Tesla Inc. (NASDAQ: TSLA) reported their Q4 2019 earnings today.

EPS was $2.14 which beat analysts’ expectations of $1.76 (+21.59% vs estimates). Revenue for the quarter came in at $7.38 billion which beat analysts’ expectations of $7.05 billion (+3.81% vs estimates).

Tesla has been one of the best performing stocks in the entire U.S. stock market for the past year and the stock has almost doubled from the same time last year. This parabolic climb in stock price has confused analysts and opinions are divided on where the stock will go next.

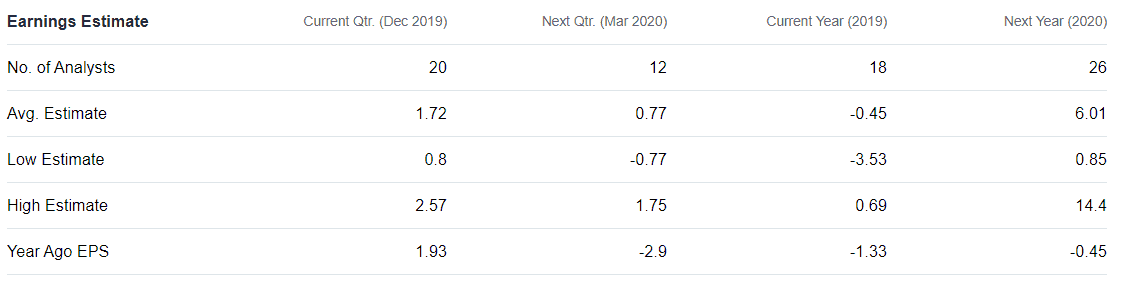

Analysts’ Expectations Are All Over the Place for Tesla

The range of estimates for EPS for this quarter span from $0.80 per share all the way to $2.57 per share. Looking at estimates for the whole year of 2020, the difference is even more drastic, with some analysts predicting a whopping $14.40 per share and the low estimate coming all the way down to $0.85 per share.

This partly explains the volatile behaviour of the stock that has been the case for the past year. Before its SpaceX-rocket-propelled rise to over $500 per share, the stock crashed to below $200 back in May of 2019.

