Bottom Line

Tilray (NASDAQ: TLRY) delivered good progress in the quarter doubling both revenue and production over the last year.

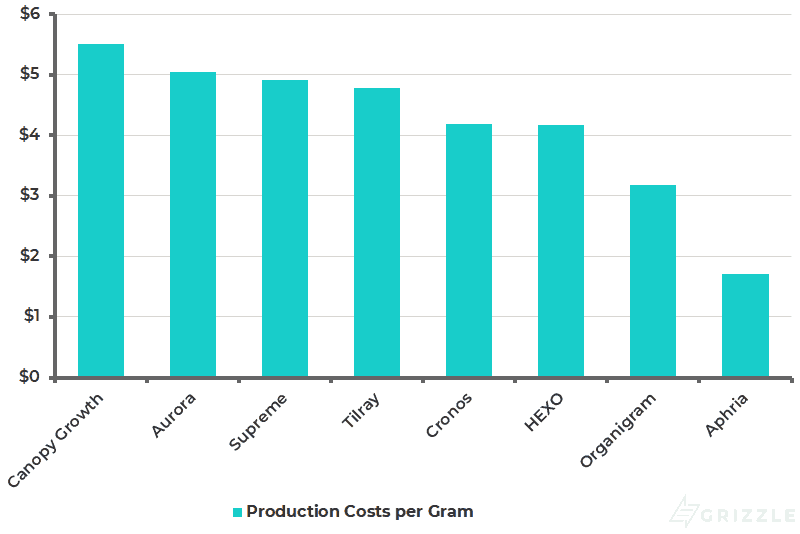

However, the selling price per gram barely budged in the last year and production costs are now $4.78 per gram compared to $3.86 12 months ago.

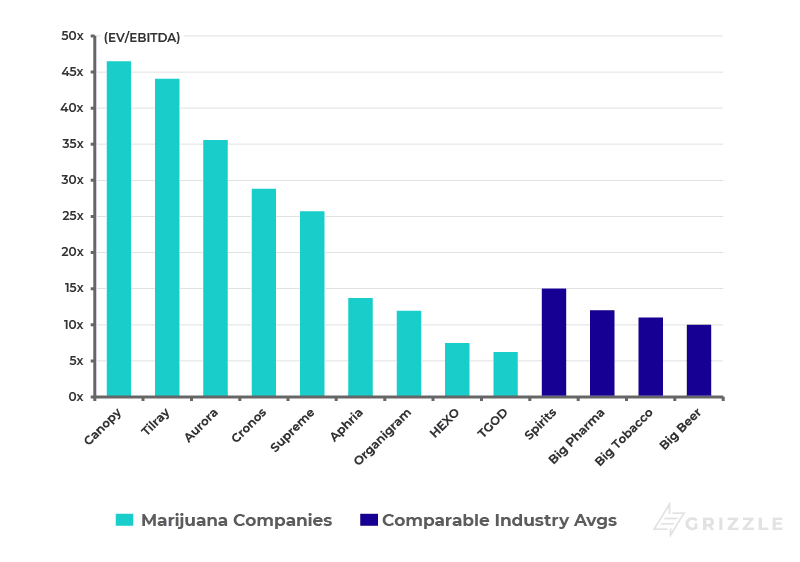

With today’s pop in the share price, Tilray is fully valued and we would recommend investors rotate into much cheaper stocks with lower cost structures such as Aphria (APH), our top pick among the large cap cannabis companies.

Aphria trades at only 14x 2020 EBITDA compared to Tilray at 45x and has production costs below $2.00 per gram compared to $4.78 per gram for Tilray.

Is Tilray a Top Target for Beer and Liquor Companies?

Acquisition rumours are swirling around the cannabis industry after Constellation’s recent investment in Canopy and many of the stocks embed significant deal expectations.

So what do beer, soda, liquor, or wine companies look for in a licensed cannabis producer?

We think it comes down to product pipeline, branding, and customer insight, in that order.

Product Pipelines

Beverage companies are looking for a producer actively developing new cannabis-infused products and one that is looking ahead, trying to anticipate what product consumers want next.

Tilray is spending over $3 million a year on R&D making it likely they have a deep portfolio of potential cannabis products such as edibles and infused drinks for when those products are legalized in Canada next year.

Brand

Branding is an area where beverage companies are at a disadvantage.

Cannabis users are already familiar with many of the leading medical suppliers, giving those LPs a branding advantage.

