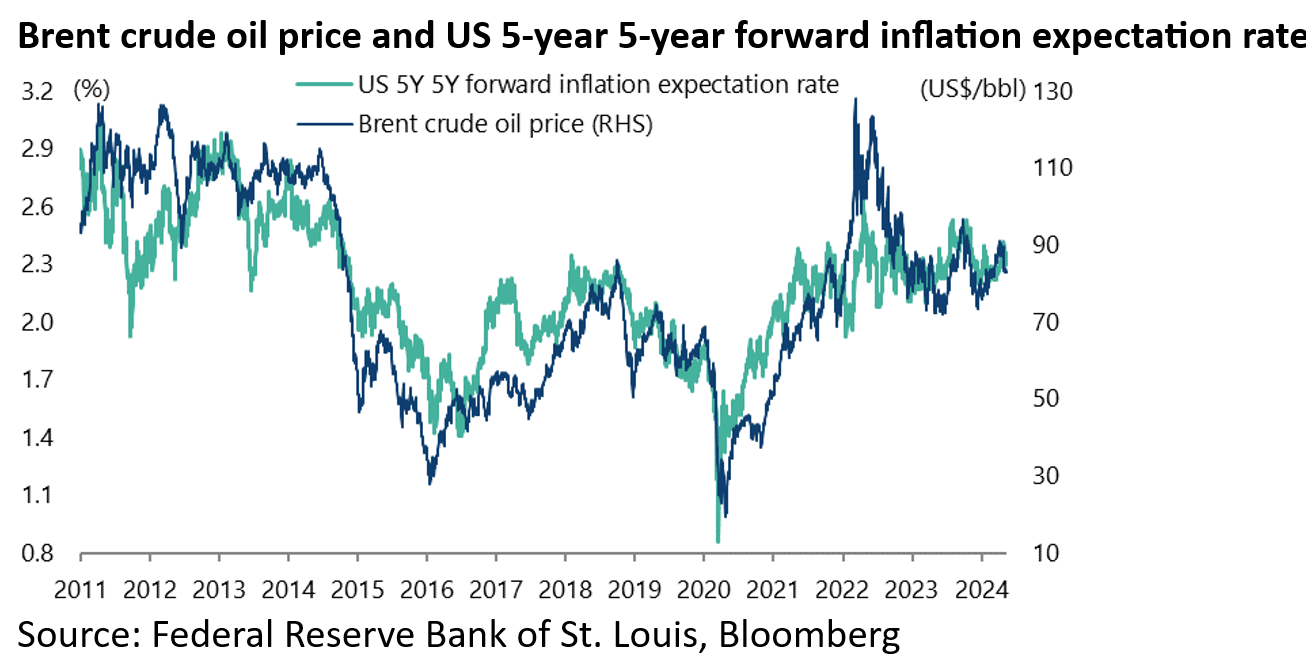

It remains the case that the last thing the Biden administration and the Federal Reserve want to see is a further rally in the oil price.

One, among several reasons for this, is the longstanding correlation between the Brent crude oil price and US five-year five-year forward inflation expectations, which for now remain well anchored at 2.34%.

The correlation between the two since 2011 is 0.88.

The oil price has begun to appreciate again since the International Energy Agency (IEA) in March increased its demand forecast and reduced its supply forecast.

Oil demand growth in 2024 was revised up by 110,000 b/d from 1.2m b/d in February to 1.3m b/d, while 2024 supply growth forecast was reduced from 1.7m b/d in February to 800,000 b/d.

