The US presidential election appears to be finally over.

But it remains unclear how the issue of regulation of “Big Tech” will be impacted by the outcome.

In the final days of the campaign, Donald Trump began targeting Big Tech in his speeches.

This seemed to follow the extraordinary development in October whereby Facebook and Twitter removed a New York Post article about Joe Biden’s son Hunter from their platforms.

This clearly politically motivated interference with content on “platforms” in the midst of a presidential campaign has raised front and centre again one of the issues raised as regard the mounting regulatory risk to the “tech behemoths”; though in this case the risk really applies to the platform companies.

This is that social media companies should be held responsible for the content they carry whereas at present Section 230 of the US Communications Decency Act of 1996 shields them from any liability for content published on their platforms, including material that could be considered defamatory.

But clearly, when social media companies start editing or censoring content for politically motivated reasons, it is obvious that they have become in effect media companies.

For anyone who wants to read a detailed account of this latest development, this writer recommends an article last month from The Intercept by Glenn Greenwald (“Facebook and Twitter Cross a Line Far More Dangerous Than What They Censor”, 16 October 2020).

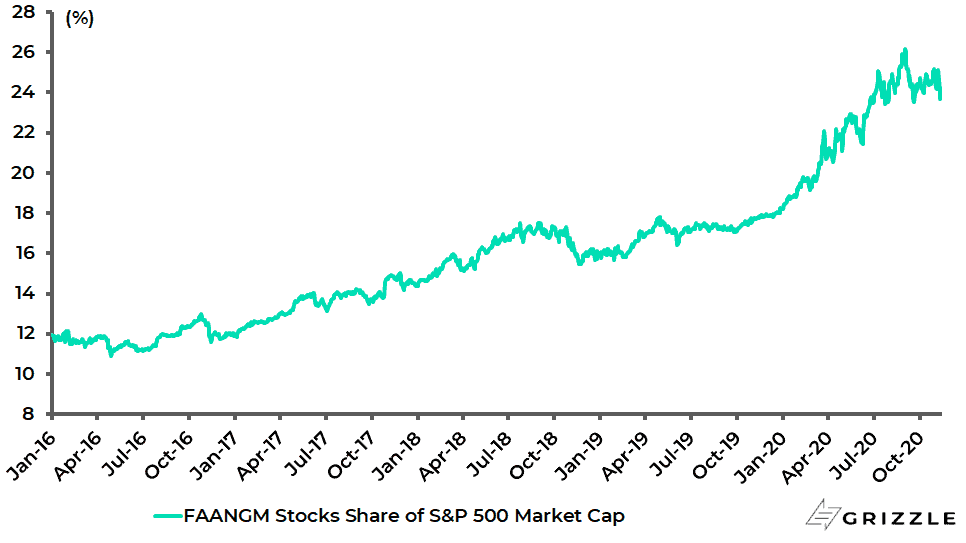

US Big Tech’s Share of S&P500 Market Cap

Tech Needs to Keep the Democrats Close

The above episode makes it more likely that Big Tech, and in particular the platform companies, will be targeted by both the political right and the political left in the coming years.

This means Silicon Valley will depend for its protection on the Democratic Party establishment which it is effectively in bed with.

With Joe Biden elected, it will be interesting to monitor the tension between the party establishment and its progressive wing on this issue.

Meanwhile, it is also clearer than ever that conventional media made a huge mistake when it allowed its content to be displayed on Google’s and Facebook’s newsfeeds in the search for eyeballs.

As the New York Times’ commercial success in the Trump era has shown, people will pay for quality editorial content.

This writer recommends all media organizations to remove their content from the “platforms” and only distribute to paying customers on their own websites.

Meanwhile, the Donald noted in his closing speeches that the New York Times and CNN will take a commercial hit if he loses, as he has.

This may well prove to be the case.

Chinese Tech Regulation: Ant Group Edition

Meanwhile, the issue of Big Tech regulation is not just confined to America.

What would have been the biggest IPO ever in Hong Kong was pulled on 3 November or two days before scheduled because of failure to meet regulatory requirements.

This was the US$35bn IPO of China’s premium fintech Ant Group, part of the Alibaba group.

The Shanghai part of the dual-listing was looking to be 200-300x oversubscribed, which means that up to Rmb12-24tn (US$2-4tn) would have been set aside for the listing.

