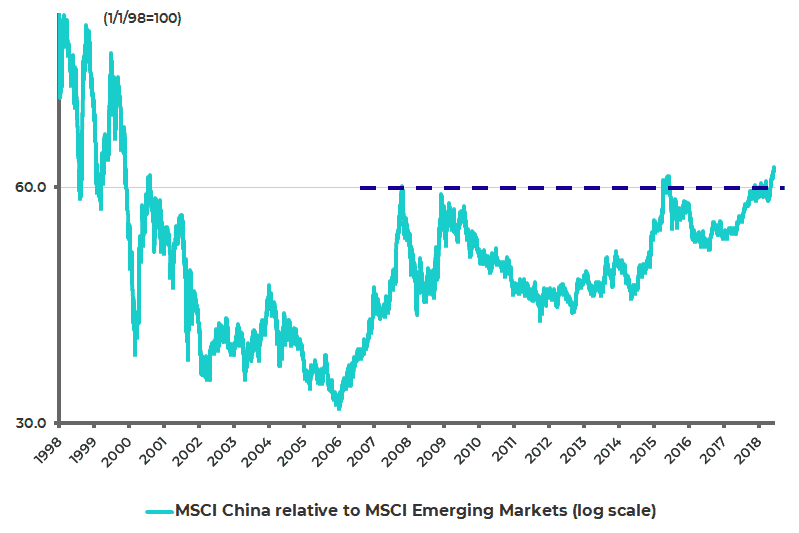

There remains a lot of noise about incipient trade wars and the like between the US and China. But, interestingly, the MSCI China Index, which mainly comprises Hong Kong and New York listed China stocks with a very small weighting in Shanghai-listed A shares, has just broken out of a decade long trading range relative to the MSCI Emerging Markets Index, which tracks all global emerging markets (see following chart).

MSCI China Relative to MSCI Emerging Markets (Log Scale)

Bond Defaults — Beijing Takes Away Safety Blanket

The positive stock market action highlights that the Beijing authorities continue for now to be successful implementing a deleveraging campaign to reign in so-called ‘shadow banking‘ without sinking the economy. One symptom of this intensifying deleveraging campaign this year has been a growing number of bond defaults. There have already been at least 22 bond defaults so far this year.

After years of bailing investors out through the back door, it seems that the time has arrived in China when investors actually lose money when bonds default. More importantly, the central government has sent out the message this year that it is willing to let so-called local government financing vehicles (LGFVs) default, most particular where the entity’s legal status is murky and has not been specifically guaranteed by a local government.

The reality of bond defaults in China can be interpreted both positively and negatively. It is clearly positive that the government seems intent on unwinding the plague of pseudo guaranteed funding that characterized the shadow banking boom in recent years and which caused so-called ‘wealth management products’ (WMPs) to grow to a recent peak of Rmb29.8 trillion at the end of last September or 12.1% of total Chinese bank assets.

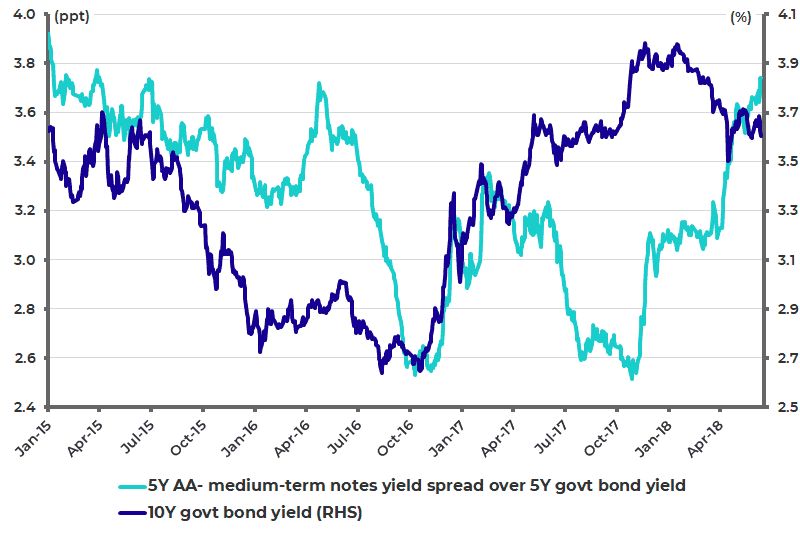

It is also a positive and healthy development that China’s bond market is starting to price credit risk, which is the direct consequence of the defaults. This can be seen in the rally in the sovereign bond market this year and the rise in credit spreads. Thus, the 10-year Chinese government bond yield has declined from a high of 3.98% in mid-January to a low of 3.50% in mid-April and is now 3.60%. While the yield spread between 5-year AA- corporate medium-term notes and 5-year government bonds has risen from a low of 251bp in late October 2017 to a three-year high of 374bp at present (see following chart).

China 5Y AA- Corporate Note Yield Spread and 10-year Government Bond Yield

Still there is also a potential negative point to consider in the sense that such a deleveraging campaign has potential negative liquidity consequences for the stock market.

In this sense, the decision in late April to extend the deadline for meeting the new rules for existing asset management products, which include WMPs, from the middle of 2019 to the end of 2020 came as a relief. That said, it should also be stressed that the extension of the deadline does not represent a ‘cop out’ on the part of the regulators. The new rules are tough and they already apply to newly issued asset management products. For this reason, it is extremely likely that bank WMP issuance has peaked for all time.