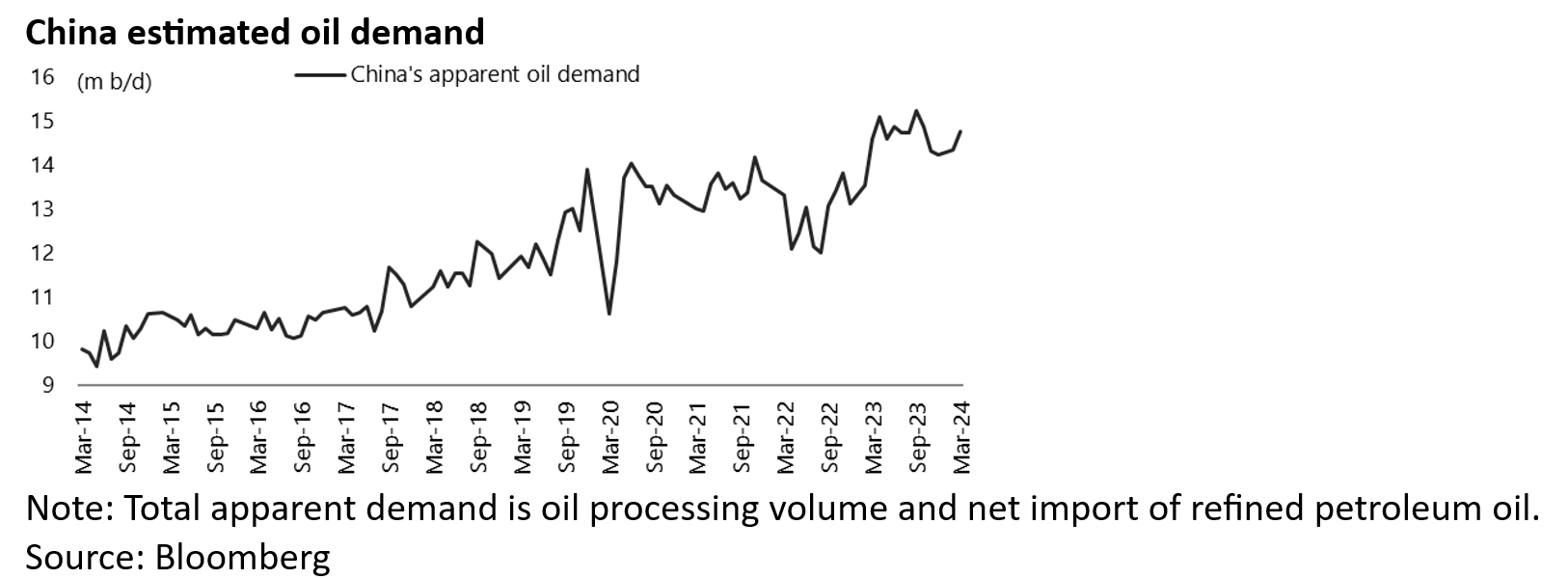

Meanwhile, the latest data on China oil demand shows a further increase reflecting the pattern prevailing last year whereby China seemed to be increasing its reserves of oil even as the US was doing the exact opposite, namely draining oil from its Strategic Petroleum Reserve at least until early July.

Since then there has only been a marginal pickup.

Thus, China’s estimated oil demand increased by 4.2% YoY to 14.48m b/d in January-March, according to data compiled by Bloomberg.

