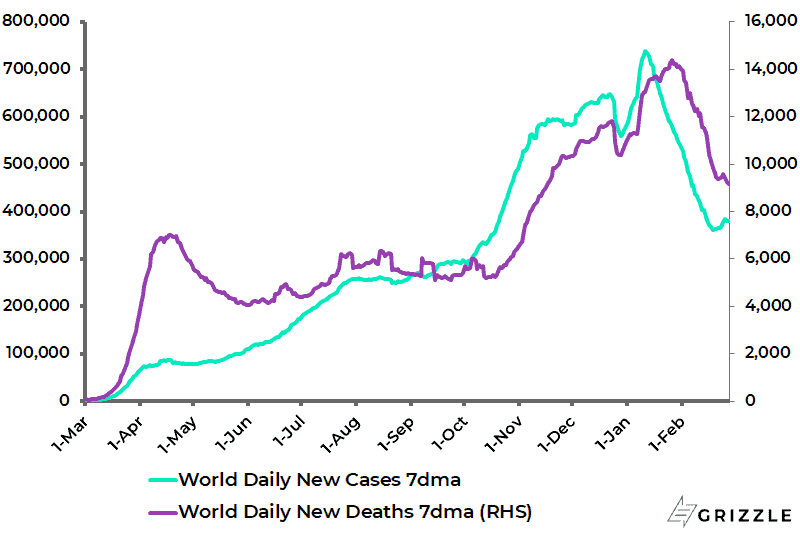

Covid cases continue to decline on a global basis as vaccine rollouts continue.

The 7-day average daily new case count globally has declined by 48% since peaking on 11 January to 380,761, while the 7-day average daily death count is down 36% from the peak of 14,377 reached on 26 January to 9,163.

World Covid 7-day average daily new cases and deaths

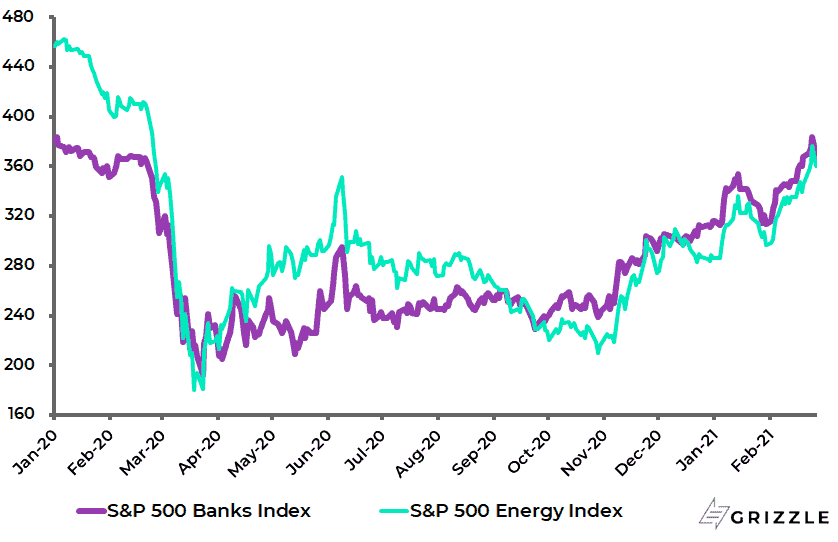

This is the foundation for the pro-cyclical trade which continues to work as reflected in the significant rally in US bank stocks and US energy stocks in recent months, and as also reflected in the continuing sell-off in the US bond market which finally caught the headlines this past week.

The S&P500 Banks Index and Energy Index have risen by 53% and 72% since late October 2020.