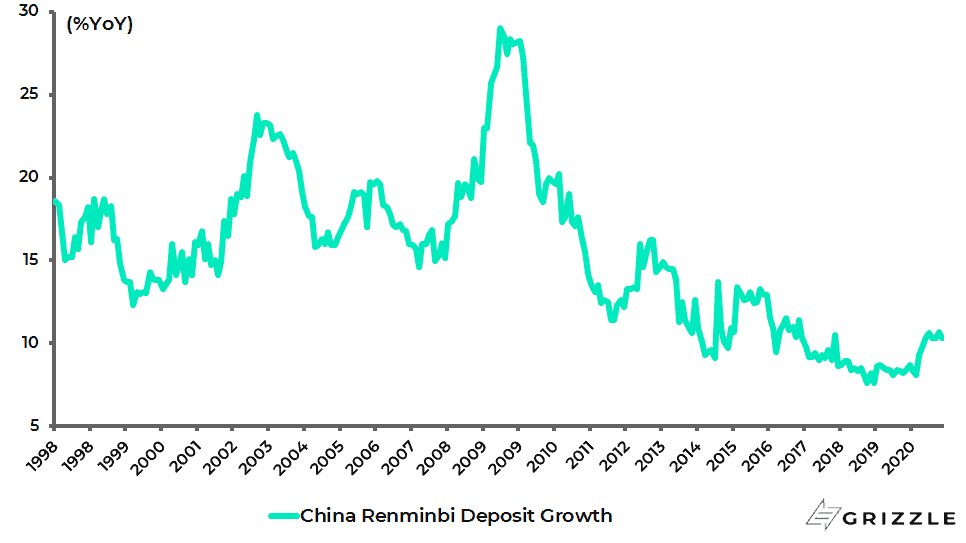

As regards the mounting hype surrounding Ant Group itself, prior to the IPO, investors were at risk of forgetting that the Chinese Government is not going to allow a fintech platform to disintermediate completely its conventional banking system where ordinary people’s savings are held, and where total deposits continue to grow at a healthy 10.3% YoY in October.

Household deposits totaled Rmb90tn (US$13.7tn) at the end of October, up 13.5% YoY.

China Renminbi Deposit Growth

The other issue is how China’s successful payment platforms like Alipay will interact with the digital renminbi which has now been launched in pilot schemes by the PBOC as previously discussed here (see Own Decentralized Assets, Digital And Physical – Bitcoin and Gold, 10 June 2020).

Such regulatory issues became clear when the Ant IPO was pulled by the mainland authorities.

Regulators from four government bodies, including the People’s Bank of China (PBOC) and the China Banking and Insurance Regulatory Commission (CBIRC), held a supervisory meeting with Ant Group’s controlling shareholder Jack Ma and two other senior executives on 2 November.

This coincided with the publication by the CBIRC and PBOC of new draft rules for online micro-lending businesses on the same day, which would force Ant and other operators of online lending platforms in China to fund a greater share of the loans they offer together with banks.

The next day the Ant Group’s dual IPO was postponed two days before the company was meant to list because Ant had not complied with certain regulatory requirements.

The regulators want to ensure that the proper rules are in place, in terms of the role fintech will play in driving consumption via the provision of credit, in the next growth cycle.

In this respect, Ant is heavily involved in consumer lending.

As for the draft measures themselves, they seem sensibly prudential.

The rules cap the size of loans at Rmb300,000 for individuals, or one-third of average annual income earned in the past three years, while lending to corporate entities should be less than Rmb1m.

Online micro-lending platforms are also required to contribute at least 30% of loans funded jointly with banks, up from the current 1%-20%.

As for Ant Group itself, it changed its name from Ant Financial ahead of the announcement of the IPO in August, with the current full name Ant Technology Group.

This was to emphasise that it views itself as a technology company, not a financial company.

Still, the reality is that its business model is heavily geared to consumer lending.

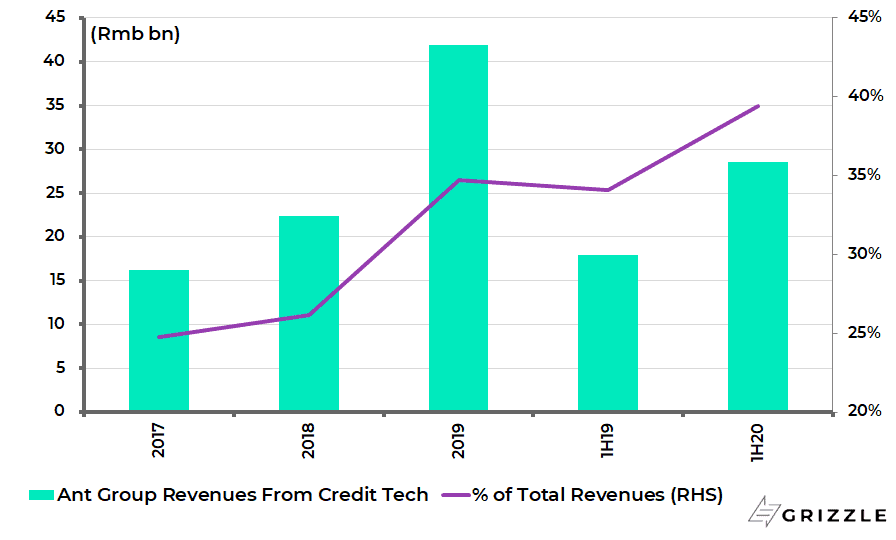

The micro-loan technology platform, namely CreditTech, generated Rmb28.6bn in revenue for Ant Group in the first half of 2020, accounting for 39.4% of its total revenues.

Ant Group’s revenues from online lending platform CreditTech

The annualized interest rate of Ant’s consumer loans is about 15%, which compares with the 15.4% interest rate ceiling for consumer lenders imposed by a recent Supreme Court ruling.

Meanwhile, Ant’s prospectus shows that only a tiny 2% of Ant Group’s Rmb2.15tn of credit extended is funded with its own money, with the rest funded by banks or asset-backed securities.

This will now change as the regulators want Ant to have more “skin in the game”.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.