Ever had one of those “aha” moments when you realize something’s not just good, it’s gold? That’s what’s happening with nuclear power. It’s green, safe, and reliable – a triple threat in the world of energy.

But hold your horses, it’s not all sunshine and roses. We’re about to dive into the nitty-gritty of nuclear power’s comeback, its challenges, and the geopolitical tango that’s got the world on its toes.

If you’d like to learn more about the developing uranium crisis, including investment ideas, visit the Grizzle Research Substack

The Resurgence of Nuclear Power

After some ups and downs, nuclear power is back in the limelight, and for good reasons. It’s seen as a knight in shining armor for environmental protection, a break from fossil fuels, and a powerhouse for electrifying transportation and industry.

With over 60 nuclear reactors in construction (21 in China alone) and plans for another 110 (70 of those plans are also in China), the world’s gearing up for a nuclear-powered future.

Even at the recent Dubai climate conference, 22 nations pledged to triple their nuclear capacity by 2050.

Already a Constant in the Energy Mix

Nuclear power isn’t new. In fact, it’s been strutting its stuff for a while now. It powers nearly 20% of the US’s electricity ( 50% of the total zero-carbon share) and about a quarter of Europe’s, with France leading the charge at 68%.

But here’s where the plot thickens. We’re staring down the barrel of a triple threat:

- A global shortage of uranium production,

- A bottleneck in enrichment processes

- Geopolitical chaos that’s got everyone biting their nails.

Geopolitical Chess Game

The US, in a belated eureka moment, has once again recognized nuclear energy production as a national security issue. But, in a classic case of “look before you leap,” the US House of Representatives recently voted to ban Russian uranium imports without a backup plan, and Russia, not missing a beat, threatened to cut off supplies immediately.

The Irony of Funding Both Sides

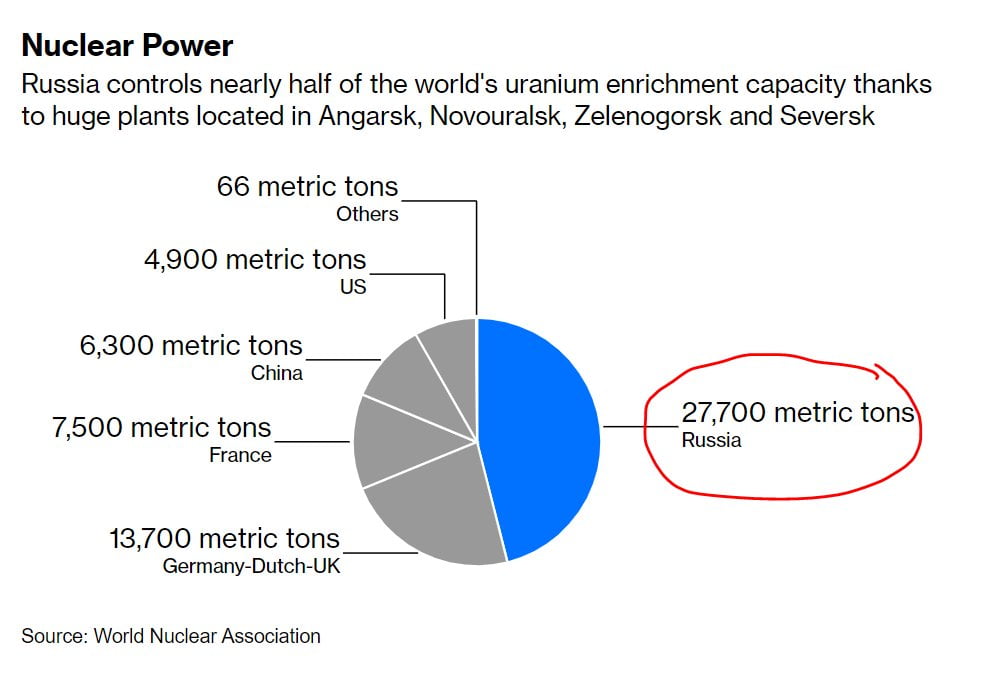

Here’s a head-scratcher – the uranium supply chain runs from Kazakhstan through Russia, accounting for a whopping 40% of US supply. And guess who controls half the world’s enrichment capacity? Yup, Russia and China.

American and European ratepayers are inadvertently bankrolling both sides of Russia’s war on Ukraine, with Rosatom pocketing over $1 billion annually from its uranium sales to US utilities.