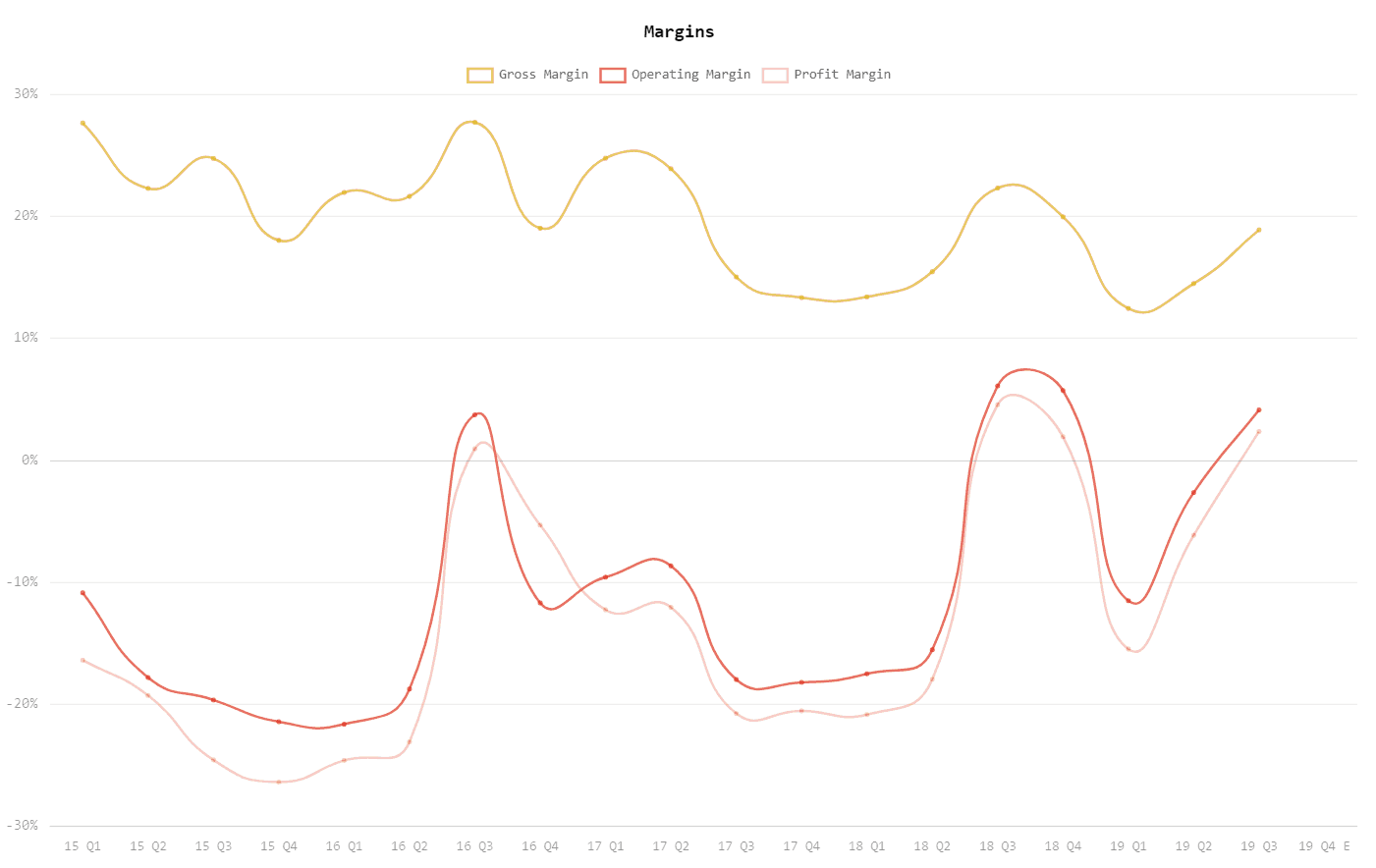

Gross Margin Will Be a Key Focus For Tesla in the Coming Months

Tesla’s gross margin has been trending downwards lately (18.9% in the previous quarter), which is not a good sign, at least in the short term. But shareholders need to keep in mind that this is partly caused by Tesla’s ramp up in their Model 3 cars which sell for much cheaper than the Model S and Model X and also carry a smaller margin. The margins are also impacted by regulatory fees and other one-time expansion costs that the company has incurred as it expands at a ludicrous speed.

