The coronavirus newsflow continues.

But the focus of concern has switched dramatically from Asia to Western Europe and North America.

The base case remains what it was last week, namely that the number of new cases has peaked in mainland China.

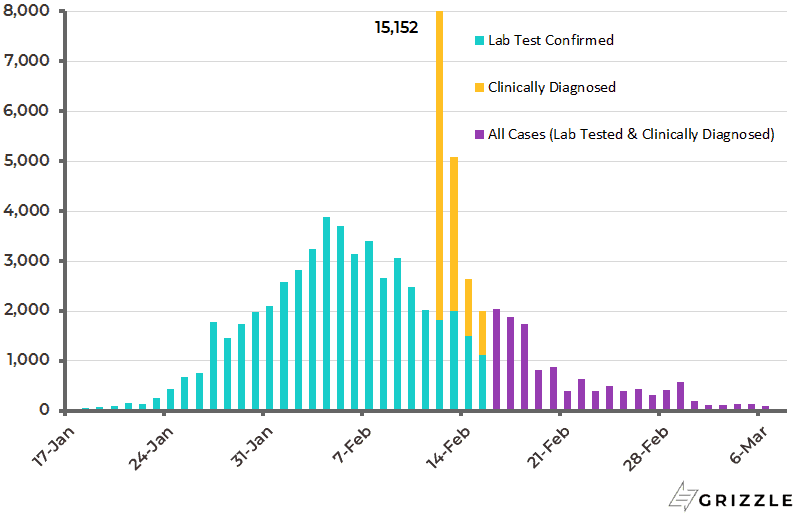

To be precise, they peaked on Feb. 4 at 3,887 new cases, however, the situation was muddied to the extent that Hubei province, ground zero for the virus, reported a record 14,840 new confirmed cases on Feb. 12.

This includes 13,332 so-called “clinically diagnosed” cases, which were previously seen as suspected cases and are now counted as confirmed cases following the National Health Commission’s diagnosis criteria revision.

As a result, the number of new cases in the mainland surged to 15,152 on that day.

Since then the number of new cases has collapsed to 44 cases on Saturday.

Mainland China Daily New Confirmed Coronavirus Cases

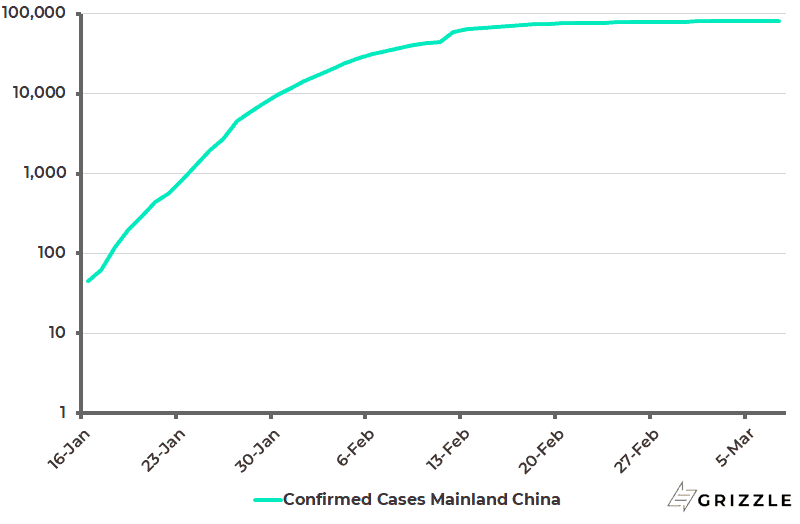

The decelerating trend in China can be clearly seen in the log chart below.

If this continues to be the case, the threat to Chinese growth should still be viewed as a one-quarter write-off and the mainland economy should be expected to bounce back strongly thereafter.