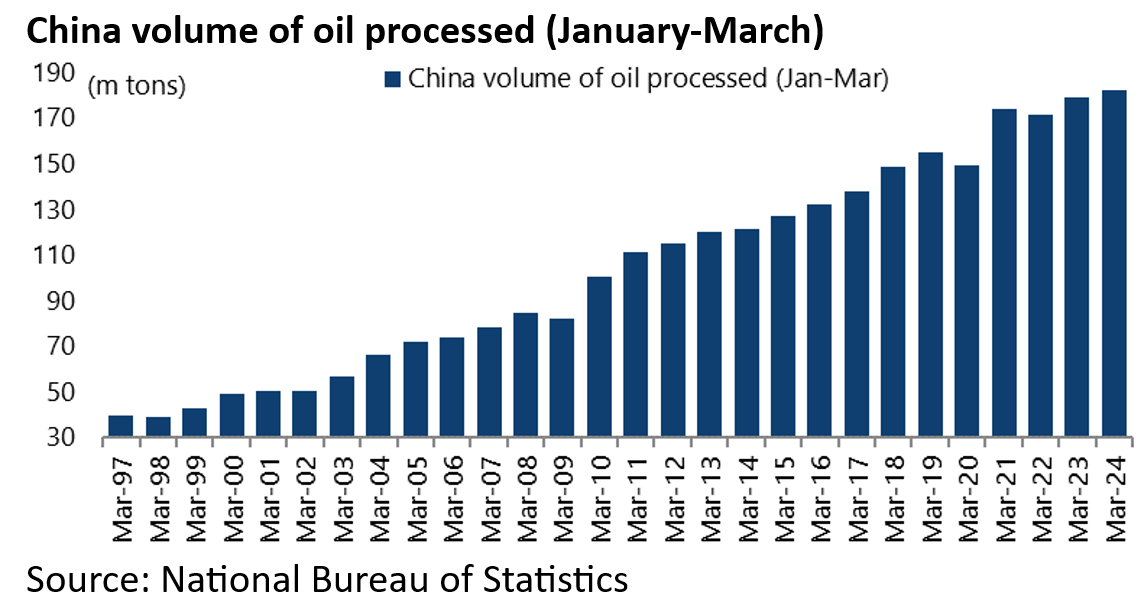

While the official data shows that the volume of oil processed in January-March rose by 2.4% YoY to a record 182.5m tons.

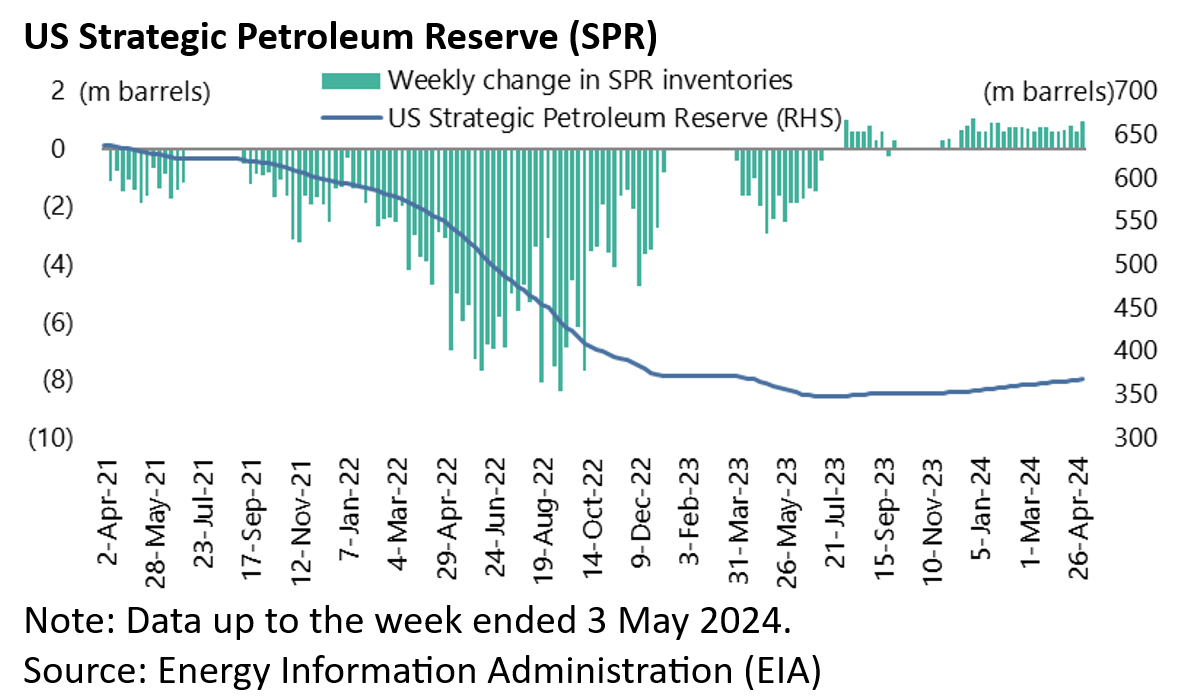

Meanwhile, the US Strategic Petroleum Reserve (SPR) declined by 25.62m barrels in the first half of last year to a low of 346.76m barrels on 7 July, after declining by 221.3m barrels in 2022.

