Tesla reported first quarter earnings that handily beat estimates.

In a seasonally weak quarter Tesla managed to generate positive net income, a milestone for the company.

The stock is up 7% in after-hours trading as investors digest the better than expected results.

Revenue of $5.99Bn beat market estimates of $5.86Bn.

Non-GAAP earnings came in at a gain of $1.24, crushing analysts estimates for a -$0.21 loss.

Analysts have raised earnings expectations for the second quarter by 11% since January even with China on lockdown and the world in Quarantine.

Current guidance may have been pulled but this quarter’s results show that profitability may be a regular occurance going forward.

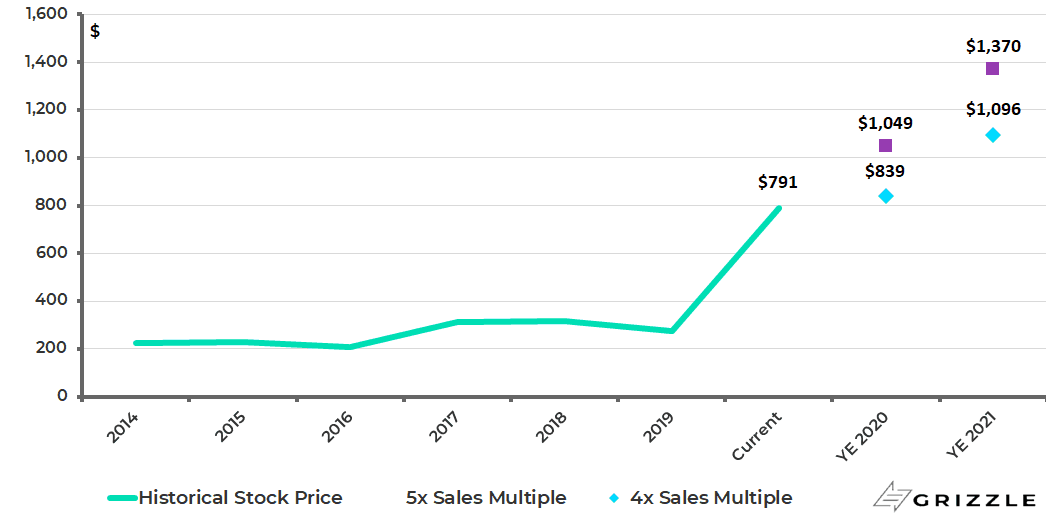

[su_panel background=”#d1cef4″ radius=”7″]If Tesla can put up the revenue growth numbers the market expects in 2021 and 2022 and maintain some level of free cashflow and positive earnings, the stock still has 35%-70% upside over the next 1-2 years. The big risk to the current stock price is if consumer demand ends up lower than the market expects this year due to cheap oil and COVID-19 spending cutbacks. Watch consumer spending and oil prices closely. [/su_panel]Potential Stock Price at 4x and 5x Sales Multiple

Why You Don’t Bet Against Tesla

Elon Musk and Tesla have proved the doubters wrong time and again.

