Trulieve Cannabis Corp (CNSX: TRUL , OTCMKTS: TCNNF) has posted their results for Q4 2019.

Revenue came in at $79.7M which beat analysts’ estimates of $79.54M

Adjusted EBITDA came in $45.0M which beat estimates of $32.19M

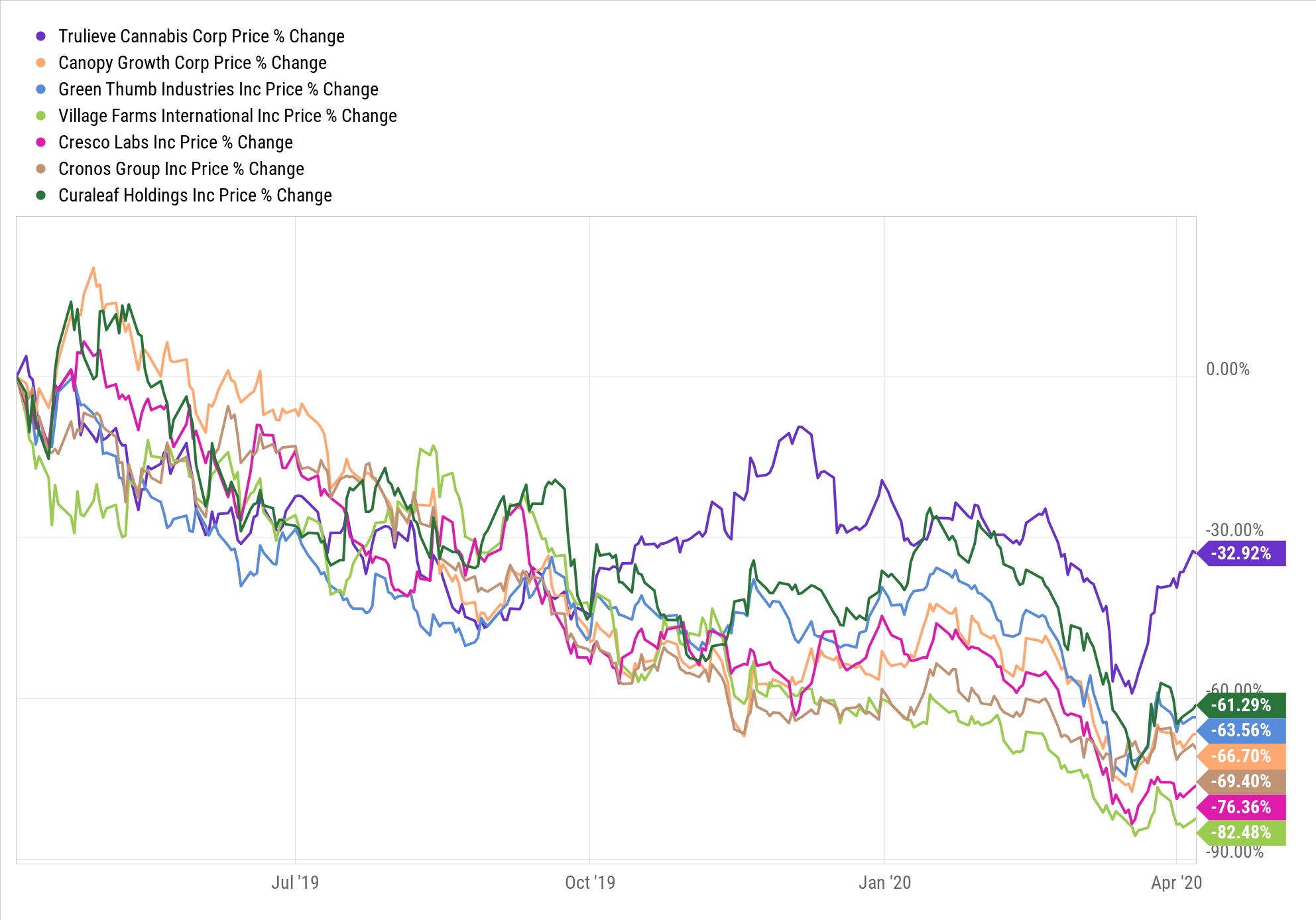

Comparing Trulieve’s stock performance to its peers, we see that although the stock price has decline by over 30% since a year ago, it is vastly outperforming all of its major peers in the cannabis industry by a wide margin.

