The interesting point about Bank of Japan governor Haruhiko Kuroda’s adjustment of yield curve control just before Christmas, jolting traders out of their pre-Christmas revelries, was why it happened when he had guided for the complete opposite.

The positive explanation is that he was taking advantage of the relative calm in fixed income markets, given the then-recent rally in Treasury bonds and correction in the US dollar, to commence the long overdue normalization of policy.

After all, in Japan it is not good to be the nail that is sticking out, and in the context of current G7 monetary policy, the BoJ governor’s stance has been looking ever more extreme.

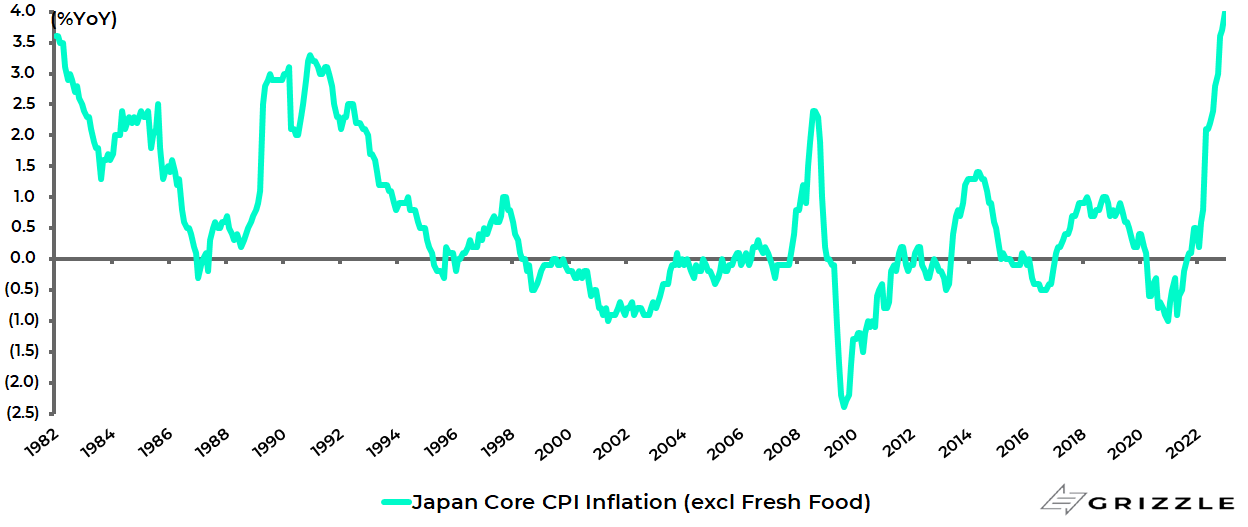

Japan core CPI inflation, excluding fresh food, rose to 4.0% YoY in December, the highest level since December 1981.

Japan core CPI inflation (excluding fresh food)

Still another explanation behind the timing of the move is that former BoJ deputy governor Hiroshi Nakaso, one of the two main candidates to replace Kuroda when he steps down in April, has apparently made it clear he would only take the job if there was a commitment to normalization of monetary policy.

Interestingly, a clue to Nakaso’s current thinking is provided by a speech he delivered at an online seminar hosted by the University of Tokyo and the IMF in November, when he argued that central banks must remove emergency support measures once financial crises are over to avoid moral hazard (see Reuters article: “Nakaso, a contender to lead BOJ, urges removal of emergency support”, 17 November 2022).

Probably both the above factors were behind the adjustment of policy.

The market reaction was initially quite orderly compared with if the action had been triggered by escalating market pressures in a context of surging Treasury bond yields and a surging US dollar, which was the growing threat when Japan engaged in its first foreign exchange intervention in 24 years to support the yen when the Japanese currency hit an intra-day low of 151.95 in October.