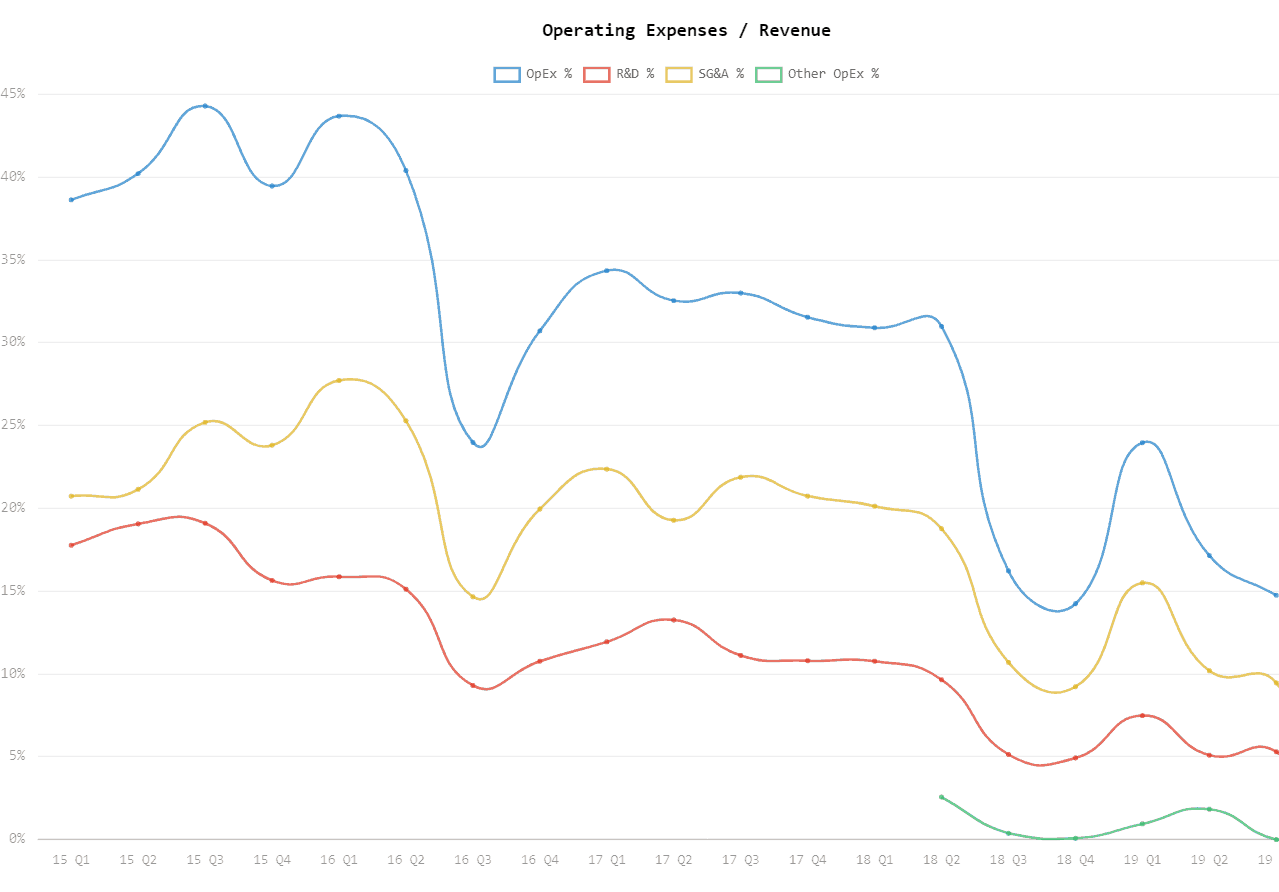

Tesla Has Brought Their Expenses Under Control, For Now

Part of the reason why Wall Street has renewed their confidence in Tesla is the fact that Tesla’s expenses seem to be finally decreasing. Last quarter, operational expenses came in under $1 billion for the first time since Q3 2017 and their expenses as a percentage of revenue has decreased dramatically. This is incredible news for Tesla shareholders as Tesla is on its way to becoming consistently profitable if they can continue to keep their expenses down.

