Legal cannabis producer Tilray (NASDAQ: TLRY) reported disappointing results and the stock is down 10% as of 4:40 EST in after-hours trading.

Revenue came in at $43 million, 23% worse than consensus of $56 million.

The miss was driven by international sales down 30% and wholesale sales down 60%.

Moving down the income statement, Tilray generated an EBITDA loss of $50 million which was more than double what analysts were expecting and far higher than last quarter’s loss of $24 million.

Losses are going in the wrong direction.

The earnings per share loss of $0.62 missed consensus of a $0.38 loss by a whopping 60%.

Looking at operational performance, Tilray sold 40% more cannabis quarter over quarter, down from last quarter’s volume growth of 94%.

Tilray has a 7% market share in Canada, its most important market.

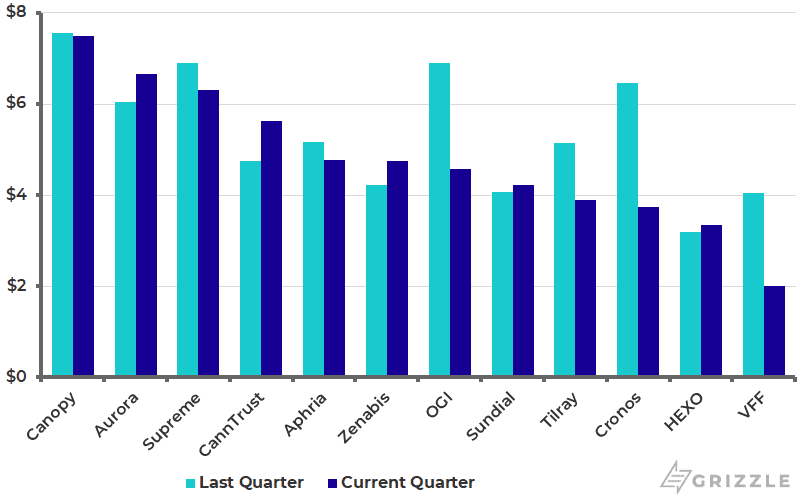

Revenue per gram was up 6% this quarter to C$4.16/gram compared to C$3.90 per gram last quarter telling us cannabis 2.0 products sold at a better margin came into play.

Tilray sold cannabis for C$9.80 per gram only one year ago, showing us how quickly prices have fallen.

Revenue Per Gram

Cannabis prices have been falling all year and will continue to fall based on our research until supply and demand are more in balance.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Tilray has only four months of cash left at the current spending rate and still has to triple revenue to break even which will be extremely challenging in the Canadian market. Until the company is close to making ends meet we think the stock will struggle as management issues more shares or dilutive debt to keep the lights on. [/su_panel]Investors don’t need to worry about missing the eventual rebound in Tilray and others.

Though you may miss the first 10%-20% of the rebound, the seriousness of the challenges ahead mean by staying out of this stock and investing elsewhere you will both avoid any future downside and avoid a missed opportunity if the stock goes nowhere, as we think it will.

Tilray will likely increase the shares count from here, making it difficult for the stock to rebound over the next 6-12 months.

