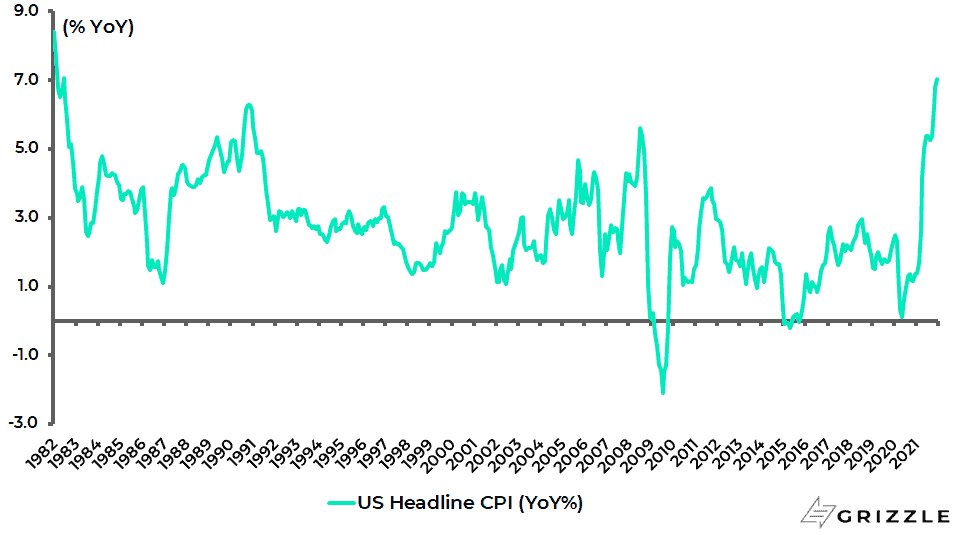

This writer remains of the view that the US CPI report is now the most important US data point monthly rather than the payroll report.

And last week’s CPI release, showing a 7.0% YoY rise in December compared with a year ago and the highest inflation print since the Volcker era in 1982, is again newsworthy.

US CPI Inflation

The dramatic surge in reported US inflation in recent months has caused moderate Democrats, and not just Republicans, to start talking about the need for interest rate hikes.

This reflects a growing concern amongst establishment Democrats, if not the party’s so-called ‘progressives’, that the inflation issue has become a major negative for the Biden administration ahead of November’s mid-term elections, as also reflected in recent polling data.

An ABC News/Ipsos poll published in mid-December showed that only 28% of Americans approved of Biden’s handling of inflation while 69% disapproved.

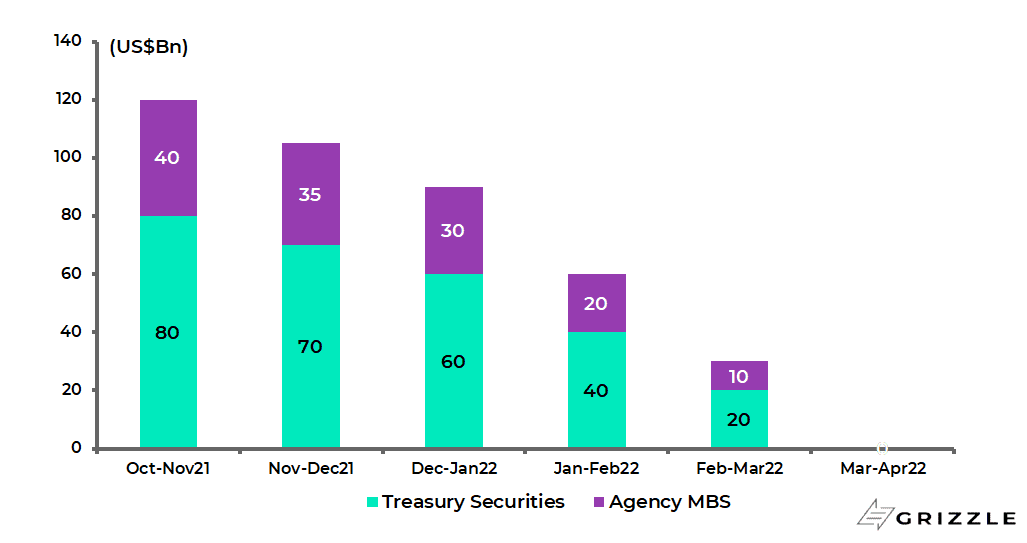

The above political pressure is one reason why the Fed has engaged in recent weeks in what has been labeled a “hawkish pivot”, as reflected in the widely anticipated decision taken at the December FOMC meeting to accelerate the end of tapering from June to March.

