Bottom Line

This is likely a quarter Tilray’s management wants to forget.

Revenue of C$20.9 million missed even the low end of revenue estimates and the net loss of $0.33/sh was also below expectations.

On one hand, management has shown they can sign interesting partnerships with some of the largest consumer packaged goods companies in the world.

But on the other hand, financial results have not yet proven this is a management team that knows how to efficiently grow and sell cannabis.

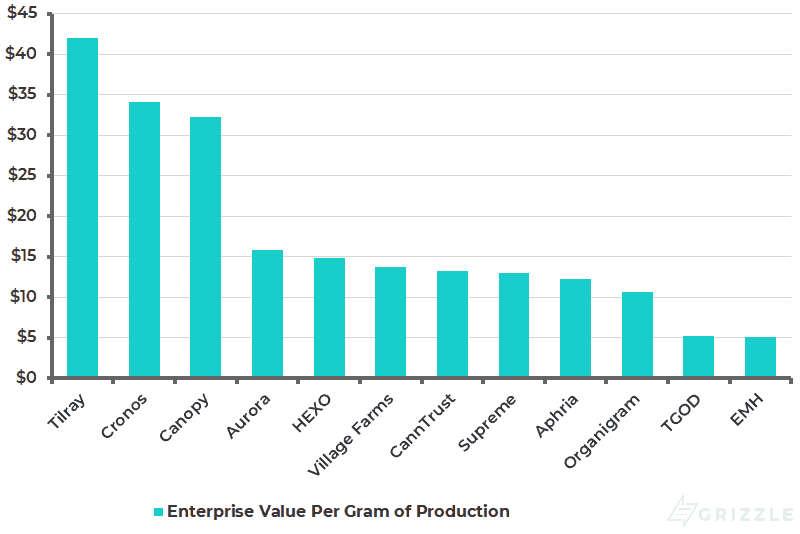

Tilray trades at a price far above the revenue greenhouses alone will generate, telling us the market expects the management team will find other large sources of revenue in the future.

Enterprise Value per Gram at Fully Funded Capacity

The problem for us investors is that we still don’t have details about where this revenue will come from and how large it can be.

Tilray’s revenue and profitability outlook are even more uncertain than similarly priced peers Canopy, Aurora and Cronos.

Tilray has the third largest market cap in cannabis, but is not even a top four producer in Canada and unlike peers, does not have ownership of its own brands which are mostly licensed through third parties.

Tilray’s stock has the farthest to fall should there be hiccups in the expansion of legal cannabis, causing us to recommend investors with a longer time horizon rotate into U.S. operators who trade at one third the multiple of Canadian growers (IAN, SOL, TRUL, HARV,CURA, ACRG.U)

Staying in Canada we prefer producers trading at a discount (OGI, FIRE, TRST, APHA) to guard against disappointing industry cannabis sales in 2019.

Operational Review

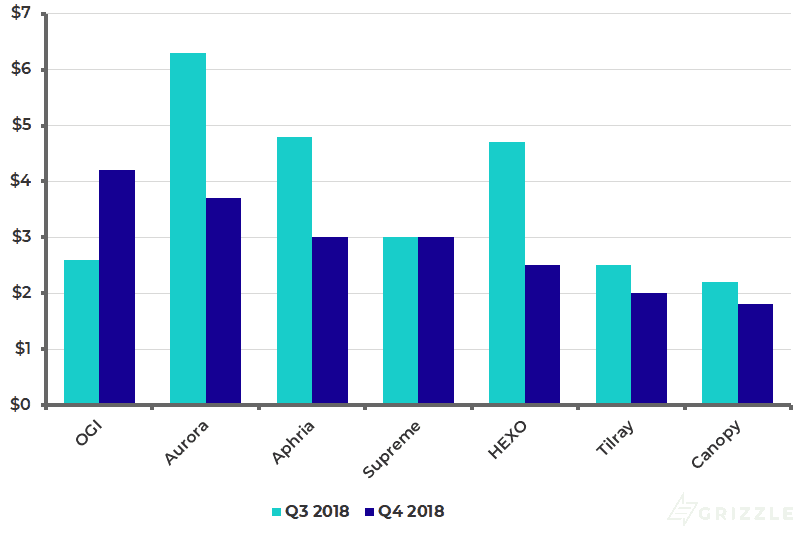

Tilray sold 2,053 kg in the first full quarter of recreational sales. This is up 27% from the prior quarter, much slower growth than peers who saw volumes increase an average of 230% in the first full quarter of recreational sales.