Producers are also feverishly introducing new retail brands so by the time beverage companies create their own, the market will already be a very crowded place.

Tilray is well positioned for recreational sales with at least eight retail brands ready to go on October 17.

Customer Insight

Licensed producers understand the cannabis customer better than anyone.

Through operations, community outreach, and market research, they have a trove of data that could prove invaluable when selling to such a dynamic and fast-growing market.

The majority owner of Tilray, Privateer Holdings, also owns Leafly, an online data hub for all things cannabis.

An investor in Tilray would likely be able to access many of the insights gained from the trove of data found on Leafly.

Tilray’s patient records combined with Leafly’s big data would present a compelling investment opportunity for a beverage giant looking to better understand the cannabis market’s potential.

What About Growing Capacity?

Notice we didn’t mention production capacity or growing expertise.

In the future, we think drinkable cannabis products will use synthetic cannabinoids to maintain consistency and to enhance shelf life, making the need for high-quality cultivated cannabis obsolete.

Even if beverage companies want their own in-house supply, they have the resources to easily staff up and build their own growing operations at a fraction of the cost of buying stock in an expensive publicly traded producer.

They could also buy a cultivation license through the purchase of a small LP instead of paying a premium for the stock of larger producers.

Production capacity alone does not signal an attractive investment target for the Diageos of the world.

Price Could be A Sticking Point

Overall, Tilray is a very attractive target for any large beverage company looking to enter the cannabis market.

The largest sticking point to a deal happening is Tilray’s premium price.

Tilray trades close to Canopy Growth multiples, so an acquirer has to believe they can squeeze over $2 billion of revenue from Tilray’s assets compared to $6 million of revenue today.

Tilray Production Costs Are Above Average

Tilray had production costs per gram of $4.78 in the three months ending June 30, 2018, 14% higher than the industry average.

Production costs increased 25% in the last year as the company staffs up and builds facilities and distribution infrastructure to be ready for recreational sales on October 17.

Tilray is well positioned to distribute cannabis grown in Canada and Portugal throughout Europe, but it will have to bring down production costs meaningfully to compete against the largest Canadian producers longer term.

Industry Production Costs per Gram

Research and Development Spending Sets Tilray Apart

Developing new and exciting cannabis product and delivery methods is the only sure way to generate higher profits.

A higher spending commitment to research activities is likely to lead to the invention of more high value cannabis products in both the medical and recreational market.

Looking at the R&D budgets of the largest licensed producers we can see Tilray leads the pack.

The company is spending over 10% of revenue on R&D compared to less than 3% for other producers.

Tilray is participating in four different clinical research studies which could set them up well to one day own patents on widely sold cannabis medicines.

R&D spending should pay dividends for Tilray in the long-term and sets them apart from competitors.

Tilray defines R&D as follows

Industry R&D Spending and as a % of Revenue

Solid Market Positioning is Reflected in a Premium Stock Price

Tilray was a first mover in establishing a growing and sales presence outside of Canada and the market has rewarded this first mover advantage with a premium stock price.

With the stock increase after earnings today, Tilray is now the most expensive Canadian licensed producer based on expected 2020 EBITDA (Earnings Before Interest, Taxes and Depreciation).

Tilray will have 25% of the growing capacity of Canopy longer term and has an in-country footprint in far less regions than Canopy.

Investors believe the quality of management and dealmaking ability internationally makes up for the difference in production capacity and international footprint.

Only time will tell.

2020 Enterprise Value to EBITDA for Largest Licensed Producers (8/28/2018)

Remember to Invest Like You Own the Assets

Investors should look at marijuana companies as if they are part owners of each company’s growing capacity.

When you think this way it will help you put each companies stock price into perspective.

Take Canopy Growth for example.

As an investor if you pay $57 to buy some Canopy stock you will technically own 1 gram of production when all planned greenhouses are fully built out.

You are expecting Canopy to take that gram and sell it for a profit which you are entitled to.

The problem is that Canopy currently loses $18 for every gram they grow and even if they can generate a 26% net income margin, in line with giant tobacco conglomerates, your 1 gram will generate $2.34 a year for your $57 payment, a payback period of 25 years and a negative present value.

This is why valuation is so important.

Any marijuana company can be a good investment if the price is low enough, but many marijuana valuations are looking rich compared to future legal market reality.

Cost to Own One Gram of Future Growing Capacity

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.