The Fed also decided to reduce the monthly pace of its net asset purchases by US$20bn for Treasury securities and US$10bn for agency MBS beginning January.

That means the Fed will increase its holdings of Treasuries and agency MBS by US$40bn and US$20bn this month.

Federal Reserve tapering plan: Monthly asset purchases

The other concrete result from the December meeting, aside from Powell’s more hawkish talk, is that most Fed governors now project three rate hikes this year whereas, as recently as last September, around half of them still thought there would be no rate hikes until 2023!

Meanwhile, the other point is that 7.0% is so far above the Fed’s formal 2% target that continuing talk of ‘transitory’ from the recently re-appointed Fed chairman Jerome Powell would have run the severe risk of degenerating into self-parody.

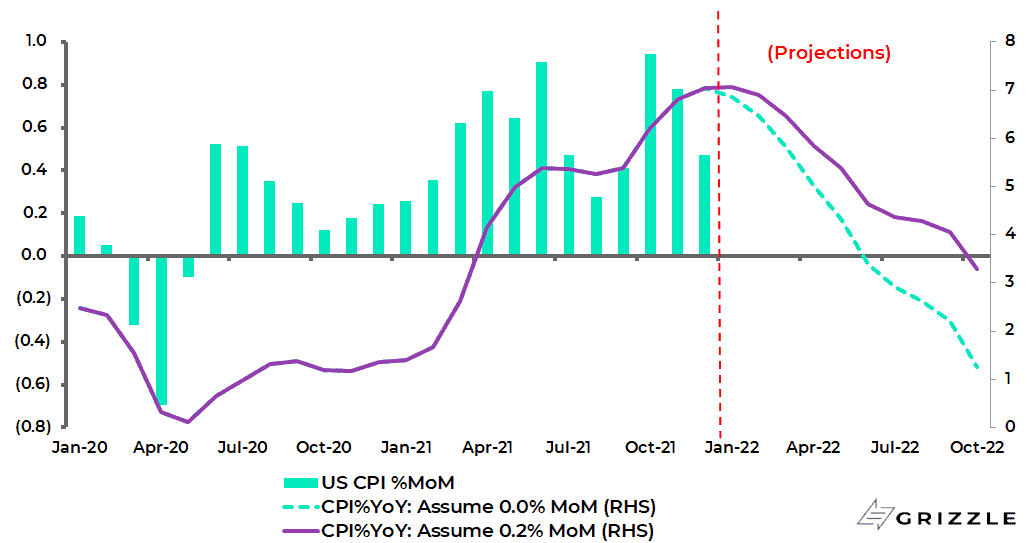

What about the inflation rate going forward?

These forward projections are in the context of the coming base effect which should kick in in the second quarter in the sense that CPI started to pick up in March 2021.

US CPI Inflation Projections

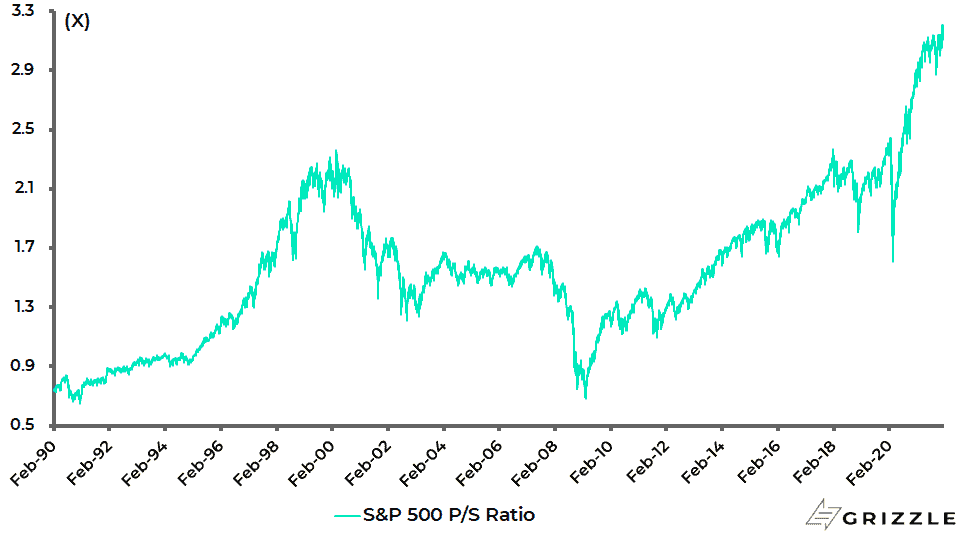

Meanwhile, the seemingly suddenly ‘hawkish’ Fed clearly poses obvious risks for stock markets, particularly the US stock market given the valuations, with the most vulnerable area the profitless tech thematic space as previously discussed HERE.

