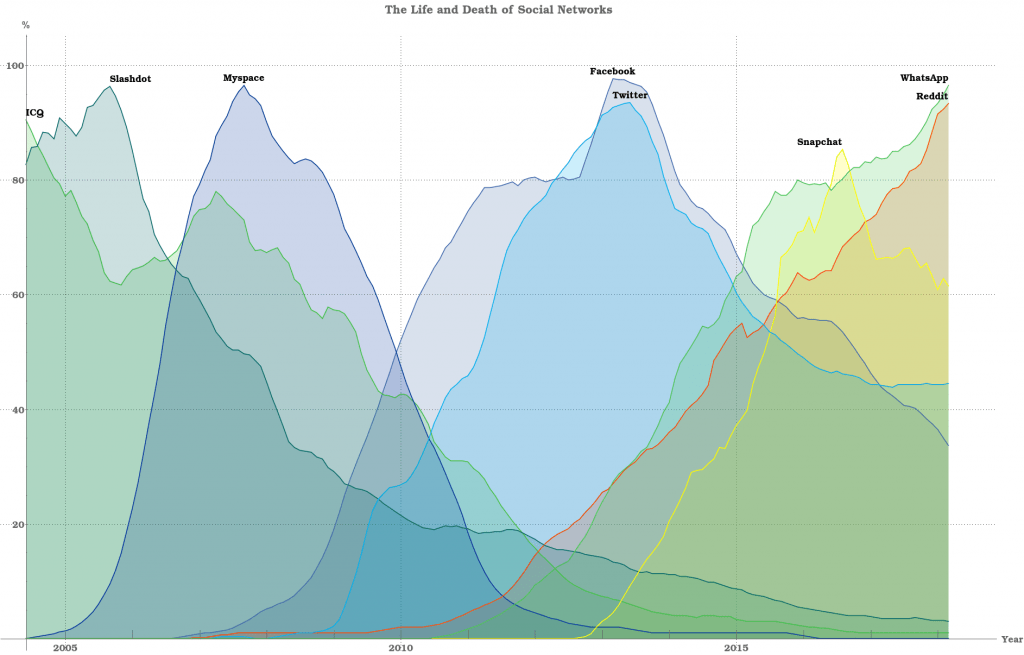

Zerohedge highlighted the following graph showing Google search interest of social networks through time. This graph was created prior to the #deletefacebook movement, the investor narrative should be plenty clear — social networks are the furthest thing from a utility.

Something new and shiny always comes along. Telegram, a free encrypted message service, sounds like the right antidote for many of the current social network ills. Having raised $1.7 billion through an initial coin offering doesn’t hurt either.

The main pushback from the bulls on the stock is that Facebook owns the two other dominant social networks: WhatsApp and Instagram.

Facebook paid $19 billion for the platform and the app currently has an impressive 1.3 billion users. Only snag is that the app generates no revenue for mothership. Zuckerberg will have to pull a straight up Houdini to squeeze any revenue from this app. Users will balk at any attempt by Facebook to monetize ads generated from very personal phone-based messages.

On the other hand, Instagram does generate revenue. eMarketer estimated the platform generated $4.1 billion in sales in 2017, representing approximately 10% of Facebook’s total $40 billion 2017 sales. However, the platform is simply too small to fill the gap for any shortfall resulting from the Cambridge Analytica fallout at Facebook.

Facebook Investor Outlook

Facebook investors are genuinely looking down the barrel of the abyss for three main reasons: Valuation multiples still have downside, strong cash flow and slowing growth, questionable efficacy of digital ad spend.

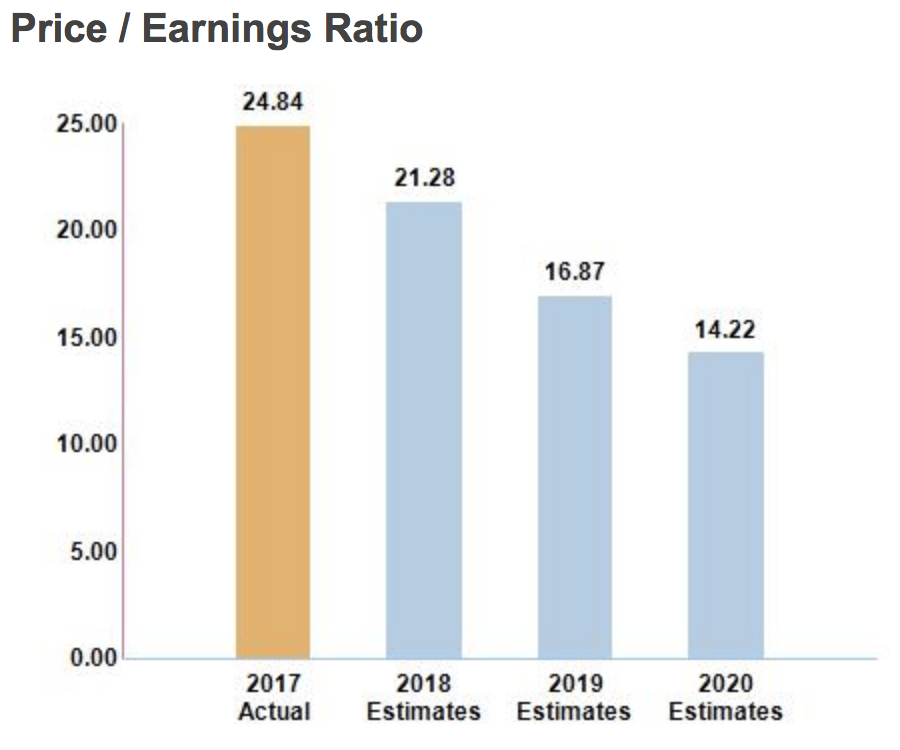

Valuation multiples still have downside

Wall Street analysts estimate the company will earn $7.19/share in 2018. Consensus in classic form will be meaningfully behind the curve on the impact of the crisis on user confidence.