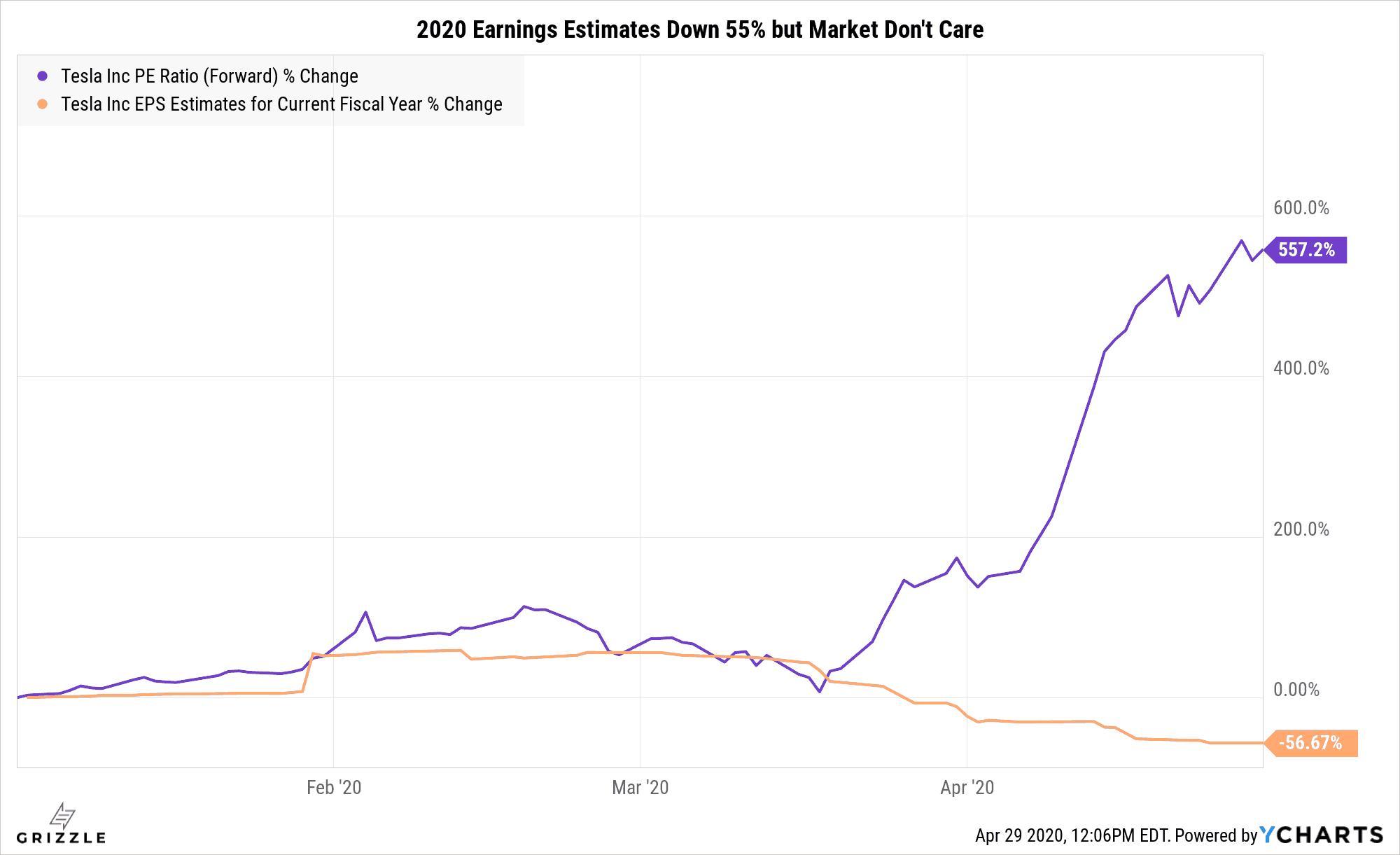

Now with the company generating some positive free cashflow and putting up six months of positive earnings, the stock multiple has moved to a whole new level.

Even though analysts now expect Tesla will generate 55% less net income in 2020, the stock is back to all-time highs.

The Price to Earnings Multiple has now Reached a Whole new Stratosphere.

Some may say Tesla is now laughably expensive but we say you might have to look at this stock from a Millenial retail investor’s point of view.

They love Tesla for the long term.

If this year’s results are bad, they just look to the future when numbers will look great once again and the trading multiple will fall back to a reasonable level if the stock goes sideways.

[su_panel]Tesla remains a dream stock and will trade on price to sales when times are not so good, and price to earnings when Elon is at his most dreamy.[/su_panel]The only way we see the multiple compressing at this point is if consumer demand just isn’t what the market is expecting.

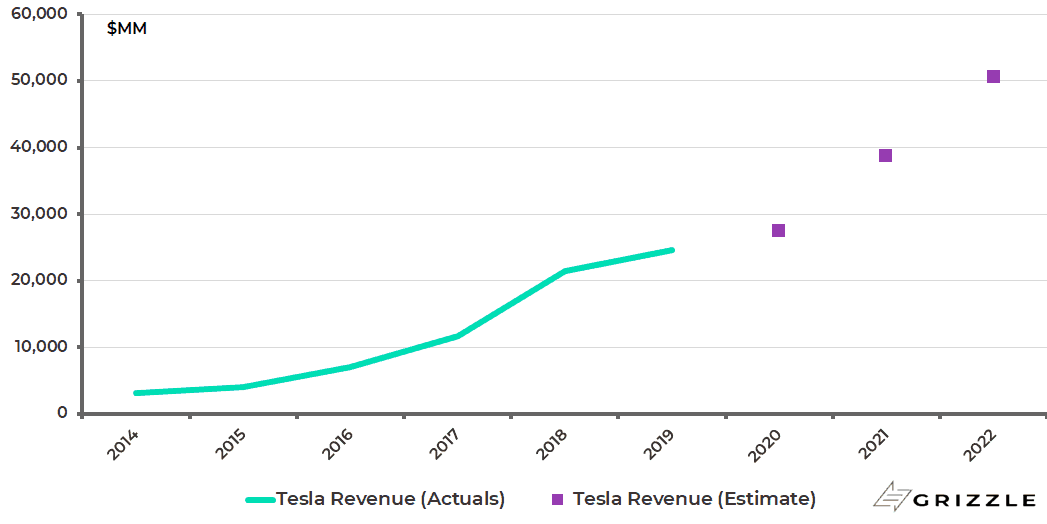

Even in the face of slowing revenue growth as the model Y ramps up sales and the older models fall out of favor, the market is already looking ahead to 2021 and 2022 when revenue growth should reaccelerate to 40% in 2021 and 30% in 2022 from only 11% expected this year.

Higher revenue growth brings a bounceback in earnings and the P/E multiple will fall back to a crazy, but not so crazy level and let’s be real, in a world of unlimited government spending do earnings even matter?