There’s Lots To Be Excited About Regarding Tesla

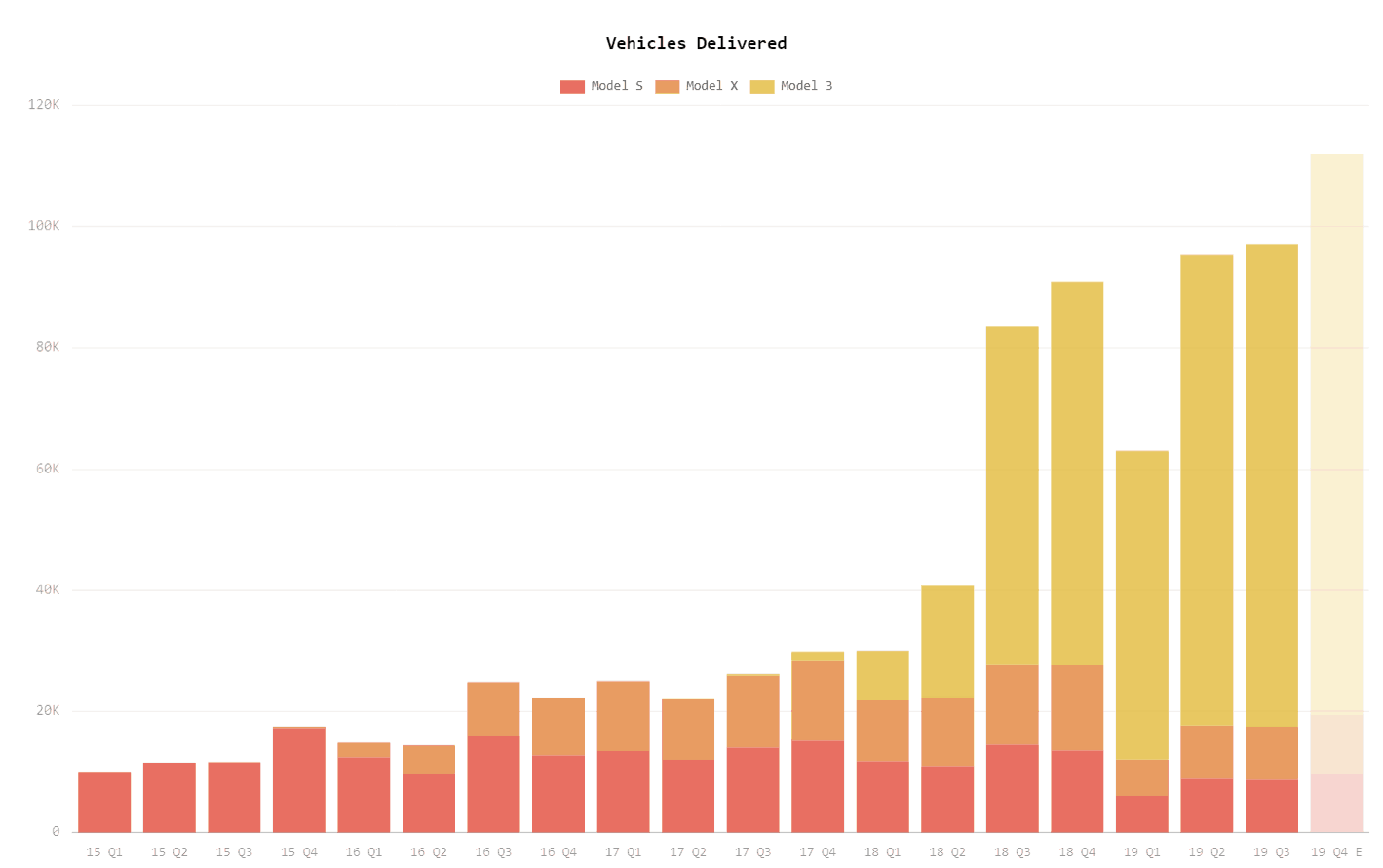

Tesla reported record delivery numbers for Q4 2019 coming in at 112,000 deliveries in total which represents an all-time record high for Tesla. This metric beat analysts’ expectations who were forecasting deliveries somewhere just over the 100,000 mark.

The Model Y Has Been Spotted Out In the Wild

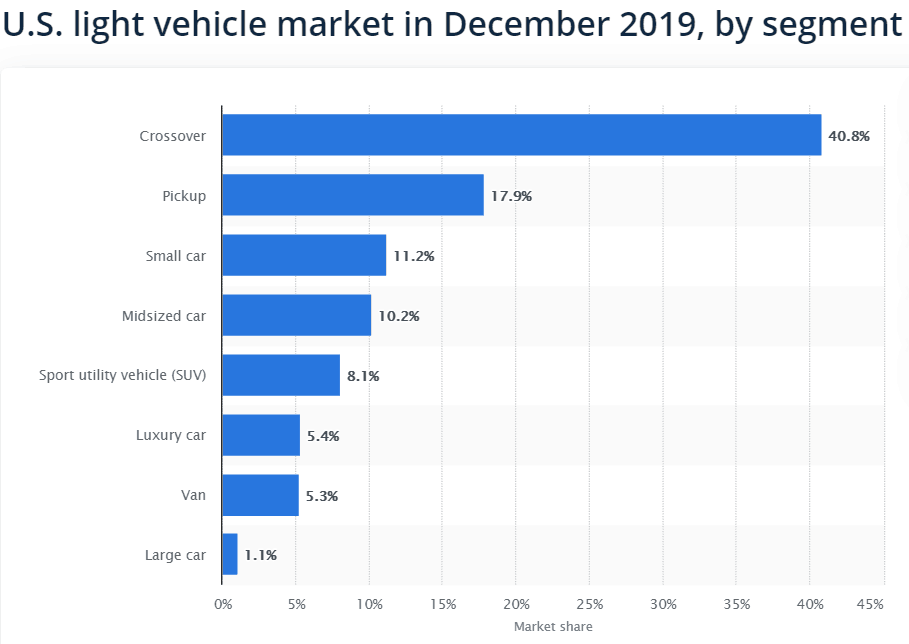

The Model Y, Tesla’s upcoming Sport Utility Crossover, will be a very important product for Tesla. According to the latest data from Statistica, the crossover category makes up by far the largest share of the automobile market in the United States, at just over 40%.