Mainland China Cumulative Confirmed Coronavirus Cases (log scale)

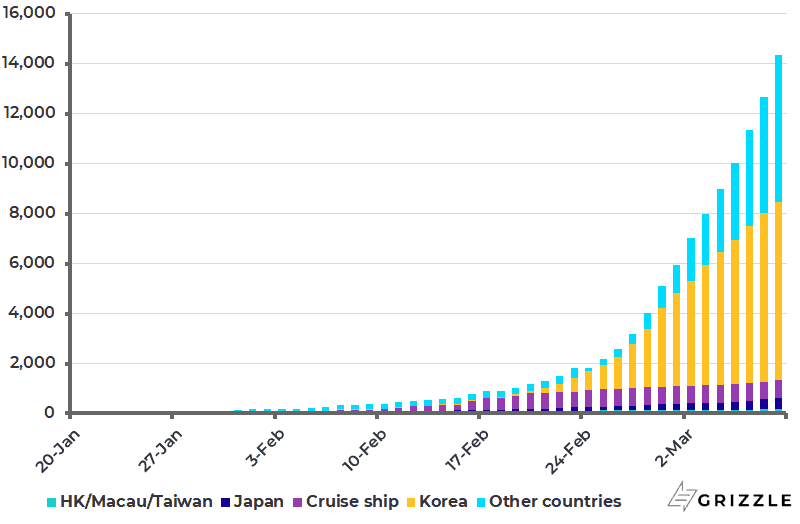

Key Virus Risk Remains Spread Outside China

Here the data has become much more concerning.

There are now 25,520 cases outside mainland China, up from 1,506 cases two weeks ago, including 9,652 cases in Western Europe and 444 cases in America.

Coronavirus Cases Outside Mainland China

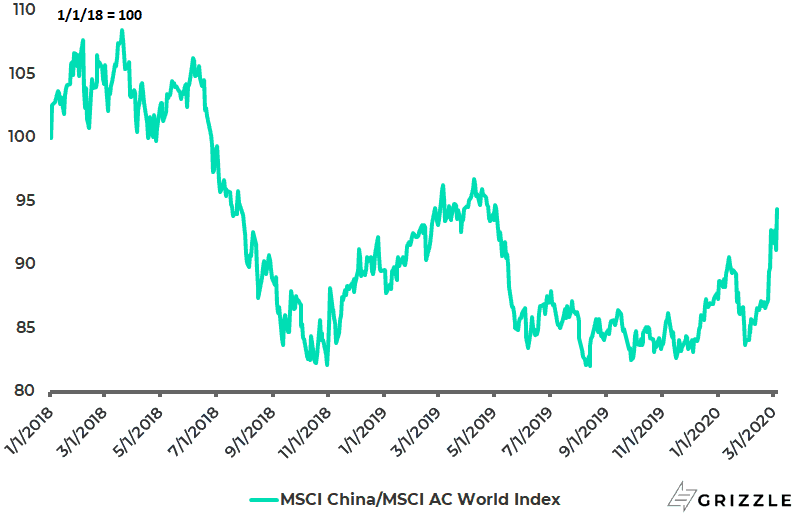

It is this which explains the panic selling in stock markets over the past week. Indeed, China has been outperforming because there is a growing sense that it has seen the worst.

The MSCI China has outperformed the MSCI AC World by 8.6% over the past two weeks.

MSCI China Relative to MSCI AC World Index

If the base case is a return to normality in China in the second quarter as the country gradually returns to work, it is worth noting that there has of late been a flurry of commentary in the Western media focusing on how the mainland authorities’ response to the health emergency has shown up the inadequacies of the political system, and how the Communist Party could be facing a day of reckoning from an aggrieved population.

While it is clearly the case that doctors sounding the alarm in Wuhan were silenced by the local government in the early weeks of the virus in late December and early January, the reality is that the central government imposed drastic measures once the virus threat was officially recognized.

In this respect, it could be argued that the command economy model is much better suited to combating such a health threat than liberal democracies.

The closing off of the province of Hubei, for example, has been ruthless, albeit effective, in the sense that 84% of the total cases in China are in that province which has a population of 59 million.