Since then it has risen by only 20.46m barrels to 367.22m barrels as of 3 May.

Has US Shale Growth Finally Peaked?

But perhaps the most significant issue as regards supply, assuming OPEC Plus can maintain its discipline, is what happens to US shale production.

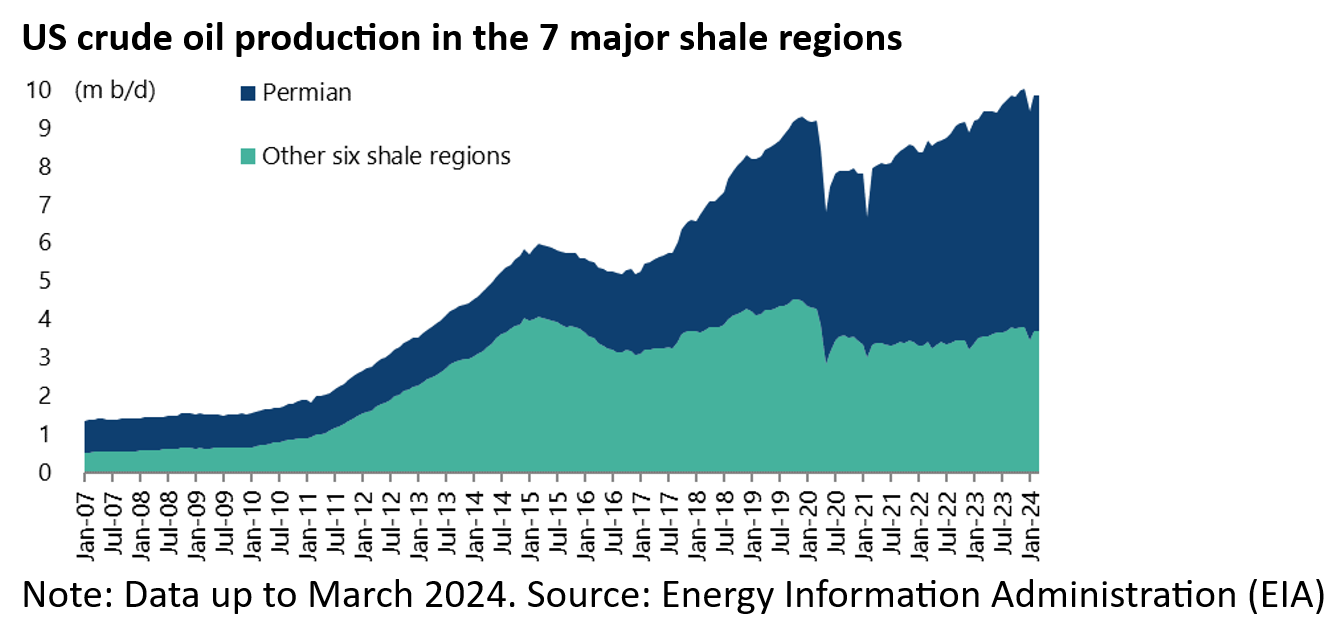

In that respect, all the major US shale regions look to have peaked in terms of shale production except the Permian region.

Total crude oil production in the six shale regions outside the Permian, at 3.69m b/d in March, remains 19% below their peak of 4.54m b/d reached in October 2019.

While production in the Permian region, at 6.15m b/d in March, is 25% above the previous high of 4.92m b/d in March 2020.

