The “situation” remains the inverse of Goldilocks for Wall Street-correlated world stock markets with the one consolation for investors that President Xi Jinping’s policy of Covid suppression has in recent months been keeping the price of oil lower than it otherwise would be.

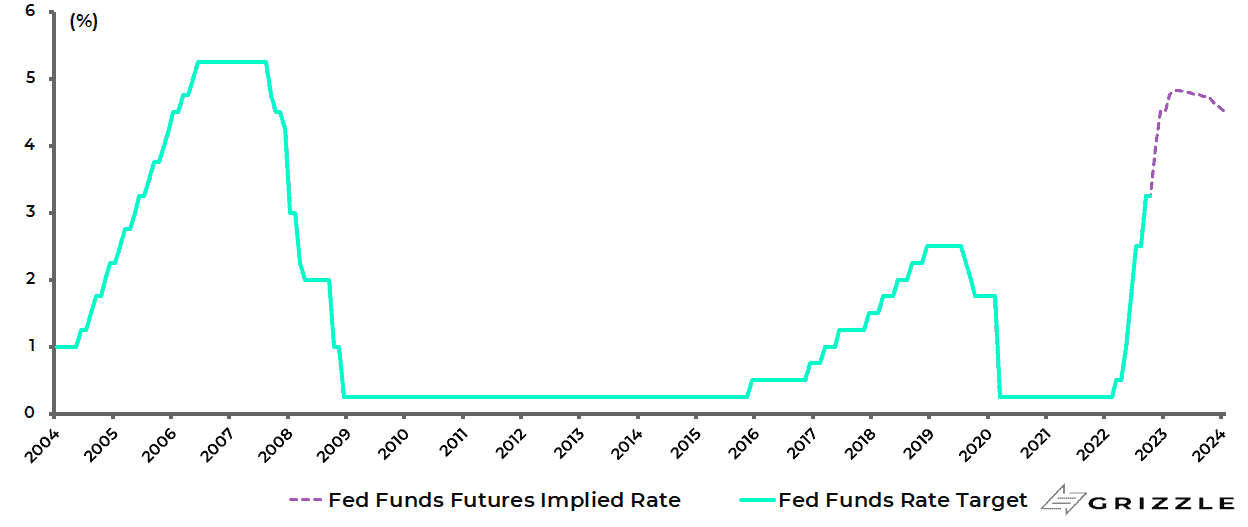

Money markets are still expecting another 150bp of Fed tightening following the 300bp of rate hikes already implemented this year.

While quantitative tightening has now commenced in the US.