S&P500 Banks Index and S&P500 Energy Index

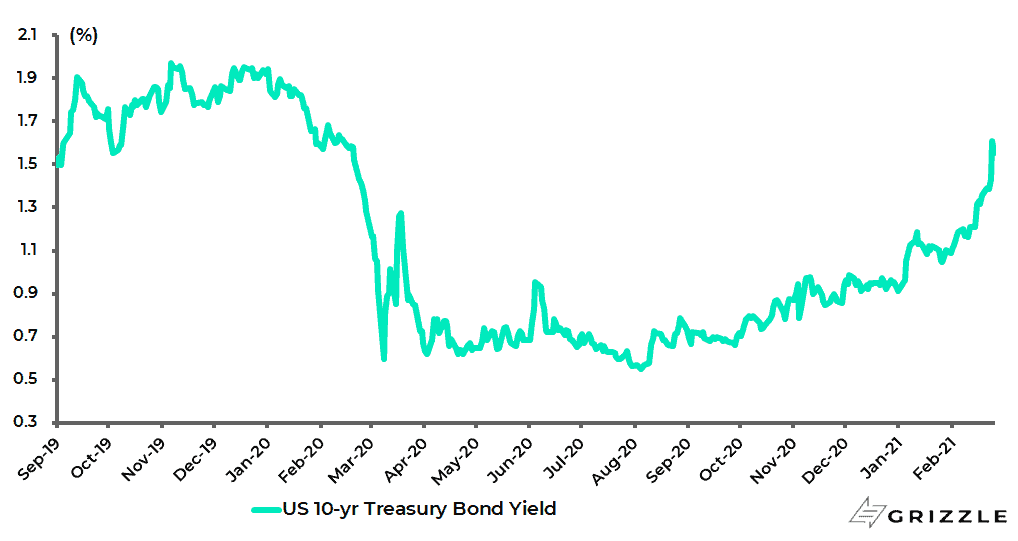

While the 10-year Treasury bond yield surged from 0.91% at the end of 2020 to an intraday high of 1.61% on 25 February, the highest level since mid-February 2020, and closed last week at 1.40%.

US 10-year Treasury Bond Yield

The biggest risk to this pro-cyclical outlook is clearly the efficacy of vaccines, most particularly as it relates to the mushrooming new variants, be it the British variant, the South African one or the Brazilian one.

A particularly alarmist headline occurred in Britain in late January when there were news reports that Britain’s Health Secretary, Matt Hancock, had told a webinar meeting with business leaders and travel agents that the South African variant reduced the vaccine efficacy by 50% while adding that “I wouldn’t say that in public”.

A recording of the speech was duly, and predictably, leaked to the media (see Sky News article: “COVID-19: Matt Hancock says South African variant could reduce vaccine efficacy by half”, 23 January 2021).

If this is the concern, the evidence so far suggests that the problem can be addressed by tweaking existing vaccines.

That at least is the encouraging message which has been delivered by Moderna CEO Stéphane Bancel in late January when the company announced vaccine trials to tackle the British and South African strains.

Still, if the company is confident that its so-called messenger RNA (mRNA) technology can be quickly adapted for new variants, there is also another less positive, but potentially very realistic point which has been made by Bancel.

That is that Covid may, like the flu, be with humans “forever”.

That means, like the flu, a new vaccination will be required at least every year.

If this is indeed the case, there are two obvious public policy conclusions.

The first is that the regulatory process needs to be speeded up to approve the tweaked vaccines.

The second is that the world needs to get used to living with the virus, just as the world has long ago learned to live with the flu, and stop trashing the vulnerable sectors in the economy.

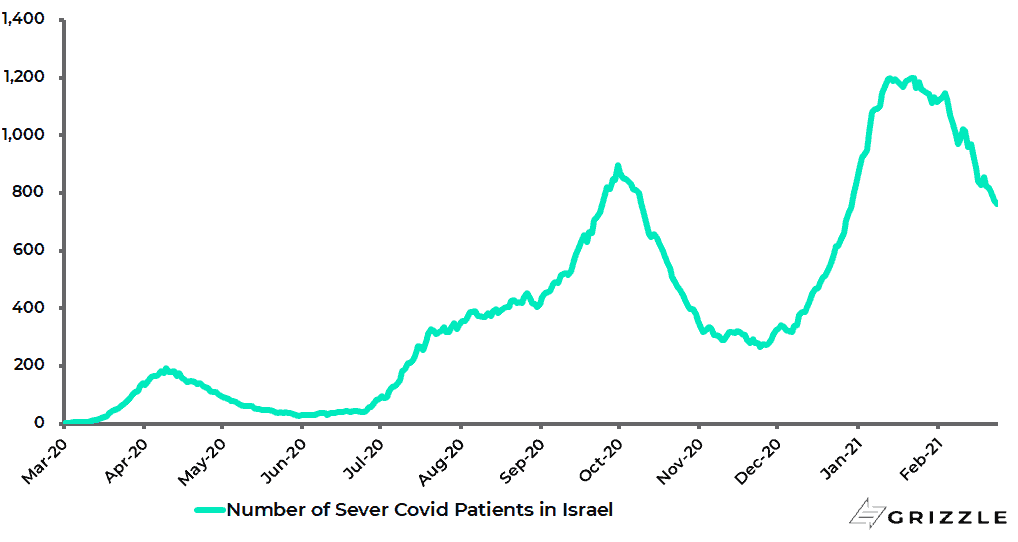

Watch Israel for Confirmation the Vaccines Work

Meanwhile, investors should be focused on Israel in terms of monitoring the efficacy of a highly organised vaccine rollout.