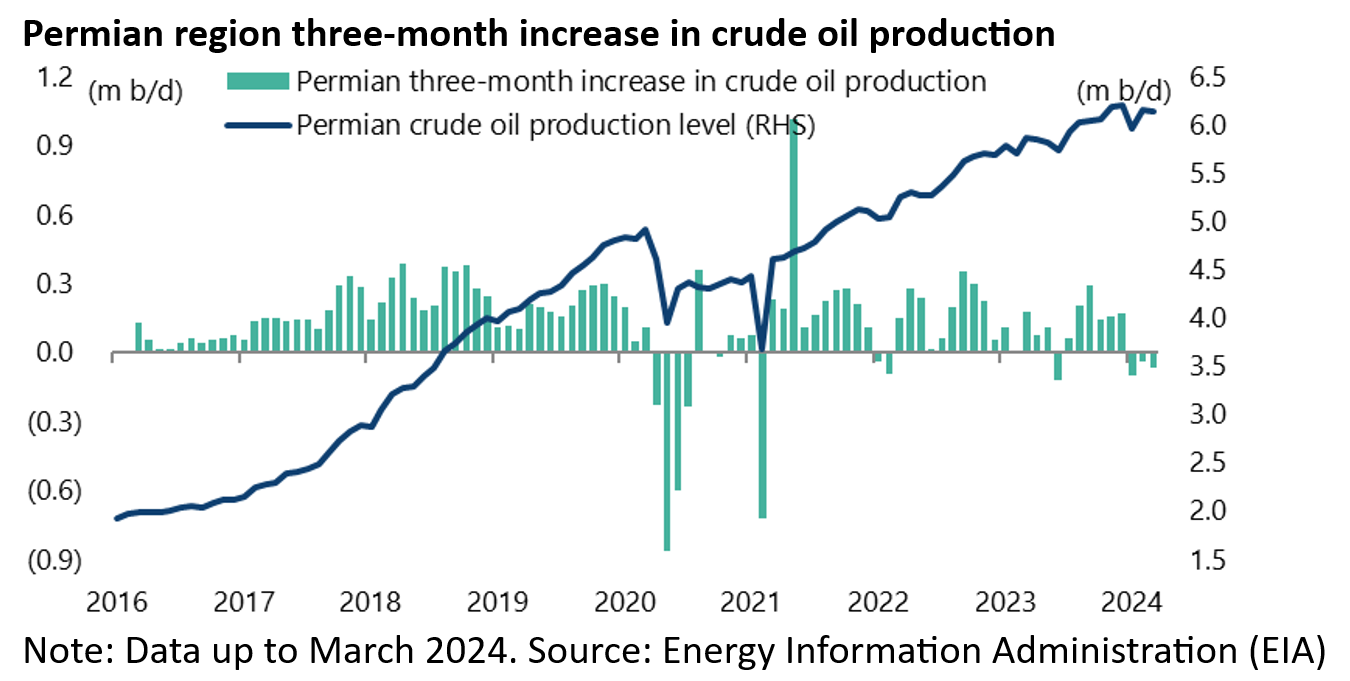

On this point, crude oil production in Permian has declined by 63,868 b/d over the past three months to March or a monthly average decline of 21,289 b/d.

By contrast, Permian production increased by 1.11m b/d over the past two years to a peak of 6.215m b/d in December 2023, or an average 553,483 b/d per year (46,124 b/d per month).

The History Behind Today’s Geopolitical Tensions

The other issue that could trigger a further rise in the oil price is, obviously, rising geopolitical tensions.

In this respect, this writer has been reading of late a memoir by experienced US career diplomat William Burns who since March 2021 has also been head of the Central Intelligence Agency (CIA) (see book “The Back Channel: A Memoir of American Diplomacy and the Case for Its Renewal” by William J. Burns, Random House, March 2019).

Two passages from this memoir are illuminating in view of current developments.

The first is Burns recalling that then US Secretary of State James Baker in May 1989 told the annual American Israel Public Affairs Committee (AIPAC) conference in Washington that “now is the time to lay aside, once and for all, the unrealistic vision of a greater Israel”.

When in response to this then deputy Israeli foreign minister Bibi Netanyahu accused the Bush administration of “lies and distortions”, Baker, according to Burns’ account, banned the now Israeli Prime Minister from the State Department for the next 18 months.

Netanyahu at the time was the protégé of then Israeli Prime Minister Yitzhak Shamir.

The other episode of relevance to the present is a Baker reassurance to then Soviet leader Mikhail Gorbachev in Moscow in February 1990 that there would be no extension of NATO’s jurisdiction or forces “one inch to the east” of the borders of a reunified Germany.

