The ESG boom may have peaked in the fourth quarter of last year.

If that is just a judgement call, the catalyst for it is the wake-up call provided by the Russian invasion of Ukraine.

This has highlighted the astonishing dependence of Europe on Russian energy and brought renewed focus on the precipitous decision of Frau Merkel to wind down nuclear power back in 2011.

The result has been continuing European reluctance to stop imports of Russian energy even as the political pressure has grown in America, which is much less impacted, to stop buying Russian energy.

For the record, Russia accounts for around 40% of Europe’s gas imports and coal imports and more than 20% of oil imports.

While the Biden administration announced on 8 March that it will stop buying Russian oil, gas and coal, Europe is still in discussions about what to do.

Clearly, a lot of the dependence on Russian energy is not just the consequence of Merkel’s reaction to Fukushima.

It is also the result of the unintended consequences of political greenery, with Western politicians last year competing to talk like the now 19-year-old Greta Thunberg.

British Prime Minister Boris Johnson was the winner in that particular “race to zero” competition with unfortunate consequences for British people’s energy bills.

But fortunately, common sense is now entering the debate.

One signal was the significant decision in early February by the European Commission, doubtless pushed for by French President Emmanuel Macron, to declare nuclear as a green energy along with natural gas.

But perhaps even more notable was the announcement by German Vice Chancellor Robert Habeck, the “economy and climate minister”, on 27 February that Germany would consider stopping its long-planned phase-out of nuclear energy.

It has been estimated that if Germany turns back on the recently decommissioned three nuclear plants, and cancels the original plan to turn off the other three by the end of this year, that will be enough to replace 11bn cubic metres of natural gas a year, which is one eighth of Germany’s current energy needs.

It should be noted that Habeck was a co-leader of the Green Party until late January.

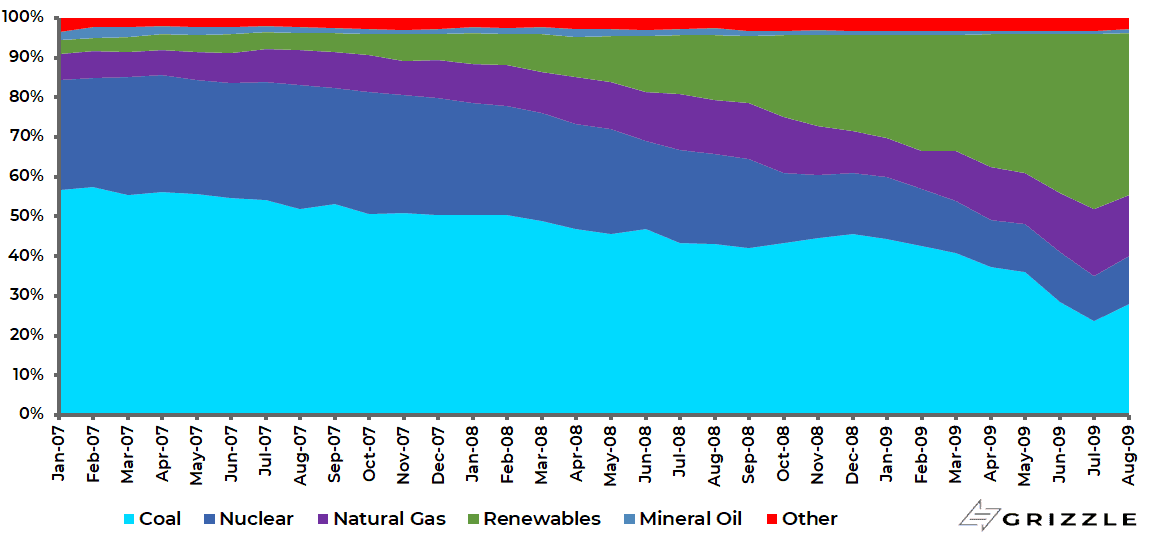

It should also be noted that back in 2000 nuclear accounted for 30% of Germany’s power consumption, though still well below France’s current 70% share.