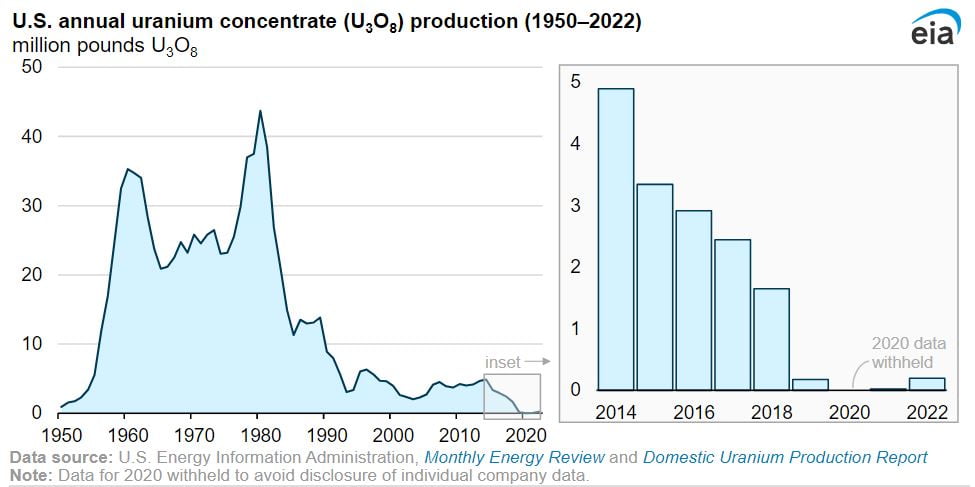

By 2028, Western nuclear utilities alone will need to replace about 40 million pounds of uranium concentrates annually, currently sourced from Kazakhstan. But there’s a catch – production in North America and Europe currently ammount to 96 million pounds while production in non-China/Russia-aligned countries will only amount to about 48 million pounds. You see the problem?

Filling this gap is going to be like climbing a mountain without a rope. We’ve got potential mines in Australia, Canada, and the US, but red tape and environmental concerns are major hurdles.

Enrichment: The Achilles’ Heel

The US hasn’t added new enrichment capacity in ages. Although there’s some momentum with projects by Urenco, Orano, and others, Russia’s Rosatom still controls over 50% of global enrichment capacity.

There’s a narrow window – maybe five years – to ramp up US capacity. But even with a green light from the government, it’s a race against time given deteriorating political conditions between the West and East.

Without new funding incentives and a real push from governmen’t to ramp up local sources of uranium and enrichment capacity, cutting off supply from Russia today could lead to a 1970’s oil embargo type price spike.

Uranium is Now a Key Pawn in a Blobal Energy Chess game

In the grand scheme of things, nuclear power is like a chess game where every move counts.

It’s a golden opportunity to transition to cleaner energy, but it’s tangled in a web of geopolitical and supply chain complexities.

As we navigate this new Cold War-esque landscape, the stakes are high.

The West needs to up its game in uranium mining and enrichment to keep the lights on and stay in control of its energy future. Will we learn from past oversights, or will we be left reminiscing about the days when uranium was as cheap as chips? Only time will tell.

What Should an Investor Do to Take Advantage of This Mess?

The way we see it, there are two segments of the western uranium supply chain that would be the big winners from a reshoring of supply.

- Own the miners: Large miners with high quality resources, like Cameco (Ticker: CCJ), Denison Mines (Ticker: DNN) or NexGen Energy (Ticker: NXE) will see rising free cashflow if uranium prices spike due to supply disruptions. They have large resource ready to begin production if fuel buyers are willing to sign long term supply agreements at prices around $65/lb or higher. With spot prices currently over $85/lb it is likely we will see production ramp up from all three of these companies in the near future.

- Own the Mills: A lesser understood but potentially explosive opportunity is to own the companies will both uranium resource and milling capacity in North America. All uranium dug from a traditional mine, needs to be milled on its way to becoming enriched uranium, though only two companies have licensed and constructed mills in America. Anfield Energy (Ticker: AEM) and Energy Fuels (Ticker: UUUU). If we see rising uranium production in North America, demand for these two company’s mills will be far above their capacity, leading to a period of significant profits.

![]()

FAQ

1. Why is nuclear power making a comeback?

– Nuclear power offers a green, safe, and reliable alternative to traditional energy sources and plays a key role in reducing reliance on fossil fuels.

2. What challenges does the nuclear power sector face?

– The sector grapples with a global deficit in uranium production, enrichment bottlenecks, and geopolitical complexities, especially involving Russia and China.

3. How critical is uranium to the nuclear power sector?

– Uranium is the lifeblood of nuclear power. Control over its supply and enrichment is a strategic advantage in global politics.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.