Revenue Growth Expected to Pick Back up in 2021-2022

Demand the Big Risk Factor in 2020

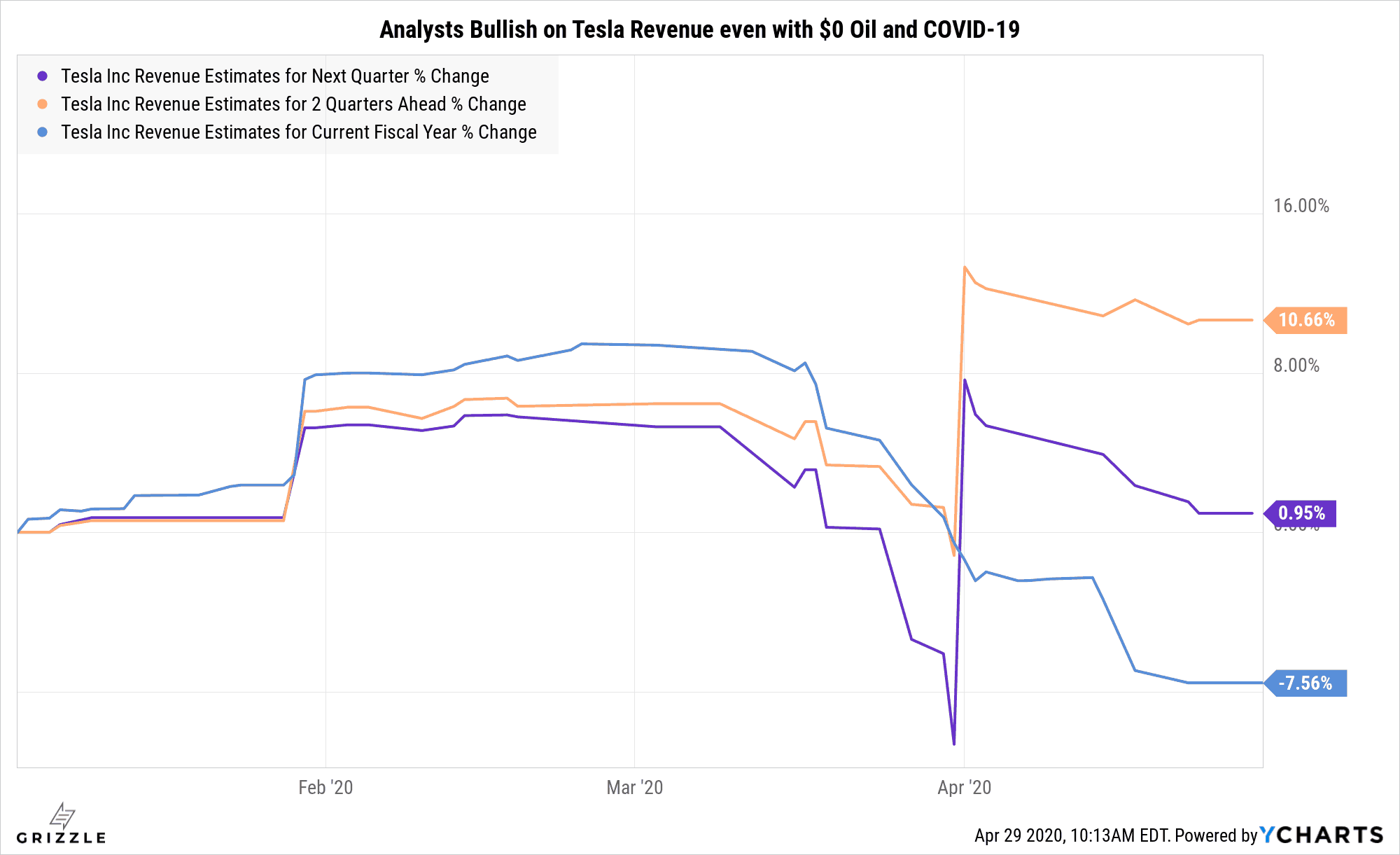

Analysts have actually become more bullish on second-quarter deliveries since the COVID-19 pandemic began.

Though estimates for full-year 2020 revenue have been cut 8% since March, analysts still think next quarter (ending June) will see a big bounceback in deliveries and revenue will be 11% higher than what they were expecting before COVID-19 appeared.

The only explanation we can come up with for this bullishness is a belief among analysts that production capacity is improving and there is pent up demand as purchases that didn’t happen in February-March will now happen in April-June.

Yes the market already looks like it is pricing Tesla off 2021 results, if demand doesn’t rebound as quickly as analysts are expecting, then estimates for the rest of 2020 need to come down.

Falling estimates equal a lower stock price, if just temporarily.

In our opinion. Tesla stock still has 30%-70% upside over the next two years, but investors need to watch consumer spending data out of China, Europe and the U.S. along with oil prices for any indication of softening demand.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.