Grizzle had the pleasure of sitting down with David Smith, Chief Financial Officer of Agnico Eagle Mines (NYSE: AEM, TSE: AEM).

Agnico is one of the best run gold mining companies in the world and has delivered superior shareholder return versus their peers and the gold price for nearly 25 years.

In our interview Smith provides excellent insights on the challenges and opportunities in the gold mining industry and how Agnico is well positioned to capitalize.

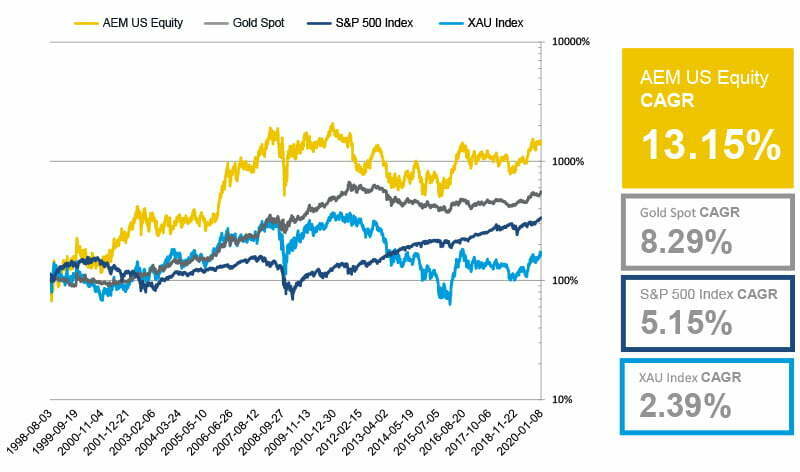

Agnico Eagle vs The Rest: 1998 to Present

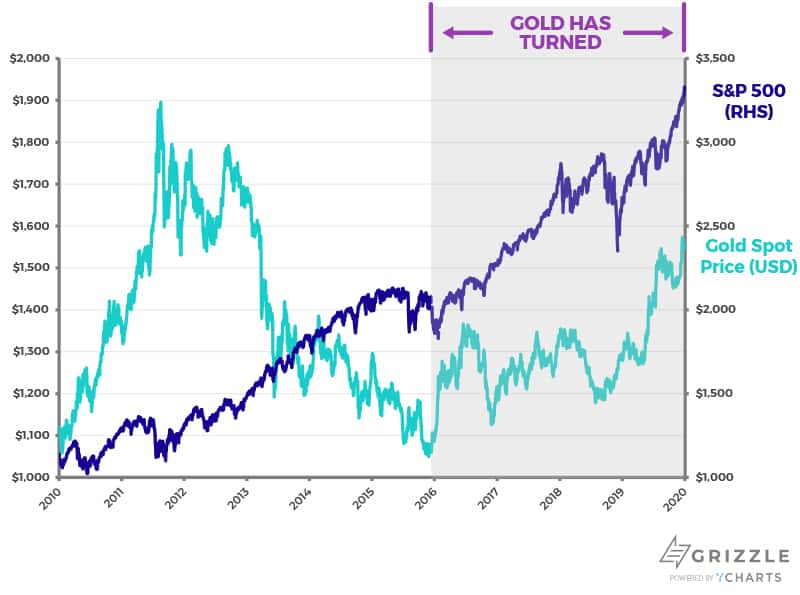

The recent turn in the gold price has provided an important tailwind for growth in cash flow for the industry. The strong gold price presents the opportunity for the industry to deliver on its self-imposed mantra of “profitability over ounces”.

Gold vs. S&P 500

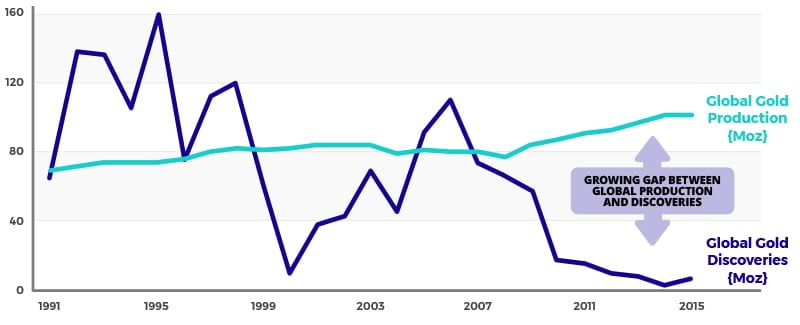

One of the structural challenges in the gold mining industry is the lack of exploration discoveries over the last 2 decades.

There is a structural gap between current gold production and gold discoveries. This ”discovery deficit’ will disproportionately benefit companies that have successfully invested in exploration over the last 20 years — Agnico Eagle has been the most successful senior gold mining company to harvest value from the drill bit.

Global Gold Production vs Discoveries

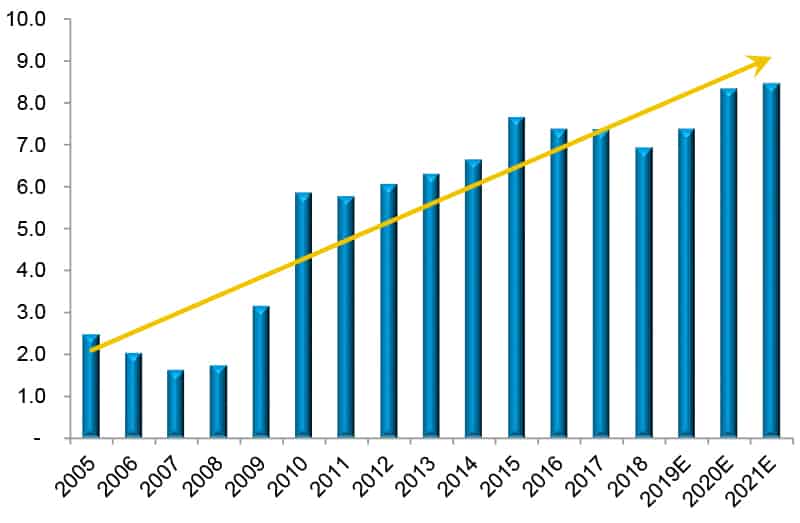

Smith outlines Agnico’s winning gold mining framework: delivering value per share.

Agnico has grown production per share by 8% annually over the last 15 years — no other large cap gold company has even come close to this level of operational execution, in fact nearly all senior gold companies have seen gold production per share fall over the same period.

Production per 1000 Shares: 8% CAGR from 2005 to 2021E

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.