The S&P500 price to sales ratio is still at 3.12x, not far below the record high of 3.21x reached in late December.

S&P500 price to sales

Ultimately, this writer continues to have a hard time seeing the present Fed leadership ever becoming really hawkish.

But they are, unlike former Fed chairman Paul Volcker in the early 1980s, highly political in nature.

And the growing political pressure raises the risk that the Fed acts more hawkishly in the nearer term than previously expected.

That is, perhaps, until a major risk-off move causes them to move the other way.

Democrats Will Still Try to Pass Another Infrastructure Bill

Meanwhile, the failure of the Democrats to pass the bizarrely named ‘Build Back Better’ legislation late last year, due primarily to the resistance of one Democrat Senator Joe Manchin, does not mean that some alternative form of legislation will not be brought forward.

Still, it is unlikely to be quite as ambitious, or as costly, as Build Back Better which would have added as much as US$5tn of spending based on the Congressional Budget Office (CBO) estimate (see CBO report: “Budgetary Effects of Making Specified Policies in the Build Back Better Act Permanent”, 10 December 2021).

It was this CBO report which gave Machin significant political cover for his stance which so infuriated the progressives.

Unsurprisingly, that proposed legislation was criticized by Republicans not only for being un-American and socialist, in terms of its promotion of European-style welfarism, but also for fanning inflation.

One of the many controversial aspects of this bill was subsidies for electric vehicles, particularly those made by unionised labour in America.

Thus, the bill included a tax credit of up to US$12,500 for buyers of electric vehicles that are assembled in America by union labour.

Elon Musk Doesn’t Want Competitors to Have Access to EV Subsidies

In this context, this writer was interested to read the attached WSJ interview with Elon Musk last month (“Elon Musk on EV Subsidies, Corporate Titles and China: The Full Transcript”, 8 December 2021).

The Tesla boss advocated getting rid of all EV-related subsidies, including government support for the charging network which was another feature of the aborted bill.

Musk also made the point that the existing US$7,500 vehicle purchase tax credit for an EV was lobbied for by General Motors and not Tesla, and that all Tesla’s sales in 2020 and 2021 were no longer eligible for the tax credit because the company has already made so many electric cars.

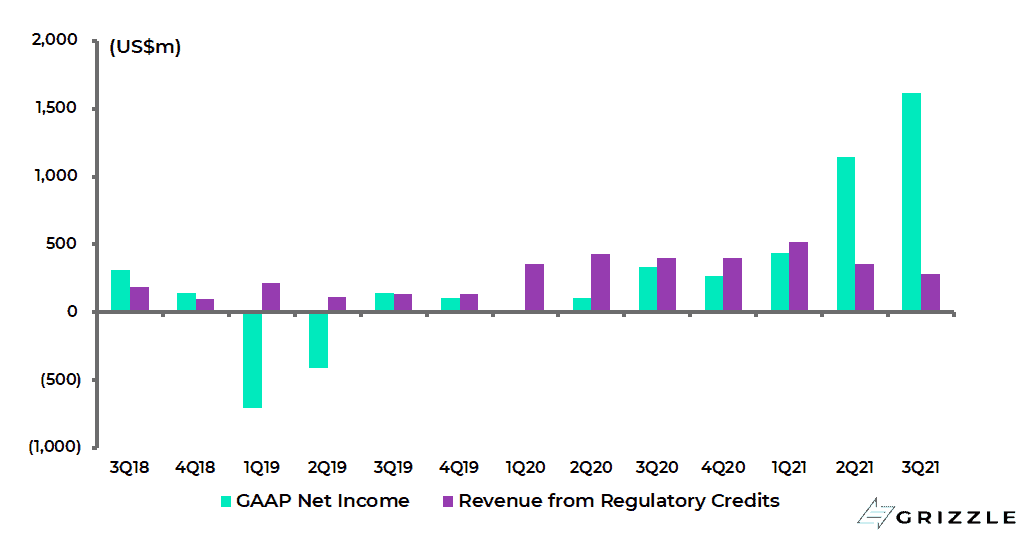

On this point, it is worth noting that Tesla has already made about two-thirds of all the electric cars made in America and sold around 900,000 cars last year.

While in the third quarter of 2021 it made US$1.6bn of GAAP net profits of which only US$279m came from the sale of “carbon credits”, the lowest since 4Q19.

The company’s next earnings report is due on 26 January.

Tesla GAAP net income and revenue from regulatory credits

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.