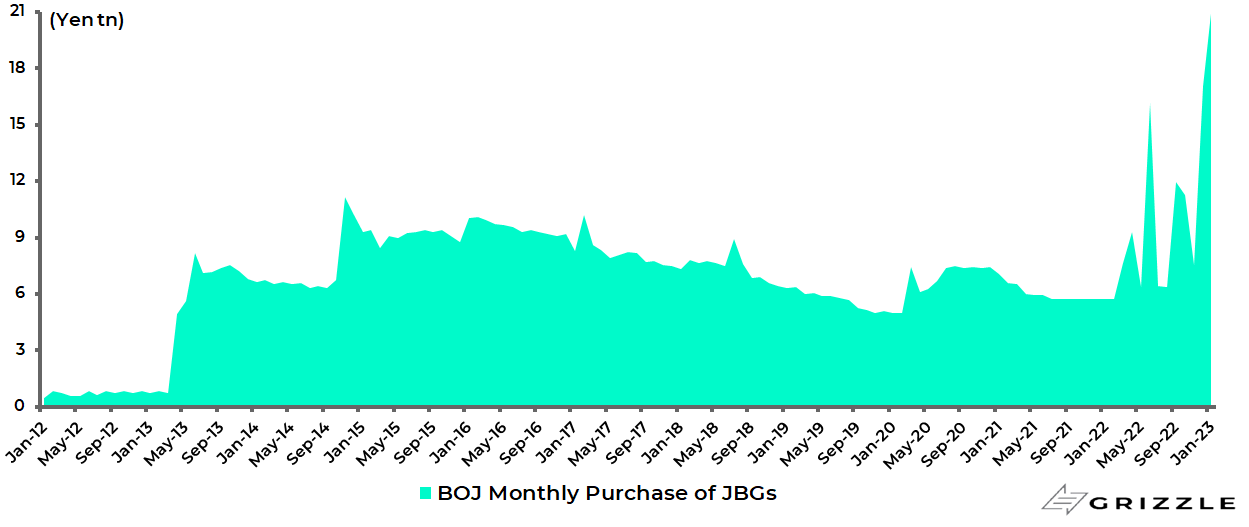

Still the pressure has been building up of late again with the Japanese central bank forced to do record buying of JGBs ahead of its policy meeting on 17-18 January.

The BoJ bought a record Y11.1tn in the week prior to the policy meeting and a monthly record Y20.9tn so far in January.