We also estimate revenue growth was anemic, up only 16% when other producers were doubling or tripling revenue.

QoQ Revenue Growth in First Quarter of Recreational Sales

We also estimate revenue per gram fell 9%, but with the company refusing to break out excise tax we won’t be totally sure about results until more detailed financials are released.

The fall in per gram revenue and gross margins will continue at least for another quarter as the company continues to buy additional wholesale product from other licensed producers to meet demand.

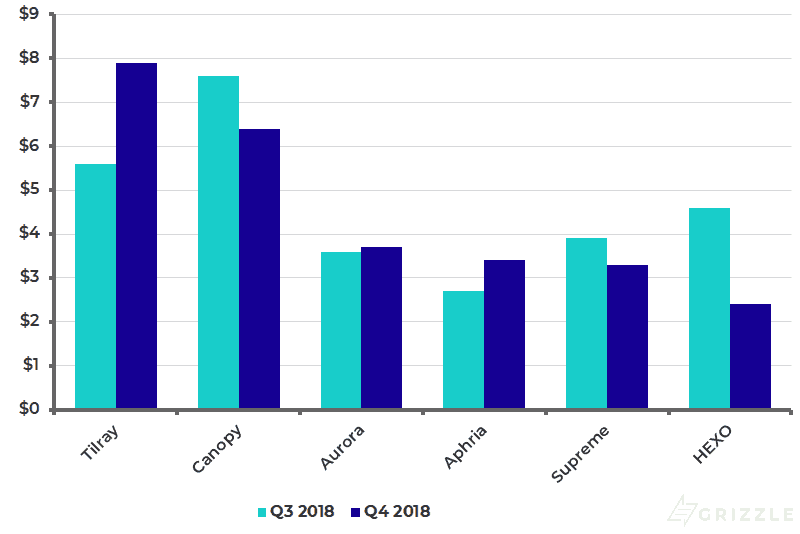

Moving on to Tilray’s profitability, this is a company with the second lowest margins in the peer group, after Canopy, and is 35% below the group average of $3.04/gram.

Gross margins of 20% are the lowest in the industry because Tilray is having to buy supply on the wholesale market to satisfy customer demand.

Gross Margin Per Gram Over Last 6 Months

Production costs this quarter were about $7.90/gram, 125% above the peer average. Costs per gram will definitely fall as volumes harvested increase and Tilray stops buying supply in the wholesale market, but Tilray still has a lot of work to do.

Production Costs Per Gram for Producers with Recreational Sales

Valuation is in the Clouds

The best way to illustrate the world investors think Tilray will live in 3 years from now is with two examples.

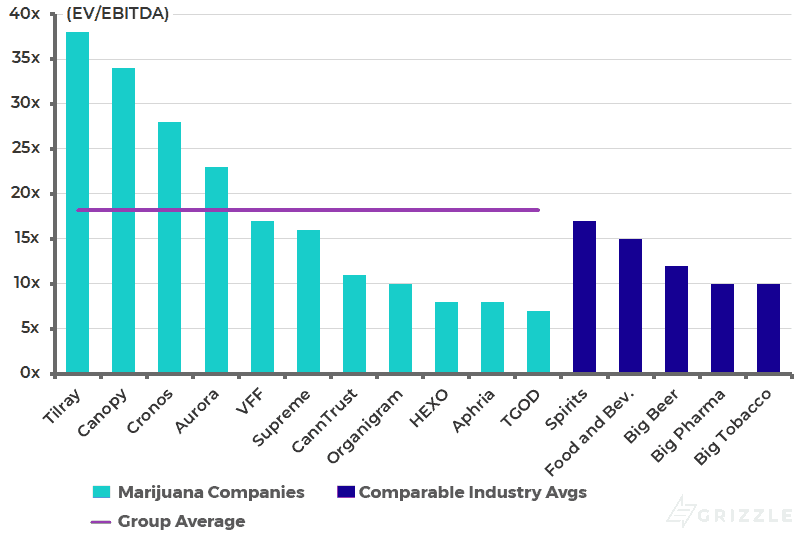

If Tilray sells cannabis for this quarter’s selling price of $7.36/gram, the company will have to sell 260,000 kg a year at a 30% EBITDA margin to justify the current market cap.

260,000 is 25% more than Tilray’s ultimate funded capacity will be, again demonstrating the significant premium built into the stock.

Put another way, when Tilray reaches funded capacity of 209,000 kg they will have to sell each gram for $7.50 per gram to justify their $8.8 billion market cap.

Recreational revenue is only $4.40/gram today.

EV/EBITDA in 2020

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.