Burns recalls in the memoir, which was first published in 2019, that “The Russians took him at his word and would feel betrayed by NATO enlargement in the years that followed, even though the pledge was never formalized and was made before the breakup of the Soviet Union.

It was an episode that would be relitigated for many years to come.”

It would be interesting to know what Burns, in his new role as head of the CIA since March 2021, is advising now.

Burns, who served in the US embassy in Moscow in the mid-1990s and then between November 2005 and May 2008 as US ambassador in Moscow, also makes it clear in the memoir that during his first posting the embassy at that time had concerns about the efforts in the Clinton administration to promote NATO expansion.

Recalling how Clinton followed through on NATO expansion, following his re-election as president in 1996, by extending formal invitations to Poland, Hungary and Czech Republic to join NATO in the summer of 1997, Burns quotes famous US diplomat George Kennan who called the expansion decision “the most fateful error of American policy in the entire post-Cold War era.”

It has to be hoped that that statement does not turn out to be prophetic as it currently sounds.

Meanwhile Congress’ passage on 23 April of the US$61bn aid package for Ukraine ensures that the Ukraine-Russia conflict will continue for now.

Higher For Longer Rates are a Big Problem for Private Equity

If geopolitics is one issue facing markets, the other is higher for longer interest rates given the decline in monetary easing expectations since the start of this year as regards the Federal Reserve.

The Fed funds futures are now discounting only 40bp of Fed rate cuts by the end of 2024, down from 168bp anticipated in mid-January.

Still this is much less of an issue for listed companies than for the formerly booming world of private equity.

That this boom has reached a scale of macroeconomic significance was highlighted to this writer by the findings of an annual report on the private equity industry by consultancy firm Bain & Company (“Global Private Equity Report 2024” by Hugh MacArthur, 11 March 2024).

This report highlights, among other details, that private equity companies were sitting at the start of this year on 28,000 unsold companies globally worth a hoped for more than US$3tn.

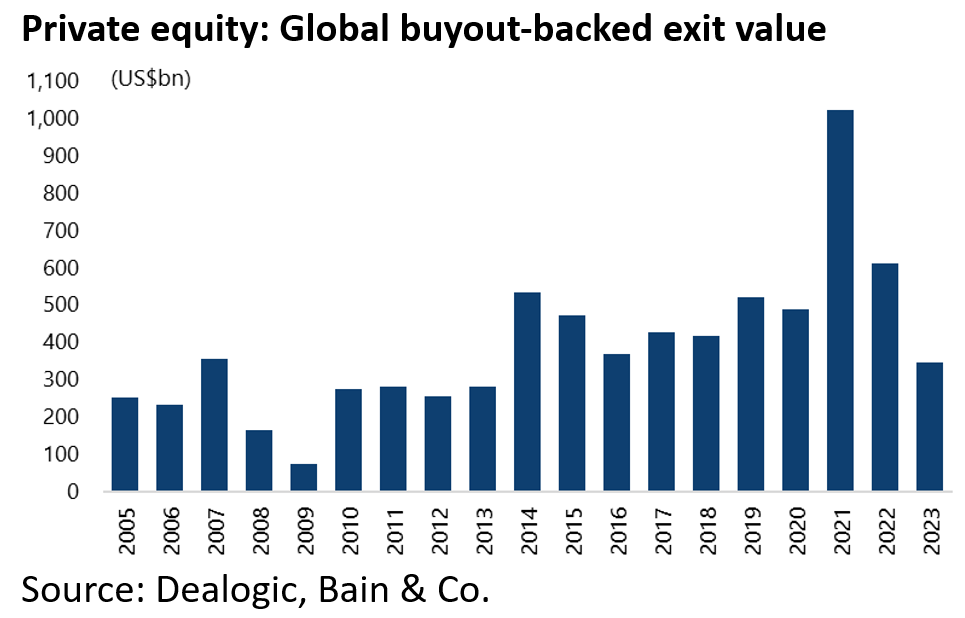

The Bain report also notes that last year the combined value of companies sold by the PE industry, privately or via public markets, fell by 44% to a decade low of US$345bn, down 66% from the peak reached in 2021.