Share of Germany electricity generation by energy source (%)

Meanwhile, as a direct result of this reduced dependence on “clean” nuclear energy Germany’s dependence on “dirty” coal went up.

It currently consumes 152m short tons of coal a year of which it produces 118m short tons.

Germany has also been spending US$36bn a year on renewables, mainly wind and solar.

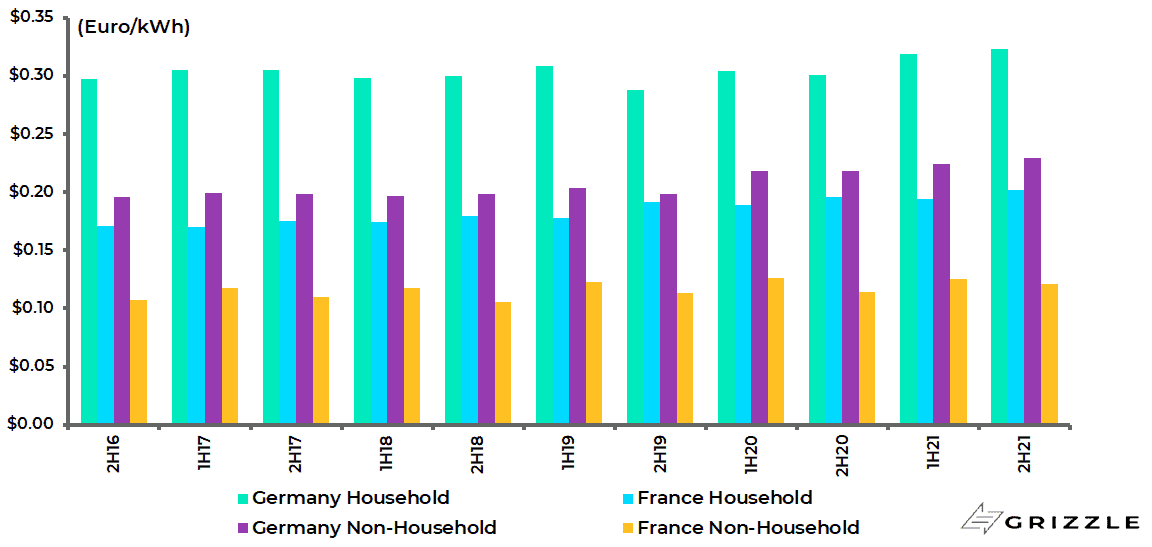

The result of all of the above is that Germany’s electricity is 70% more expensive than its French equivalent while it is also generating more carbon.

It should be noted that natural gas emits almost 50% less carbon dioxide than coal.

Electricity prices in Germany and France

It has long been astonishing to this writer that German industry did not raise greater objections to these policies launched in the Merkel era given the significant impact on businesses’ operating costs.

But that reflects the corporate establishment’s deference to the perceived absolute truths pronounced by the green lobby.

It is also the case that the Volkswagen diesel emissions scandal in 2015 undoubtedly undermined the moral authority of Germany’s automakers to question the strict emission targets which have forced them, by a combination of sticks and carrots, to attempt the transition to electric vehicles.

Meanwhile, it is far from clear that all Germany’s famous automakers will succeed in this transition. It would certainly be imprudent for investors to assume such an outcome.