Trulieve Stock Performance (1 Year) Vs. Peers

Although, given that it is still a decline of over 30%, many investors have been wondering if the stock is now undervalued.

15% Of Trulieve Shares Will Be Released From Lockup in May 2020

It is worth mentioning that current and perspective investors should keep in mind of the announcement made last December that Trulieve will extend its lockup period that was originally due in January to May 15th, 2020.

On that day, 11,205,960 shares which represent 15% of the subordinate voting shares, will be released from the restrictions of the lockup agreement.

54,047,133 of the subordinate voting shares of the company shall remain subject to the lockup agreement restrictions until July 25, 2020.

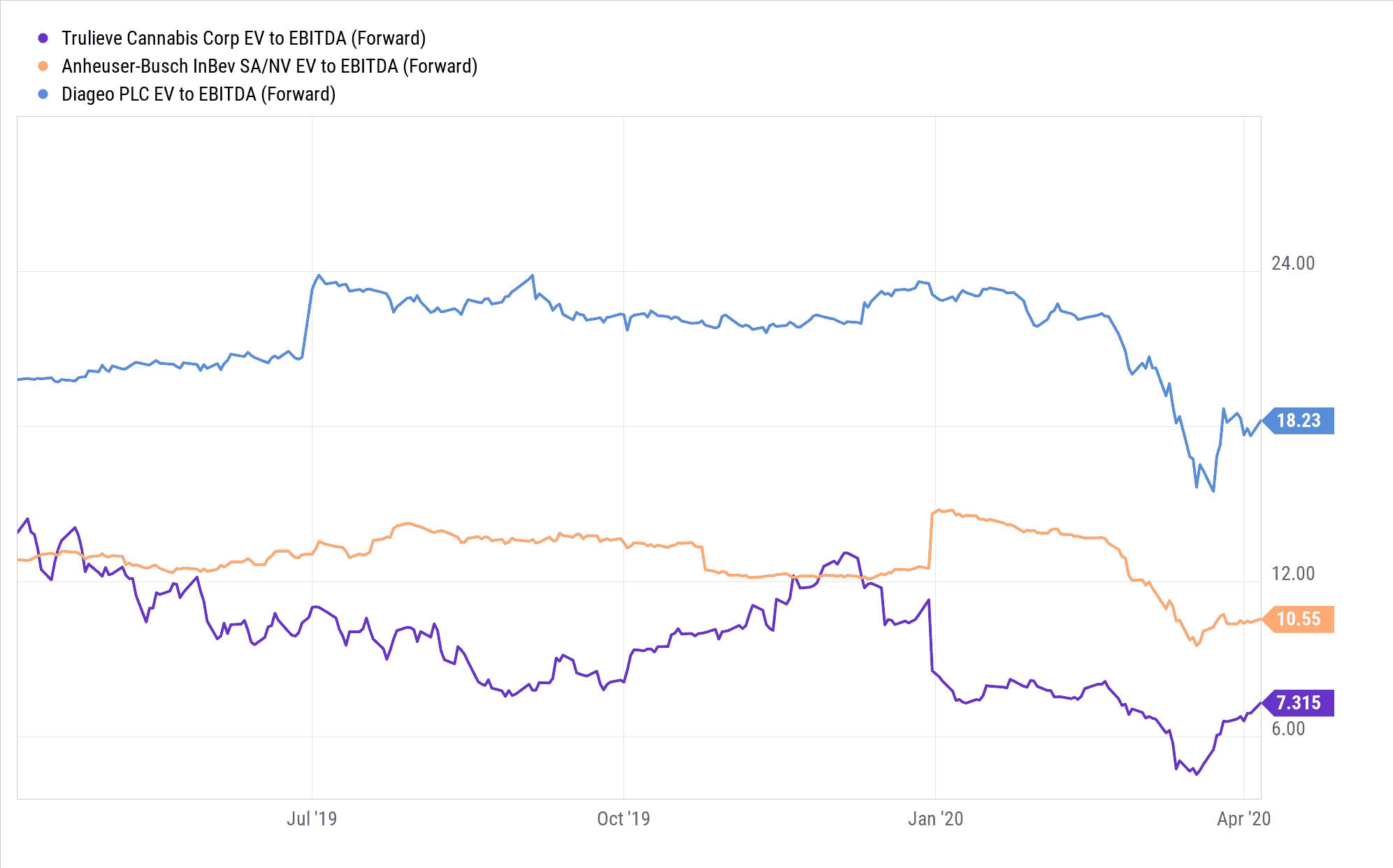

The Ultimate Value Cannabis Stock?