Bank of Japan monthly purchases of JGBs

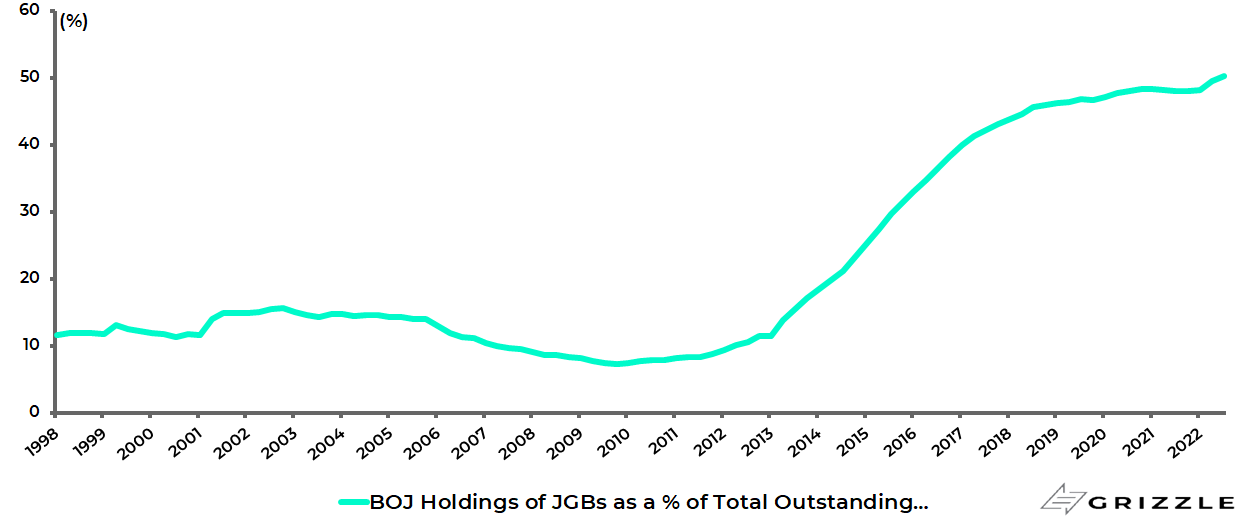

The pressure is certainly building.

The Bank of Japan’s total ownership of JGBs was 50.3% at the end of 3Q22 based on the flow of funds data, and it will have increased since, raising the spectre of outright monetisation.

When Kuroda arrived at the BoJ in March 2013 it was only 11.5%.

Bank of Japan ownership of JGBs

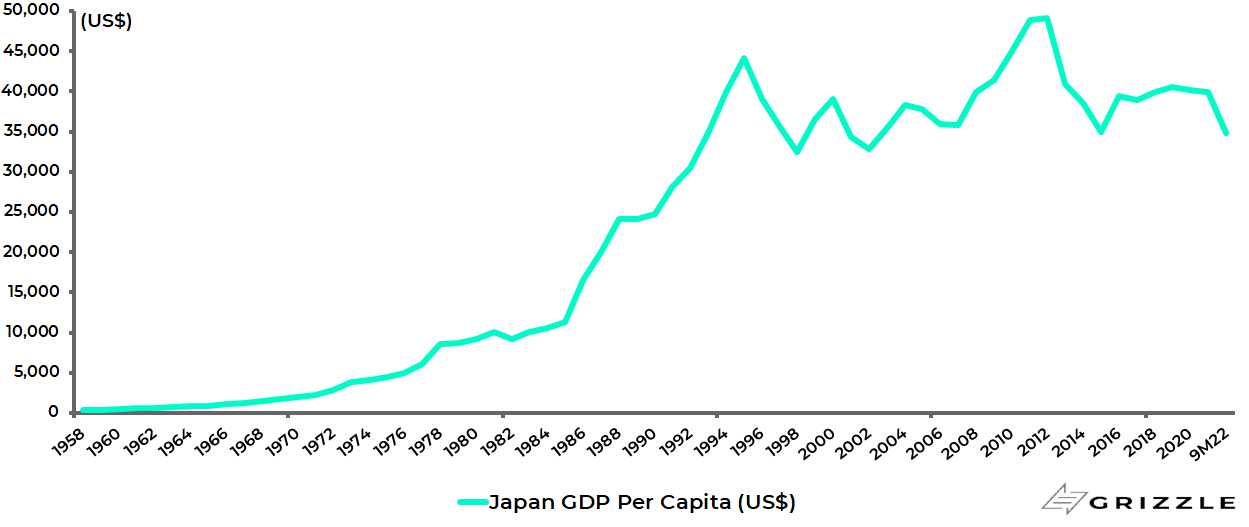

Japan GDP per capita was US$49,000 in 2012 before Kuroda took over and it is now US$35,000.

In this respect, Kuroda’s extreme policies have succeeded in impoverishing ordinary Japanese people.

Japan GDP per capita (US$)

Technically, of course, Kuroda is correct to say that YCC has only been adjusted.

The BoJ has, to be precise, raised in December the target yield on the 10-year JGB from 25bp to 50bp under its six-year-old yield curve control policy, thereby allowing up to a 50bp move above or below 0%.

It had been at 25bp since March 2021.

The move came after the central bank in October raised its inflation forecast for this fiscal year ending 31 March from 2.3% to 2.9%. This would be the highest annual inflation rate since FY89.

The BoJ again raised its inflation forecast for this fiscal year to 3.0% this month.