The Model Y has already been spotted numerous times out in the wild, another sign that Tesla will roll out the product much sooner than the original anticipated Q3 2020 release.

A Tale of Two Gigafactories

The Shanghai Gigafactory was completed right before New Year’s and Tesla has started to deliver its first China-made Model 3s. Right around the same time, hot off the news and excitement of the Shanghai Gigafactory, Elon Musk announced that the company has selected Berlin, Germany to be the site of Gigafactory 4. Construction on Gigafactory 4 has already begun as the company wasted no time in their expansion.

Germany provides a unique opportunity for Tesla to further tap into the European market and puts Tesla right on the home turf of many of its powerful competitors like Volkswagen Group, BMW, and Daimler.

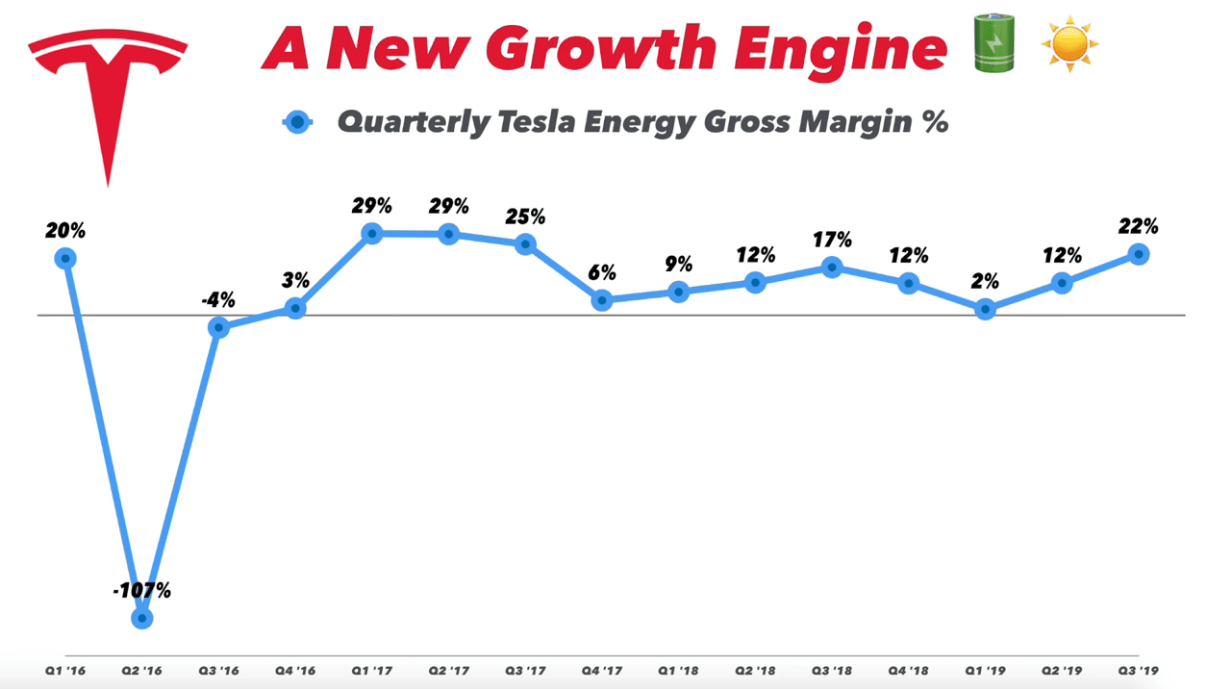

Is Tesla’s Energy Business a ‘Dark Horse’?

Everyone likes to ignore Tesla’s energy segment. Or, people simply forget that it exists at all since it only makes up a very small part of Tesla’s revenue at the moment. The company has been pouring a ton of money into developing better battery technology and its acquisition of SolarCity back in 2016 puts Tesla into the solar panel business. Tesla’s energy segment gross margin hit a record high of 22% last quarter. It may be a mistake to ignore this portion of the business as there is still massive potential for growth in this sector.