Fed funds rate and Fed funds futures implied rate

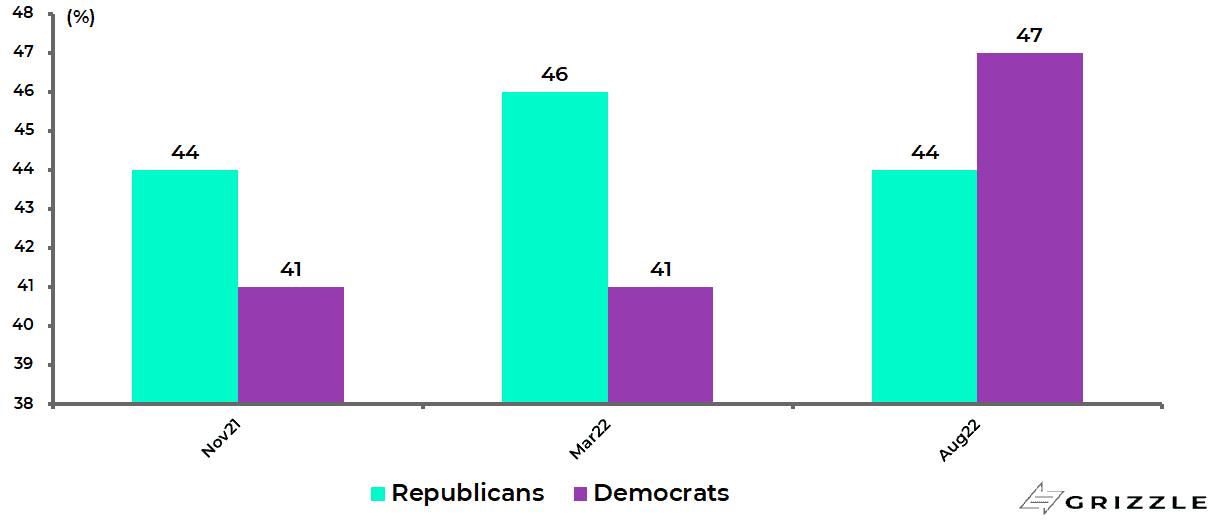

Investors Expect Democrats to largely Hold on to Mid-Term Victories

Meanwhile, with the US mid-term elections now less than two months away, it is worth highlighting that the opinion polls have in the recent past moved in the Democrats’ favour whereas not so long ago the most probable outcome looked to be a Republican landslide.

A Wall Street Journal poll conducted between 17-25 August, for example, shows that 47% of the registered voters support Democrats, compared with 44% for Republicans who had a 5ppt lead back in March.

WSJ US Mid-term elections opinion polls

Source: Wall Street Journal

The Democrats have seemingly benefitted from the abortion issue, where they currently occupy the middle ground following the Supreme Court decision on 24 June to overturn the 1973 Roe v. Wade ruling that established the constitutional right to abortion.

The word is that women under 25 are rushing to register to vote. For example, women have outpaced men in new voter registrations by 11ppts in Ohio, 12ppts in Pennsylvania and 15ppts in Wisconsin since the Supreme Court ruling.

While the decision to cancel up to US$20,000 of student debt per head will also have generated votes. President Joe Biden announced on 24 August a plan to cancel US$10,000 in student debt for those earning less than US$125,000 per year and US$20,000 for those who had received Pell grants, an undergraduate student grant for low-income families.

The result is that the Democrats are now expected to control the Senate with an increased majority while previous expectations of a Republican majority in the House of Representatives are beginning to be questioned.

Clearly, opinion polls have not been that reliable in the past.

Listen Closely to Lael Brainard, Not Powell

But from a market standpoint, it must be wondered whether the Democrats maintaining control of Congress will allow for a more relaxed attitude towards the inflation issue, most particularly if it coincides, as likely, with growing evidence of labour market weakness in coming months.

This is important since political pressure on the Fed from both the executive and legislative arms of government to be seen to be doing something about inflation was a major reason behind Powell’s dramatic U-turn last November, as discussed here previously on several occasions (see, for example, Stocks Think Inflation Has Peaked, Economic Data Says Otherwise, 25 April 2022).

In this respect, it should be noted that Fed Vice Chair Lael Brainard is a labour market specialist.

It should also be noted that she would have been the Fed chair save for concerns that her appointment would not have been approved in Congress because of a lack of the necessary Republican votes.

Brainard is also politically connected since her husband, Kurt Campbell, is the National Security Council Coordinator for the Indo-Pacific in the Biden administration.

For now she is sticking with the hawkish line.

In a speech made in New York on 30 September, her concluding paragraph was that monetary policy “will need to be restrictive for some time to have confidence that inflation is moving back to target” and that, for these reasons, “we are committed to avoiding pulling back prematurely”.

But language can change suddenly at some point in the future.

Remember that in June 2020 Powell said he was not even thinking about raising rates.

This must rank as one of the most irresponsible comments made by a Fed chairman ever, with perhaps the only competition for that ranking Ben Bernanke’s pledge in August 2011 not to raise rates for two years which encouraged all manner of leveraged speculation.