Yen Rebound Depends on an End to Negative Interest Rates

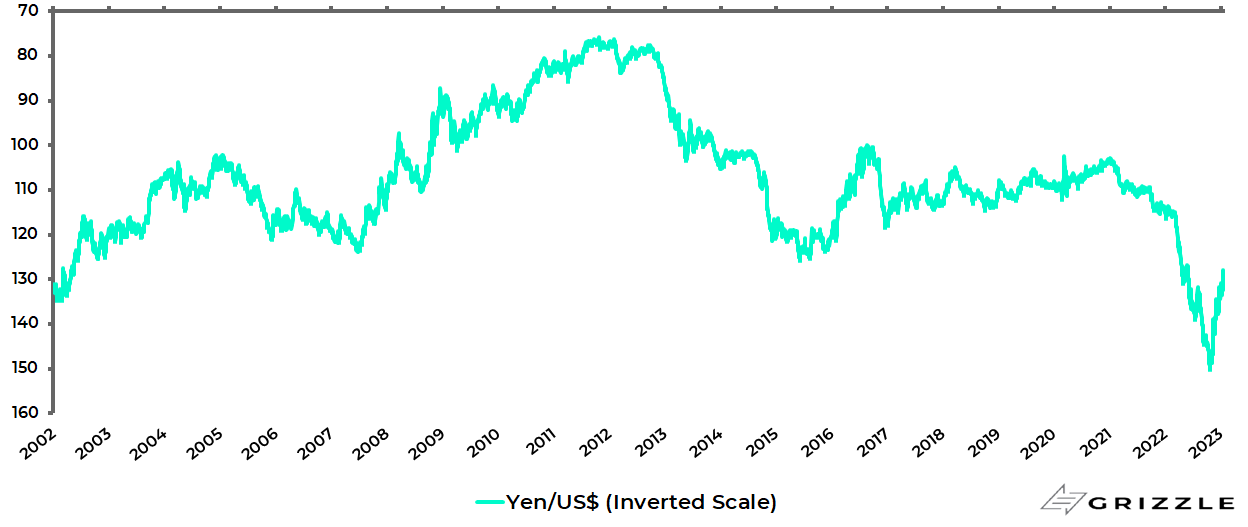

Meanwhile, it is also worth noting that the Japanese government added to the inflationary pressures by announcing in late October a Y29.1tn fiscal stimulus, a package which includes subsidising energy and gas bills to mitigate the damage from the imported inflation triggered by Kuroda’s monetary policy, with the yen at its worst point in October down by 32.5% against the US dollar since January 2021.

The yen has since rebounded by 16.7% as markets anticipate more of a de-anchoring of bond yields by Kuroda’s successor if no further pre-emptive action is taken prior to his departure.

It is also expected that whoever succeeds Kuroda will quickly end negative rates. The deposit facility rate is minus 0.1%.

Yen/US$ (inverted scale)

The Move from Japanese Bonds to Stocks Could Finally be Upon Us

From a stock market standpoint, all of the above makes it ever more likely that Japan is exiting a deflationary era, which means that, sooner rather than later, domestic institutions should, in theory at least, start to think about reallocating out of yen fixed income into Japanese equities.

This is something they have not done since the Bubble burst in 1990.

If the case for allocating out of yen fixed income into equities seems overwhelming, no one can be sure that institutional Japan will embark on such a change until there is concrete evidence that it is actually happening given institutional inertia, the longstanding entrenchment of the deflationary mindset and an absurd, albeit doubtless lingering, obsession with vol-adjusted returns.