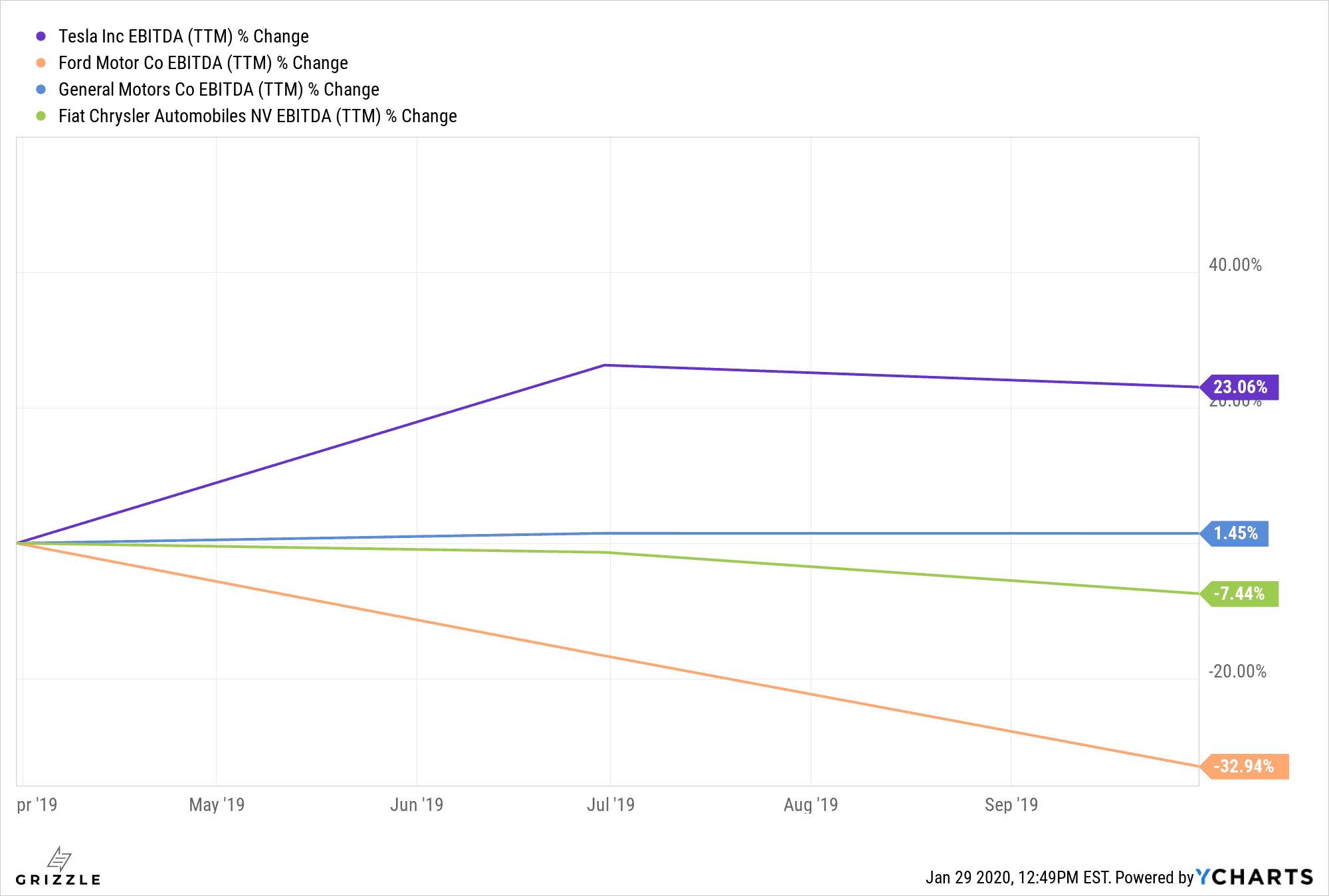

Tesla is Growing While Other U.S. Car Manufacturers Are Flat or Declining

Tesla’s EBITDA has grown by over 20% in the past year in a time when all other U.S. car manufacturers are either flat or suffering from a decline.