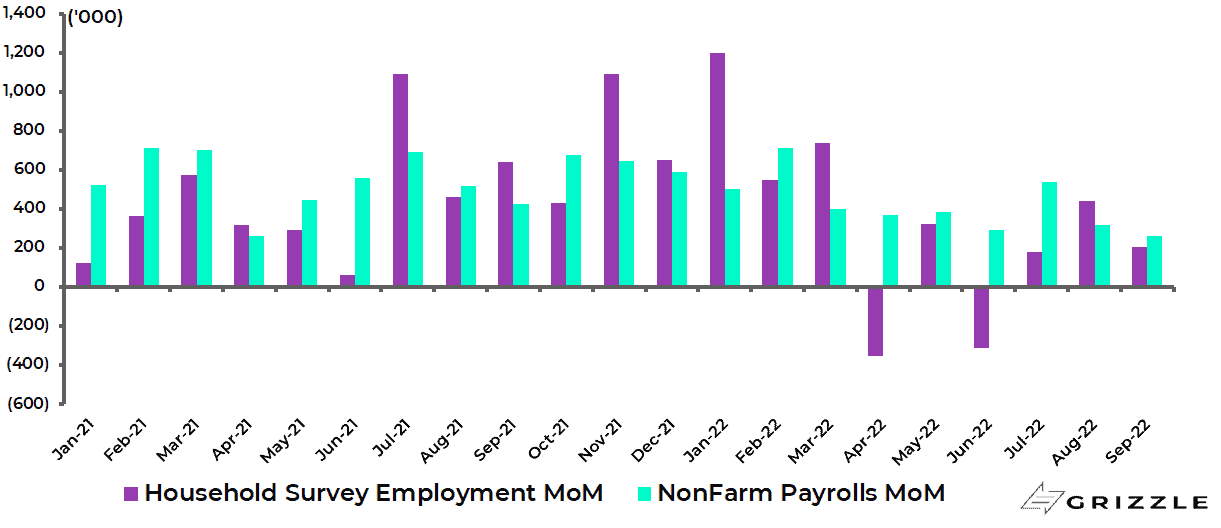

Meanwhile it is worth noting, as regards the labour market, the divergent path in job growth in recent months as reflected in the payroll survey and the household survey.

The household survey employment is up only 478,000 since April.

By contrast, US nonfarm payrolls are up 2.16m over the same period.

US monthly increase in employment

The most likely explanation for this discrepancy is that if a person has three jobs it will count as three in the payroll data but only as one in the household survey.

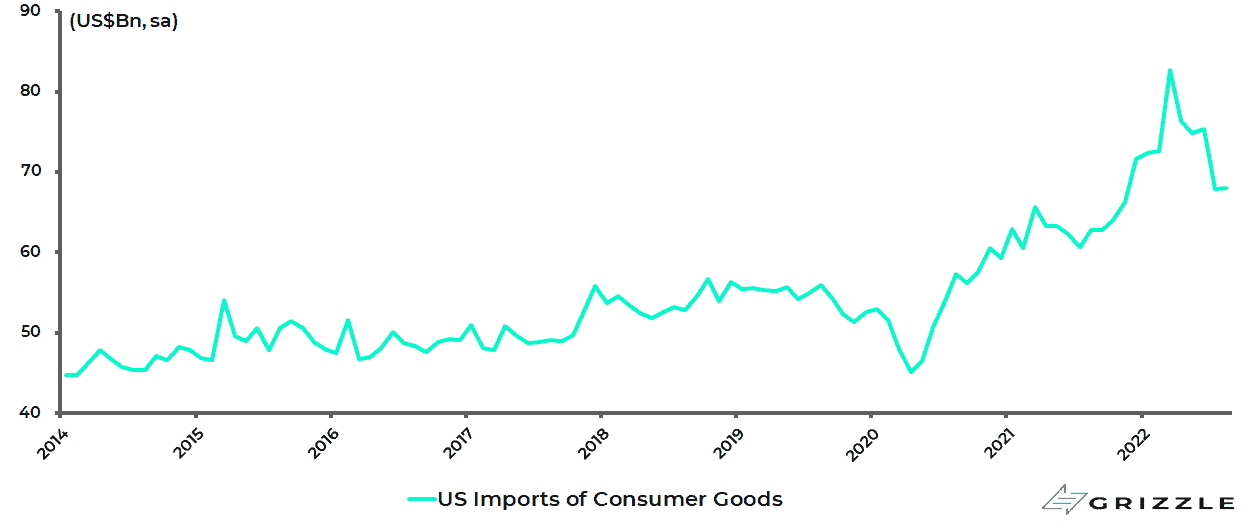

As for a hint of any pronounced slowdown in US consumption in coming months, it is likely to be signalled in a collapse in imports.

There are some initial signs of this.

US imports of consumer goods have declined by 18% from a peak of US$82.7bn in March to US$68bn in August, though they were still up 11.2% YoY in August.