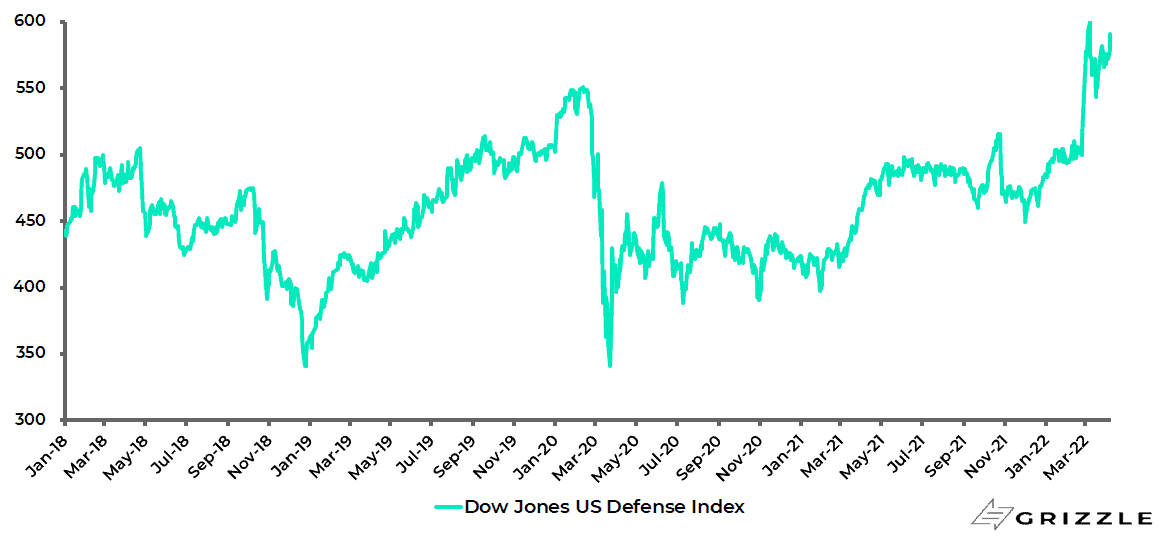

Meanwhile, if these are the consequences of energy policy in the Merkel era, one positive result of Putin’s invasion looks to be a U-turn in German energy policy, just as it has also proved to have been a long-overdue wake-up call in terms of its defence policy, to the long-term benefit of both America’s and Europe’s defence sectors.

US defence stocks are up by 17% since the Ukraine invasion was launched on 24 February.

Dow Jones US Defense Index

This outcome will also not displease the 46th American president.

The Washington establishment will not want to admit it.

But Donald Trump could not have been more vocal about the bizarre state of affairs where Germany relied on American taxpayer dollars for its defence while obtaining most of its energy from Russia.

Nord Stream 2 is Dead But it Could be Revived

As for the Nord Stream 2 oil pipeline, linking Ust-Luga in Russia and Greifswald in Germany, which was another target of the Trump administration, the project has now been mothballed though it could conceivably be re-activated if the current war ends up triggering a change of regime in Russia.

After all, the pipeline has been built.

Certainly, stranger things have happened.

As for who is bearing the €9.5bn cost of Nord Stream 2, half of the cost has been financed by five European energy firms, including Germany’s Uniper and Wintershall, while the rest has been borne by the owner Gazprom.

The ESG Trend has Peaked

Returning to the subject of ESG, the view here is that it has peaked as a trend, not that the movement has ended.

If the latest trigger for a reappraisal has been the Ukraine-triggered energy surge and a related rethink as regards the value of so-called stranded assets, the reality is that an energy crisis was already brewing as discussed here nine months ago (A Third Major Oil Crisis Is On The Horizon, 22 July 2021).

That ESG is being reappraised has become clear in recent months with the long overdue but heathy focus on so-called “greenwashing”.

BlackRock CEO Larry Fink stated in his widely followed annual “Letter to CEOs” published in January that blanket divestment from fossil fuels was not on the agenda (and that stakeholder capitalism was not “woke”), Warren Buffett has publicly defended the oil and gas industry.

The renowned British investor Terry Smith also criticised Unilever in January for having “lost the plot” with lots of talk about sustainability while neglecting operating and financial performance.

Still, going forward, there is likely to be more focus on the S and the G and less on a highly politicised interpretation of the E.

In which case ESG will become more like good old corporate governance which is what all good bottom-up focused equity investors have always paid attention to anyway.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.