What Should Investors Expect Over the Next 6 Months

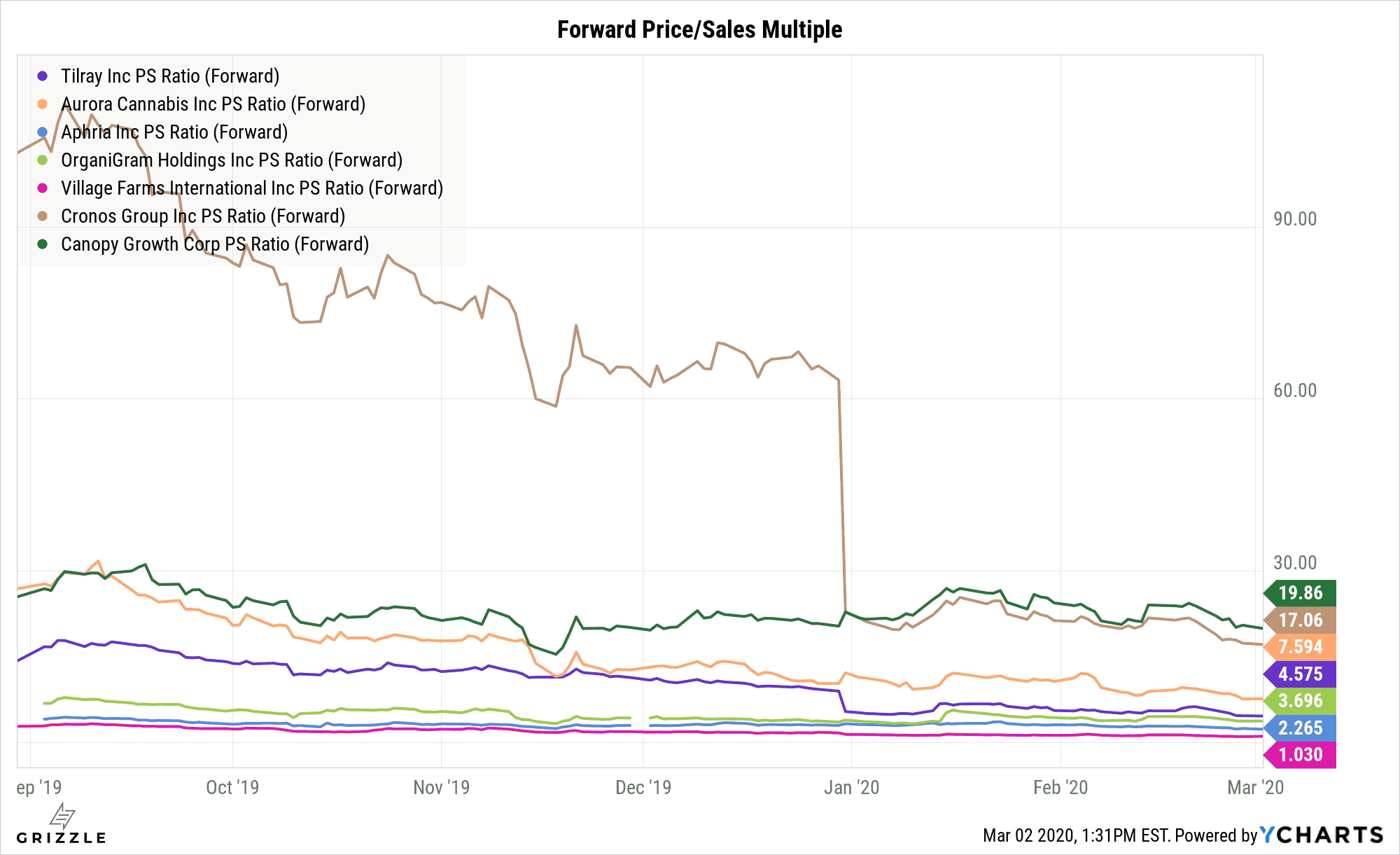

Even at ~$14.20/sh Tilray is the fourth most expensive Canadian LP, behind only Canopy, Cronos, and Aurora.

Tilray is one of the top three best-positioned producers in Europe, but that market is still puny, though growing quickly.

Management still has to rely on Canada to make ends meet, which will be difficult with increasing competition and regulatory hurdles that are keeping the legal market from quickly displacing the black market.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Tilray remains expensive compared to larger peers with either more market share in Canada or much better cash situations. We think the stock will struggle until management is on firmer financial footing and does not need to issue any more convertible debt or stock to pay for money-losing operations. [/su_panel]Forward P/S for Canadian LPs

Disclosure: The writer does not hold any positions in TLRY stock.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.