This is clearly why the alternative industry has a lot invested in the hoped for commencement of Fed easing sooner rather than later.

The same Bain report also notes that, with a record 26% of global buyout “dry powder” now four years old or older, general partners are under growing pressure to do deals.

Total global buyout deal value declined by 37% YoY to US$438bn in 2023, the lowest level since 2016, and down 60% from the peak of US$1.1tn in 2021.

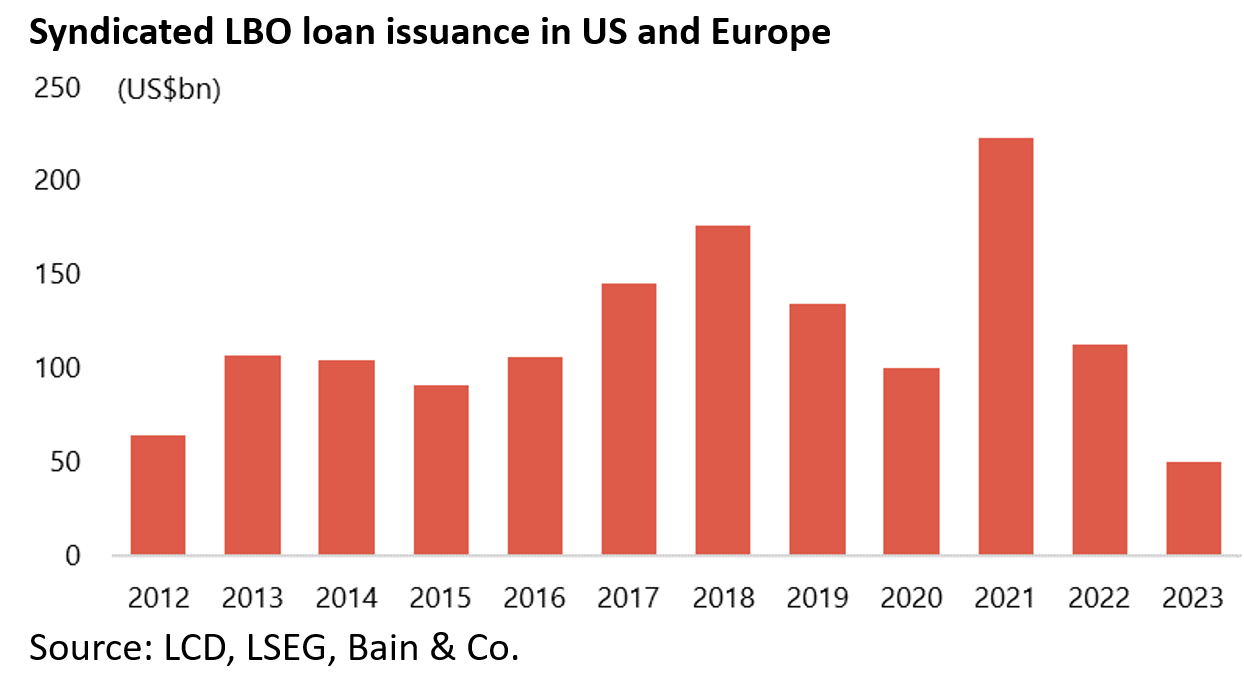

Syndicated leveraged buyout (LBO) loan issuance also plunged by 56% to US$50bn in 2023, making it hard to finance transactions.

Last year US$95bn in leveraged loans came due while by the end of 2025 loans worth nearly US$300bn will mature.

As for private fund-raising, one bright spot has been the raising of so-called secondary funds which surged by 92% YoY in 2023.

These so-called secondary funds, many of them raised by prominent private equity franchises, have been buying from “locked up” limited partners (i.e investors in private equity funds) who have been willing to sell their holding on the secondary market at a discount.

Meanwhile, surveys suggest that, despite all of the above, limited partners (LPs) remain committed to private equity, according to Bain.

But as a practical matter, increasing allocations will come down to cash flows.

LPs have been cash flow negative for four out of the last five years as unexited assets began to pile up.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.