The conclusion from all of the above is that the Chinese investment story remains all about whether the authorities can continue to manage this delicate balancing act in terms of securing the necessary deleveraging without inflicting too great a collateral damage on the real economy.

So far this assumption has been correct but clearly there is room for sentiment to turn more negative as bond defaults mount and as there is evidence of more pain for the real economy.

Infrastructure Investment Taking it on the Chin

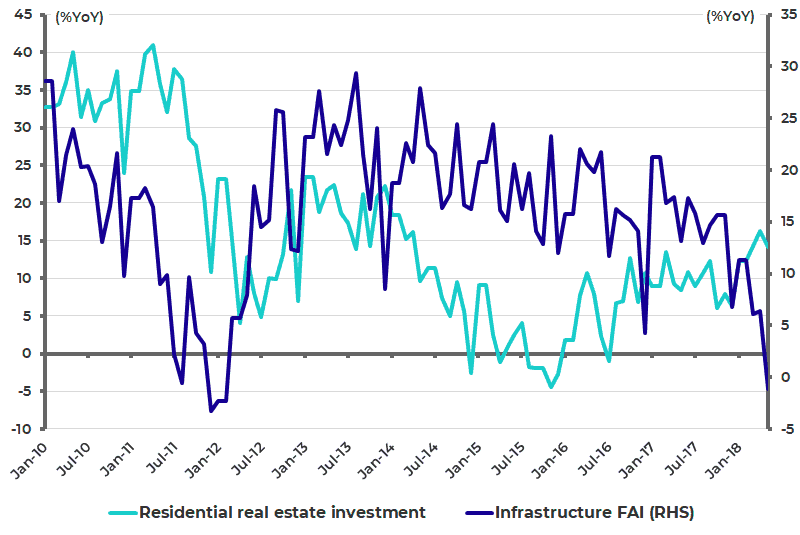

One example of the latter is the sharp decline in infrastructure investment growth so far this year as LGFV financing has been squeezed. Thus, infrastructure fixed asset investment rose by only 5%YoY in the first five months of this year, compared with 16.7%YoY in the first five months of 2017 (see following chart).

So far this has been compensated for, from a fixed asset investment standpoint, by the surprising resilience in property investment. Residential real estate investment rose by 14.2%YoY in January-May, up from 10%YoY during the same period last year. In this respect, the same deleveraging agenda which is causing a financing squeeze for smaller developers is creating opportunities for larger players to take market share, just as China’s so-called supply-side reform has already triggered consolidation in the coal, steel and cement sectors benefitting the larger players and reducing excess capacity.

China Infrastructure Fixed Asset Investment and Residential Real Estate Investment

Credit Tightening By Design

If one reason to bet on the central government’s ability to maintain the delicate balancing act is Beijing’s track record thus far in managing the economy, the other reason is the fundamental point that the authorities have induced this deleveraging by their own policies.

This is the critical difference with the US’ so-called subprime mortgage crisis more than ten years ago. For the latter was a spontaneous market-driven implosion where regulators and policymakers in Washington were totally unprepared. This is not the case in China. While the authorities undoubtedly let shadow banking grow too big, they long ago identified the problem and have been acting for some time to address it. They also have palliatives to ease the pain such as orthodox monetary easing,

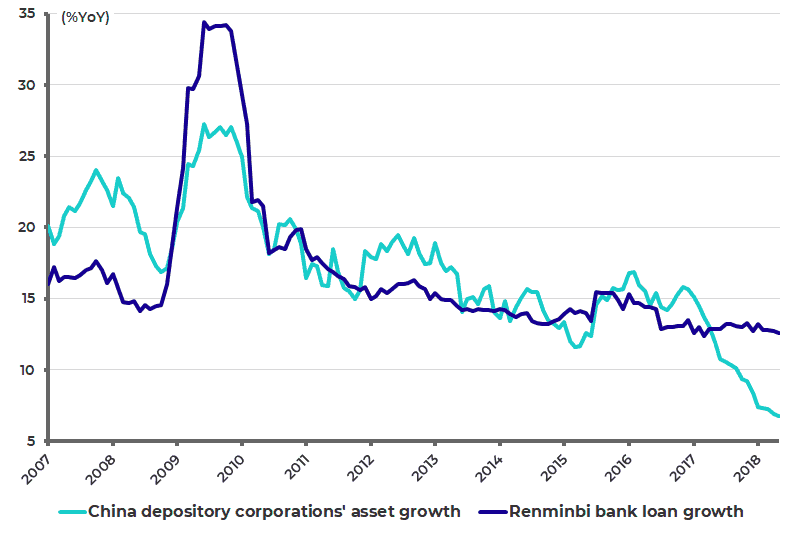

Meanwhile, there is no doubt that credit is contracting in China. Overall bank asset growth has declined dramatically even as bank loan growth has held up. This phenomenon reflects the reality that loans previously held in shadow banking vehicles have been brought back on balance sheet as a result of the regulatory squeeze. Depository corporations’ total asset growth slowed from 15.8%YoY in November 2016 to 6.8%YoY in May, while renminbi bank loans rose by 12.6% YoY in May (see following chart).

Normally such a decline in bank asset growth would look very bearish. But, as is so often the case, China plays by different rules. The point to remember is that China was heading for a potentially devastating wholesale financing crisis if shadow banking had been allowed to continue to boom. Like an unruly dog, it is now being brought to heel.

China Bank Asset Growth and Renminbi Bank Loan Growth

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.