US imports of consumer goods

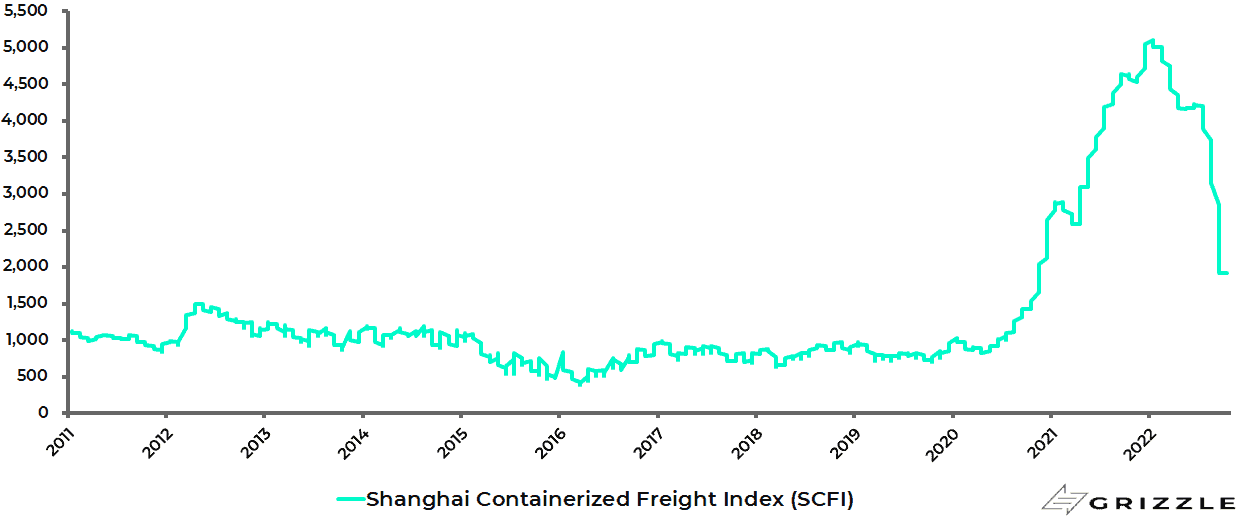

An inventory pile-up is also suggested by collapsing container shipping rates.

For example, the Shanghai Containerized Freight Index is now down 62% from the peak reached in early January.

Shanghai Containerized Freight Index (SCFI)

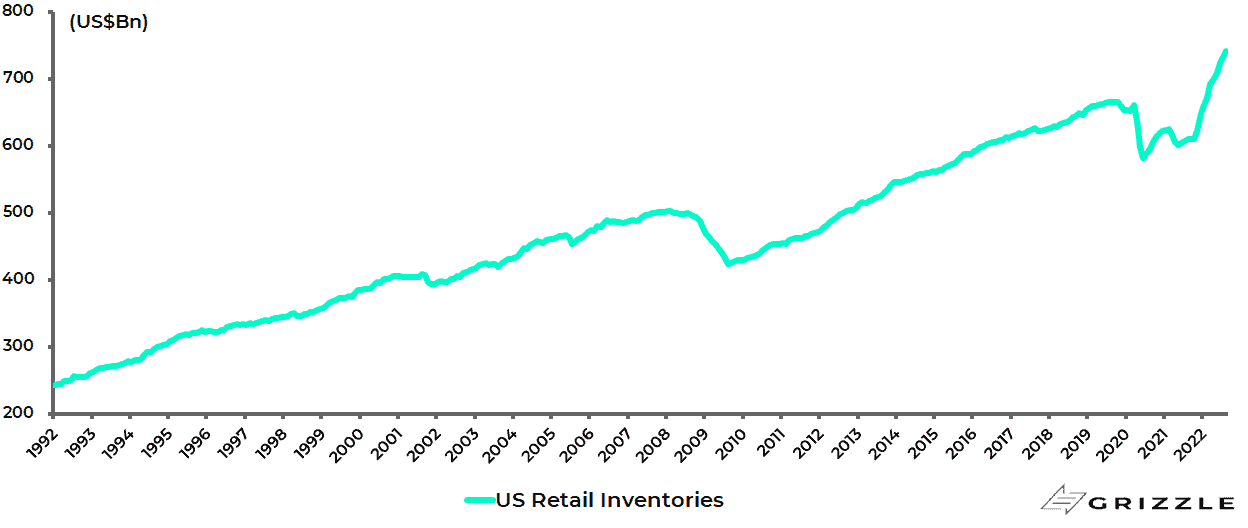

Meanwhile, US retail inventories rose by 21% YoY to a record US$741bn in August (see following chart).

US retail inventories

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.