Previously we have reported on the value case for Trulieve as they trade at a relatively low EV/EBITDA compared to some major companies in the alcohol space. And this still remains the case.

Trulieve EV/EBITDA (Forward) VS. Alcohol Companies

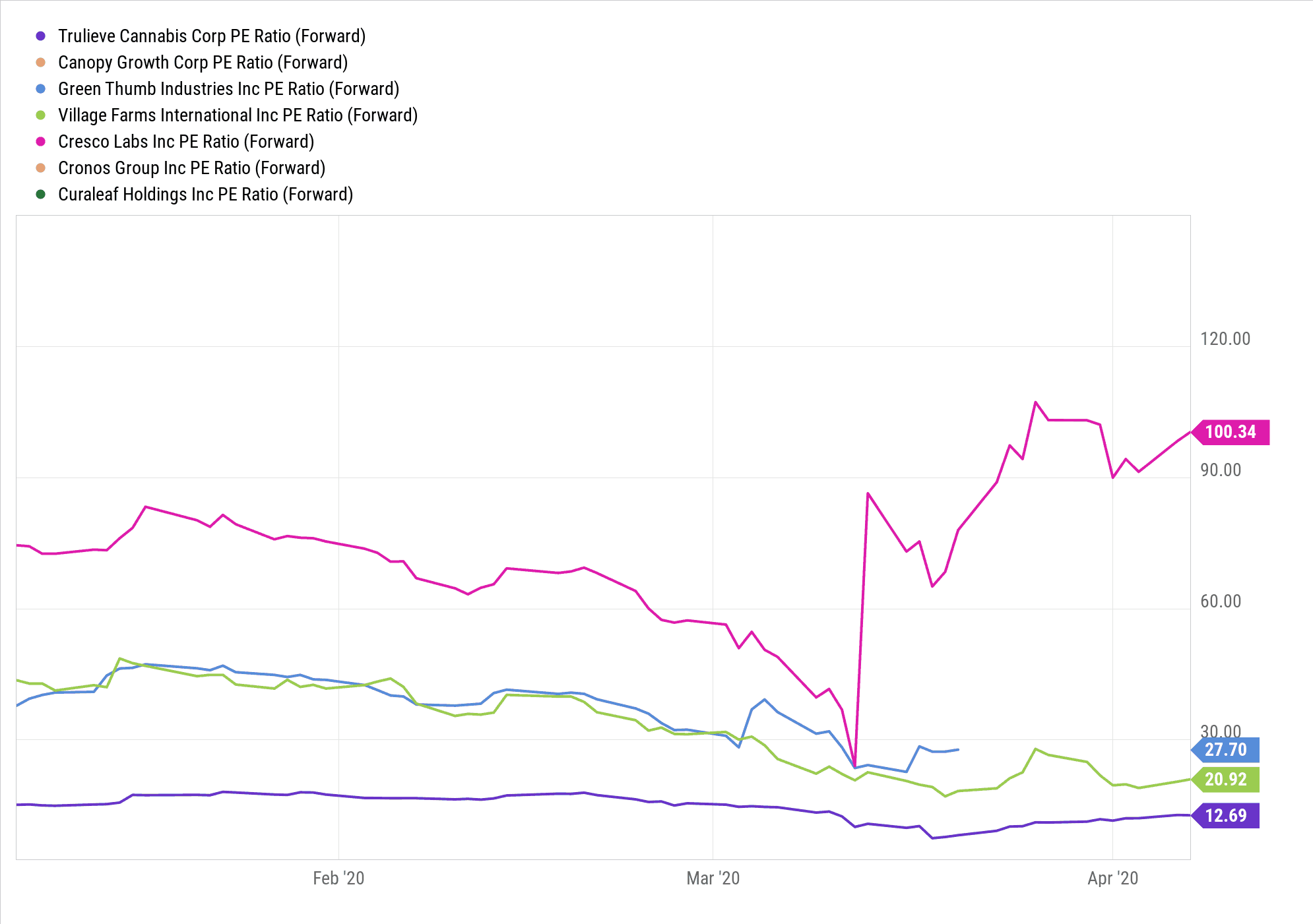

Comparing the forward P/E ratio of Trulieve versus its peers, we see that not only is Trulieve one of the few cannabis companies that is consistently profitable, it also has the lowest forward P/E compared to its peers.