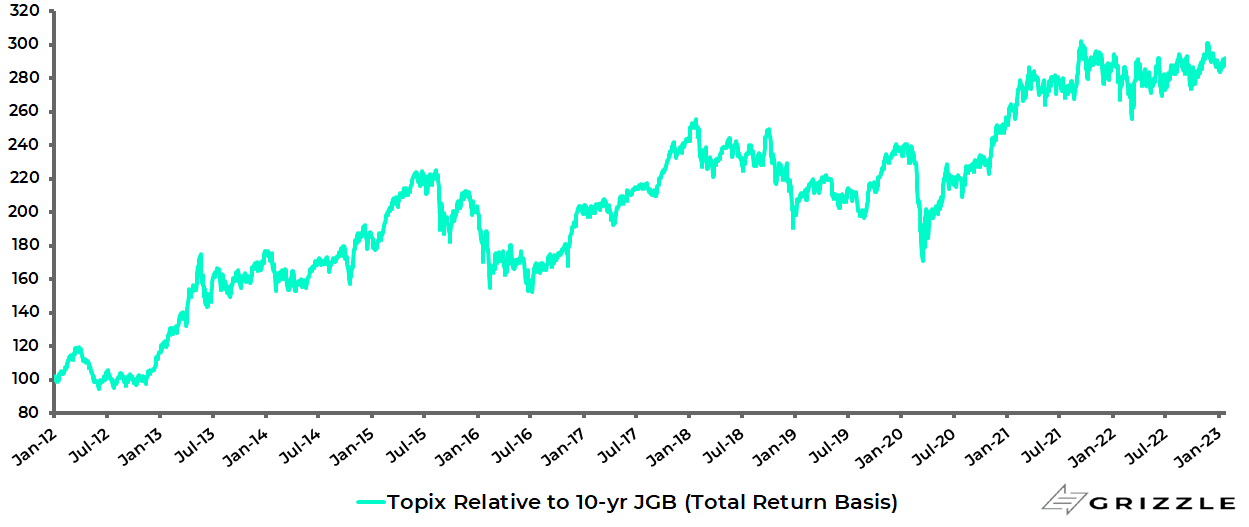

As discussed here previously (The yen is on the ropes, is yield curve control next?, 7 August 2022), an allocation from fixed income to equities should long since have happened in the sense that the Topix has already outperformed the 10-year JGB by 199% on a total-return basis since November 2012 prior to the launch of Abenomics.

Topix relative to 10-year JGB (total-return basis)

Wages Will Signal Inflation Is no Longer Transitory

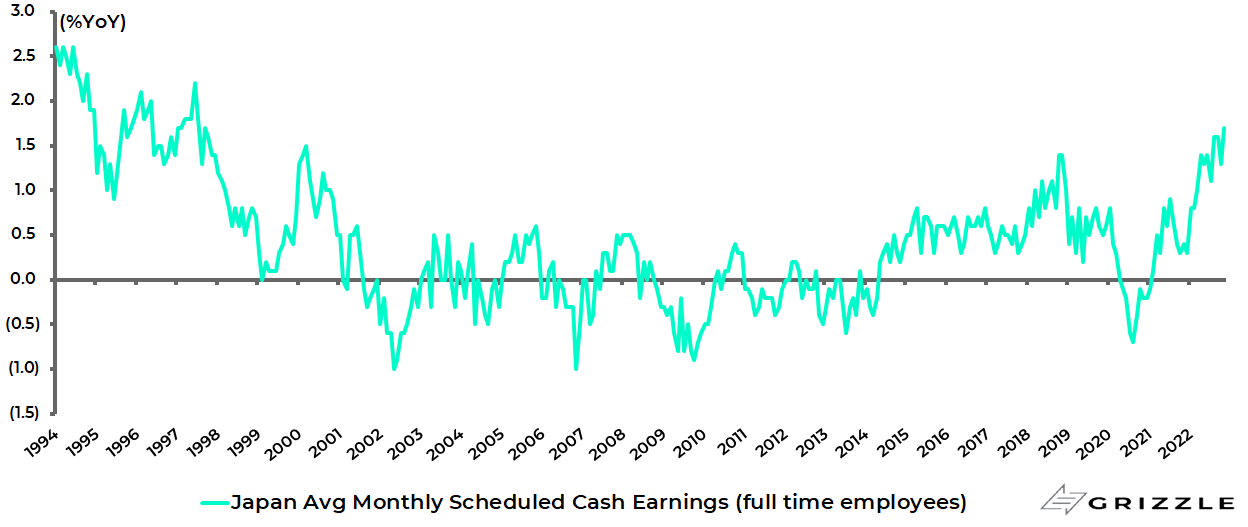

Meanwhile, Japanese nominal wage data should be watched closely for any evidence that inflationary pressures are not just imported, which has been the Kuroda argument for not adjusting policy further.