This is precisely the reason why the risk is now what happens outside China, where the ability to manage such a crisis is much more limited.

The coronavirus certainly poses an unwelcome challenge for the Donald in a presidential election year.

For he had been looking to run in the coming election campaign on a strong economy.

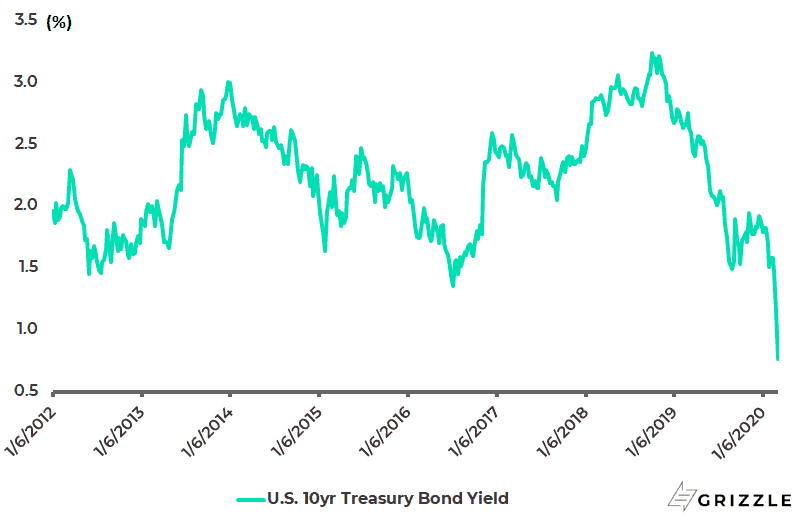

This is now at risk, as signalled by the dramatic rally in the U.S. bond market in the past two weeks with the 10-year Treasury bond yield reaching an all-time low of 0.66% on Friday.

U.S. 10-year Treasury Bond Yield

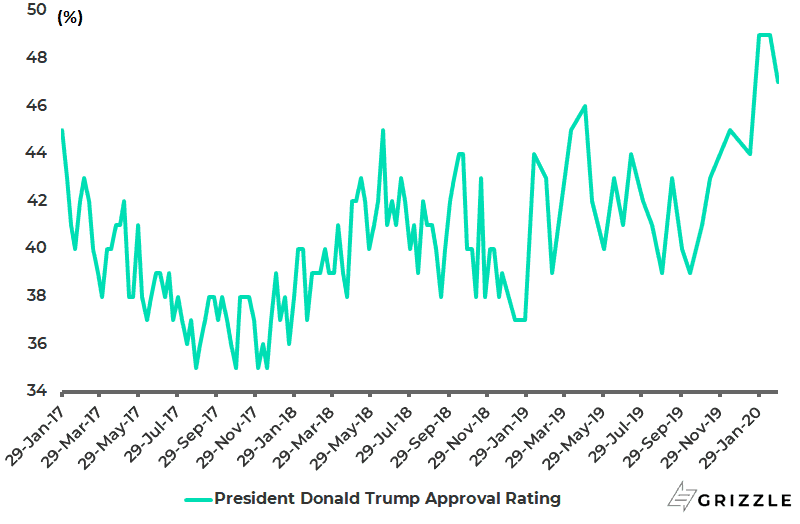

This is unfortunate for the 45th American President since he recently enjoyed the best approval rating since he became president.

The Gallup reported on Feb. 4 that Trump’s approval rating rose by 5% points to 49% in a poll conducted between Jan. 16-29, the highest rating since he took office in January 2017.

President Donald Trump’s Approval Rating

That approval rating came in a particularly good week for the Donald given his upbeat State of the Union Address coincided with the defeat of the impeachment effort in the Senate and the cock-up in counting the votes in the Democratic caucuses in Iowa.

Still that may have been the peak with the Donald’s latest approval rating falling in late February to 47%.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.