Trulieve Forward P/E Vs. Peers

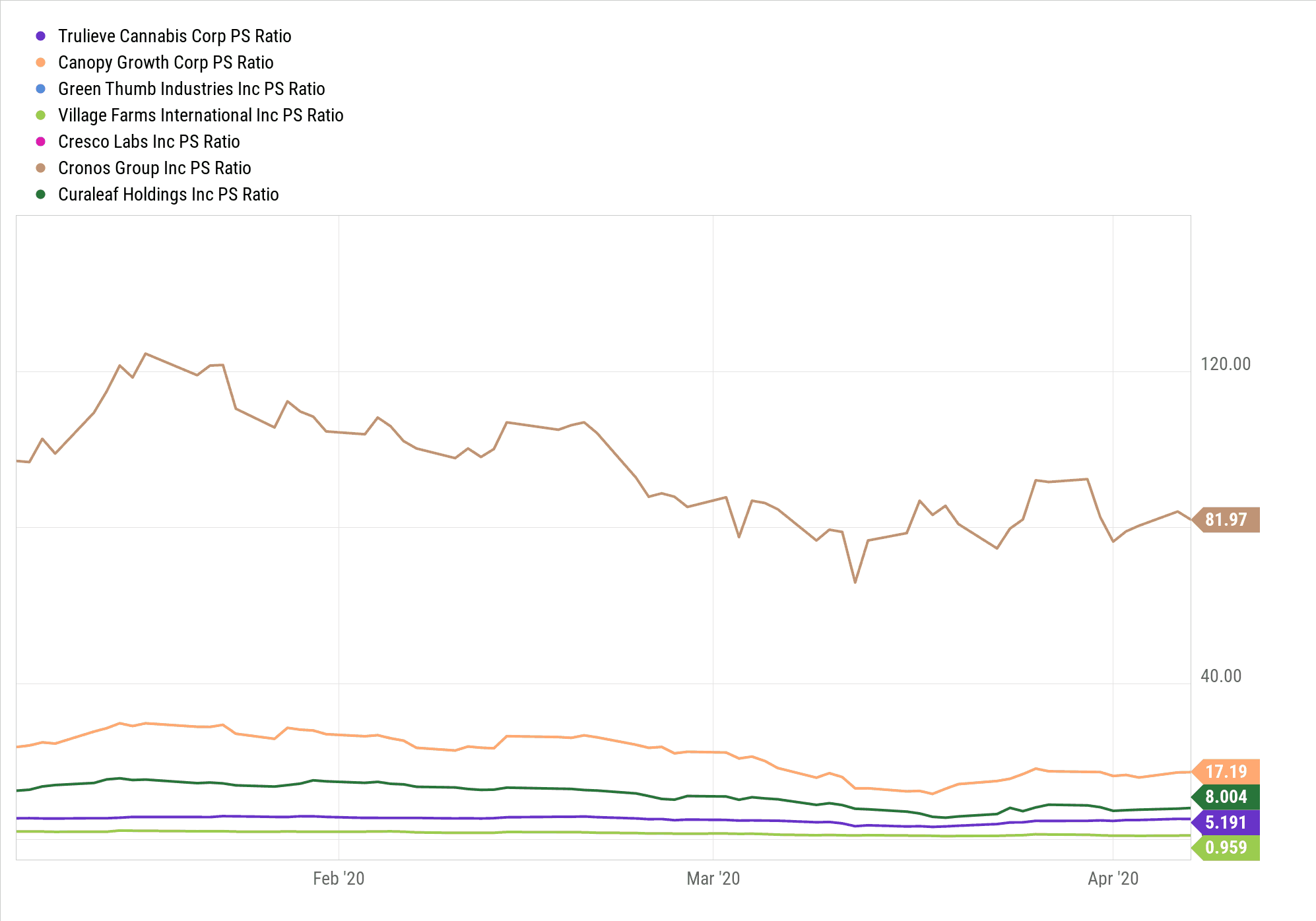

Although some may argue that Trulieve’s price to sales ratio of over 5 still seems a bit high, it is not at all uncommon in the cannabis industry and in fact ranks among the lowest compared to its peers.

Trulieve P/S Ratio Vs. Peers

It seems as though Trulieve is a potential brightspot in an industry that is otherwise not known for its profitability or low valuations.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.