On this point, average monthly scheduled cash earnings of full-time salaried employee, the most lagging indicator, rose by only 1.7% YoY in November.

Japan average monthly scheduled cash earnings growth for full-time employees

Still the Japanese Trade Union Confederation (Rengo), representing about 7m workers, is seeking an overall pay rise of 5% in the coming spring wage negotiations (shunto), the biggest increase in 28 years since 1995.

This includes a 3% increase in base pay and a seniority-linked increase of roughly 2%.

A de-anchoring of Yields Could Threaten the Government Budget

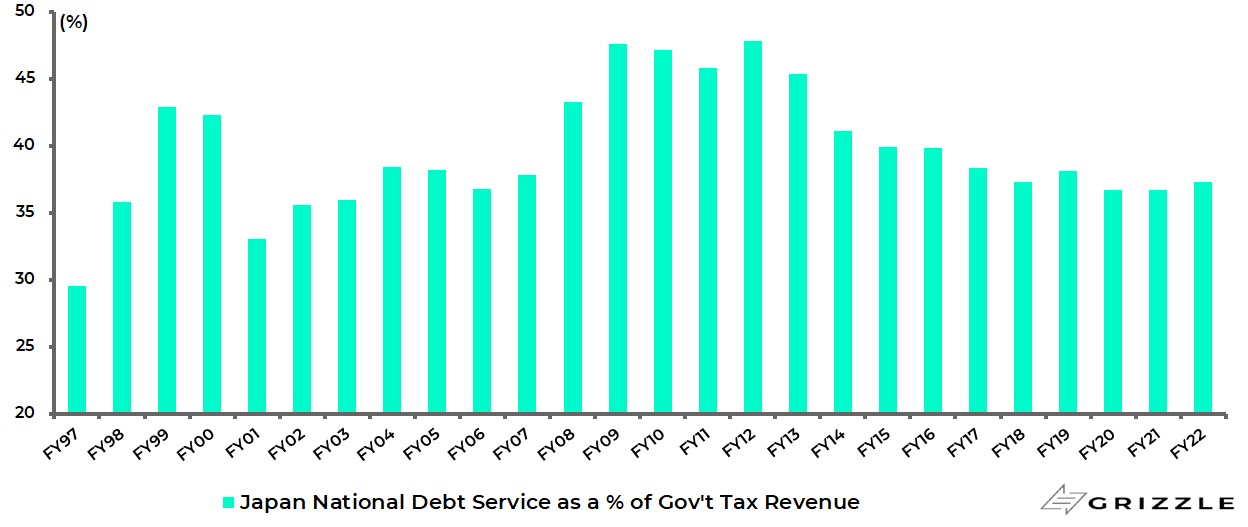

Meanwhile, if Kuroda’s stated reluctance to adjust yield curve control has been because of a lack of evidence of a pickup in nominal wage growth, there is also the unstated concern about how a de-anchoring of bond yields could increase, dramatically, the cost of servicing Japan’s massive government debt.

On the fiscal issue, Japan’s government debt totaled a gross 262% of GDP at the end of 2021, though the net number is a less scary 168%.

In this respect, the cost of servicing government debt has remained under control in recent years only because of ultra-low bond yields.

National debt service payments, as a percentage of tax revenues, have declined from 47.8% in FY12 to 36.7% in FY21 ended 31 March 2022.

Yet, as already noted, this has been at the cost of growing BoJ ownership of JGBs, thereby threatening central bank credibility.

Japan national debt service as % of government tax revenue

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.