While desperately trying to regain trust of users the company will most certainly look to take the foot off the ‘advertising accelerator’. If revenues decelerate meaningfully in 2018, the stock could easily trade down to a mid-teens multiple for 2018 — representing ~30% downside.

If earnings grow at the rate analysts bullishly imagine it will only amplify the scrutiny of flat-footed regulators.

Strong Cash Flow and Slowing Growth (Not a Good Look for Tech)

The death cross for any technology stock is high free cash flow generation and slowing user/sales growth metrics. ‘Clever’ value investors that know squat about technology start to nibble away only to see the base of growth investors exit stage right quickly.

Questionable Efficacy of Digital Ad Spend

Advertisers will certainly be gun-shy of investing significant ad dollars in a channel with abysmal user trust ratings. Additionally, Macro Battleship highlighted the issue of ‘ineffective’ digital advertising, P&G cut $200 million in digital ad spend in 2017 and found that it had no impact on sales.

Tesla — From an EV in Space to a Self-Driving, Self-Combustible EV on Earth

Elon Musk has been basked with overwhelming praise as truly being an eco-superhero variant of Iron Man. From flamethrowers to cars in space, he’s one of the most gifted technology carnival ring leaders of our time. Hell, even German engineer-snobs love him:

![]()

He is unquestionably a next level visionary, no matter how much debt it took him to get there, he has created the sexiest cars in a generation and sent a fuck-off sized rocket to space. He is to eco-technology what Trump is to gaudy real estate development.

He even trolls on Twitter, Musk vs. TSLA short sellers in 2013:

Seems to be some stormy weather over in Shortville these days

— Elon Musk (@elonmusk) April 25, 2013

And he’s at it again on April Fools – faking bankruptcy. The fanboys absolutely ate it up.

Tesla Goes Bankrupt

Palo Alto, California, April 1, 2018 — Despite intense efforts to raise money, including a last-ditch mass sale of Easter Eggs, we are sad to report that Tesla has gone completely and totally bankrupt. So bankrupt, you can’t believe it.— Elon Musk (@elonmusk) April 1, 2018

Those carefree rock star days may now become a distant memory. Tesla is facing a full frontal assault greater than any challenge faced in the past. He has pulled his company out of debt Armageddon before. Heck he’s even pulled his cousin out of debtors prison (Tesla acquiring SolarCity). He’s been able to navigate corporate minefields one at a time before, but never a cluster bomb like this.

Production Issues and Balance Sheet Stress

Moody’s downgraded Tesla’s debt rating on Tuesday which sent both the bond and stock price plummeting. The downgrade was on the back of a ‘significant shortfall in the production rate of the Model 3 electric vehicle’ — the $35k mass market fantasy.

More troubling, any corporate officer that gets a whiff of Tesla’s books for long enough gets the hell out quick, over the last year Tesla’s Chief Accounting Officer and Chief Financial Officer both quit abruptly with less than 12 and 18 months on the job respectively.

Tesla needs to raise money very soon and the bond market is effectively closed for the company. The company had $3.7 billion in cash at year end 2017, and it burned through $3.7 billion in the same year — this is a company with a lifeline of 1 year at the most.

Equity investors are the only ones that can stop the bleeding, however the negative feedback loop of plunging debt and equity prices ensures such a lifeline will be punitively dilutive for existing shareholders.

Self-driving Fatality and Model S Recall

The Grizzle Reel has always been suspect of the nonsensical vision of a ‘better world’ ushered in by self-driving/autonomous vehicles, the dream was destined to die with a few ‘computer bug’ related deaths.

In the span of a month we’ve had Uber’s autonomous vehicle strike and kill a pedestrian and Tesla’s Model X SUV crash into a concrete divider on autopilot subsequently killing the driver.

Adding to the technical woes Tesla announced the largest recall in its history on Thursday, 123,000 Model S sedans were recalled due to rust prone bolts in the steering column.

Legal Issues

In December it was reported that Tesla was under a year-long SEC investigation about making ‘false statement of material facts’ related to the Model 3, the real rub however was that Tesla conveniently failed to let investors know.

On Wednesday a Delaware court allowed Tesla shareholders to sue Mr. Musk and board members for violating their fiduciary duty by approving the acquisition of SolarCity – the debt riddled company that was run by his half-wit cousin.

The proverbial ‘shot clock’ is counting down, Musk will need to dig deep into his carnival bag of tricks (ie. flamethrower, car in space…) to pull this off otherwise bankruptcy certainly awaits.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.