As of 26 February, 53.9% of Israelis have received at least the first Pfizer shot, and 38.1% have received the second shot.

The number of hospitalised Covid patients in serious condition in Israel has declined by 37% from the peak reached on 26 January to 760, according to the Ministry of Health.

Israel Number of Severe Covid Patients

Still, it should be noted that the Ben Gurion airport has also been closed since late January to guard against the new more infectious variants while the vaccine is rolled out.

Meanwhile, there is a clear political motivation for the government of Prime Minister Benjamin Netanyahu, that ultimate political survivor, to get this right since yet another general election is due to be held on 23 March. That will be the fourth general election in two years.

The risk in all of the above is that the new variants appear to be more infectious.

Hence the critical issue is whether the mRNA technology is as flexible in handling mutations as the likes of Moderna believes.

Will the Virus Aftermath Lead to Greater Euro Unity?

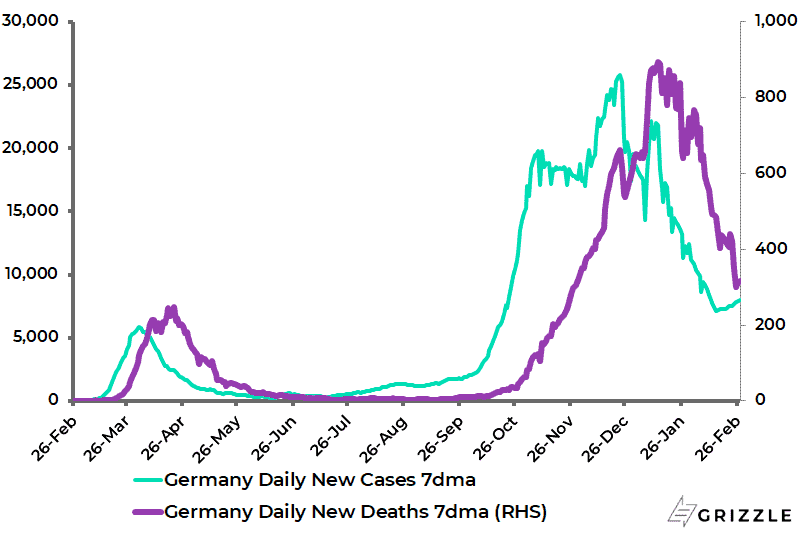

Staying on the subject of Covid and politics it remains the case that, despite the renewed Covid surge in Germany in recent months (though the 7-day average daily case count has declined by 69% since peaking on 23 December, Angela Merkel’s position politically has been strengthened by her perceived competent handling of the pandemic in stark contrast to what happened to Donald Trump.

Germany 7-day Average Daily Covid Cases and Deaths

This was seen in the results of the CDU leadership contest held on 15-16 January when her candidate, Armin Laschet, prevailed over the more right-wing Friedrich Merz identified with the faction of the party led by Wolfgang Schäuble, Germany’s finance minister between 2009 and 2017.

That sets up the CDU for a coalition with either the SPD again or perhaps the Green Party after a general election which is due to be held in September this year.

Such a coalition would likely be Eurobond friendly and would suggest further moves towards fiscal integration in the Eurozone.

It will be interesting to see if Frau Merkel, already 15 years in power, decides to linger longer as Chancellor now that she no longer has to deal with Donald Trump, with whom her relationship was bordering on the non-existent.

It is easy to forget how long Merkel has been in power, namely 15 years.

She has already been German Chancellor more than three years longer than the late and great former British Prime Minister Margaret Thatcher who, first elected in May 1979, was disgracefully removed from power in November 1990 by a coup engineered by a Tory old boy network.

But Thatcher, a conviction politician, is a very different person from Merkel who is the precise opposite.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.