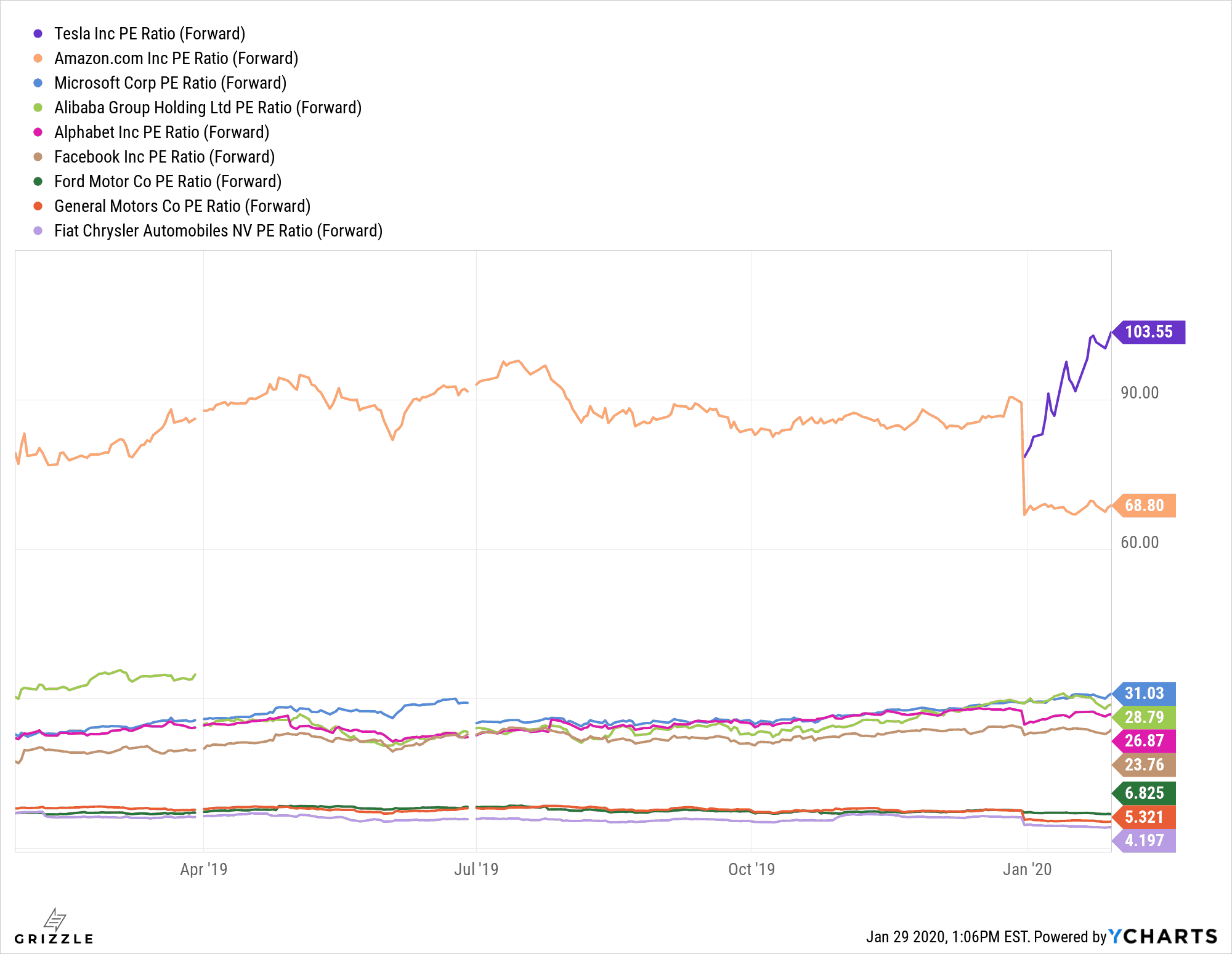

Is Tesla A Tech Company or an Auto Company? Does this Graph Answer Your Question?

Looking at the forward P/E of Tesla compared to U.S. automakers, to say that it’s a night and day difference would be an understatement. Words cannot emphasize enough the difference in valuation between Tesla and other U.S. automakers.

In the short term it seems that Tesla is extremely overvalued, trading at a forward P/E of over 100! People who are looking to pick up some Tesla stock should reconsider their decision to pick up some shares at these levels unless they plan to hold for the very long term. Even then, it may be a wiser decision to hold off until the price comes down to more reasonable levels.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.