Trump’s Anti-China Theatrics

It has become almost a pantomime. Grizzle refers to the slew of anti-Chinese measures announced by the Trump administration in recent weeks, of which perhaps the most significant for investors is the ban on US citizens transacting on WeChat as part of the Trump administration’s so-called Clean Network Programme.

Why is this called a pantomime?

The reason is that the flurry of executive orders signed by Donald Trump seem almost like a parody of China bashing. The prime driver of this flurry of activity is clearly the proximity of the presidential election and the desire of the China hawks led by Secretary of State Mike Pompeo to implement as much of their national security agenda before election day and potential defeat removes them from office.

The hope, presumably, is that once such initiatives as the Clean Network Programme are implemented that de facto reality means that they will take on a life on their own.

Meanwhile, the aggressive announcements led by the Trump administration’s chief China hawk, Pompeo, are as sweeping as they lack specific detail, which at a minimum creates uncertainty for investors.

WeChat Executive Order Open to Interpretation

Consider for example the ban on WeChat, which is due to be implemented from 20 September, or 45 days after Trump signed the executive order on 6 August. A narrow definition of the wording would mean that US-based persons can no longer communicate with their mainland Chinese contacts via WeChat.

This would clearly inconvenience the Chinese diaspora in America but nothing more dramatic. But a broader reading of the executive order could be interpreted as meaning that American companies and other “US persons” should not deal with Tencent period since Tencent is the owner of WeChat.

To be precise, the executive order on WeChat stated that the following actions shall be prohibited:

It would seem clear that the Trump administration’s hawks like Pompeo, and former journalist Deputy National Security Advisor Matthew Pottinger, would like the interpretation to be as broad as possible.

The latter is probably the author of the remarkably ideological Cold War-like White House paper published in May (United States Strategic Approach to the People’s Republic of China, 20 May 2020).

Still whether a re-elected Trump is going to go along with all this remains debatable despite his undoubted desire to appear tough on China in the presidential campaign.

Both Tencent and ByteDance, owner of the other recently banned Chinese app TikTok, are major customers of the US tech sector.

Meanwhile, a ban on WeChat on China’s Apple Store would have very negative implications for Apple’s successful China business.

Apple’s iPhone revenues increased by only 1.7% YoY in the second quarter. Yet the cheaper iPhone SE, launched in April, was a big hit in China. Hong Kong-based market research firm Counterpoint Research estimates that the number of iPhones sold in China in 2Q20 increased by 32% YoY to 7.4m.

Lower COVID Cases and Urban Unrest Narrow Biden’s Lead in Polls & Betting Markets

For such reasons it could be the case that this flurry of Trumpian executive orders targeting China could turn out to be another negotiation by the Donald before he does another U-turn.

And that is to assume he is re-elected, and that has definitely become more of a possibility as both the polls and the betting odds have moved in his favour in the past few weeks, helped by both the decline in COVID-19 cases and the focus on street violence in Democrat-run cities.

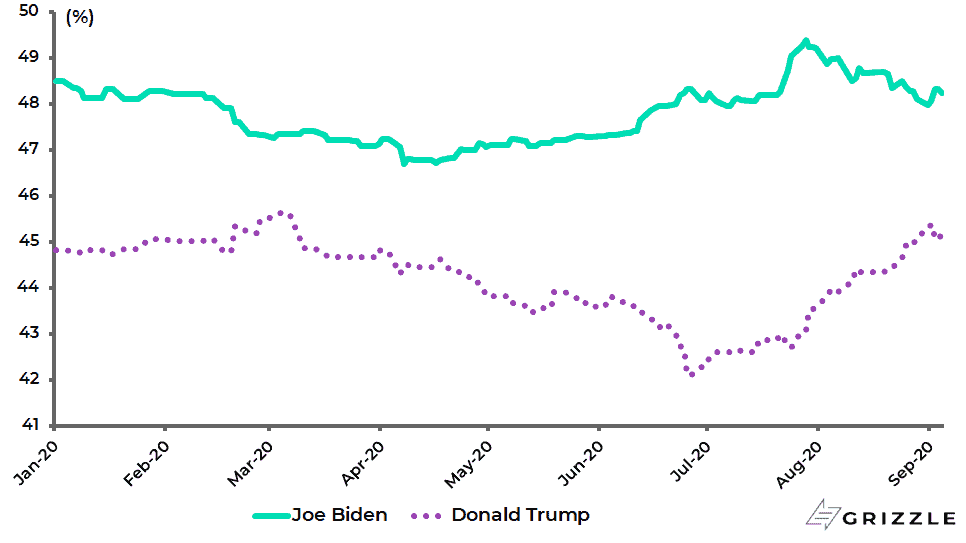

National opinion polls show that Biden’s lead against Trump has narrowed from 10% in late June to 7%.

While, more importantly, Biden is now leading Trump by only 3% in the six key marginal states, down from 6.3% in late July.

2020 US Presidential Election Opinion Polls in Six Battleground States

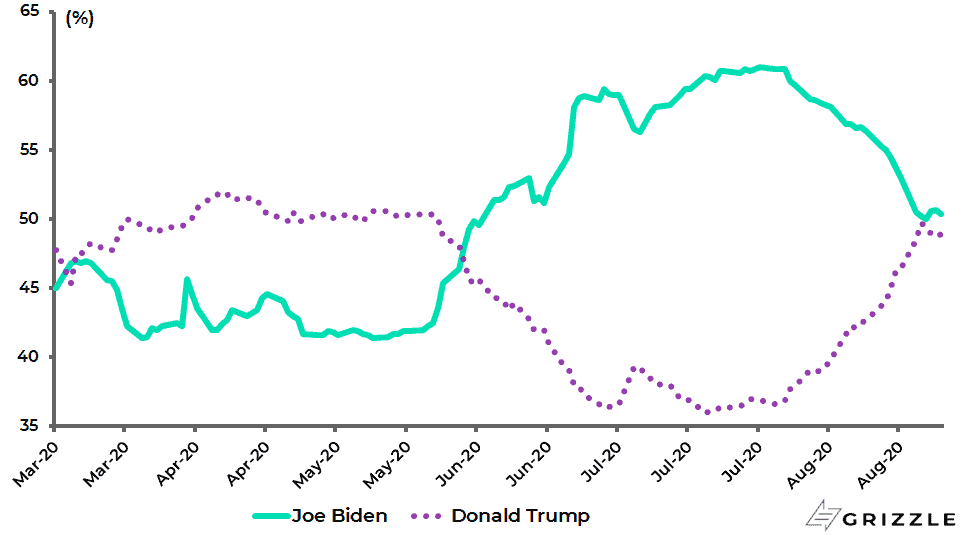

Betting markets also predict that Trump’s odds to win are now 48.9%, up from 36% in mid-July, while Biden’s odds to win have declined from 61% in late July to 50.4%, according to poll tracker RealClearPolitics.

Betting Odds – 2020 US Presidential Election

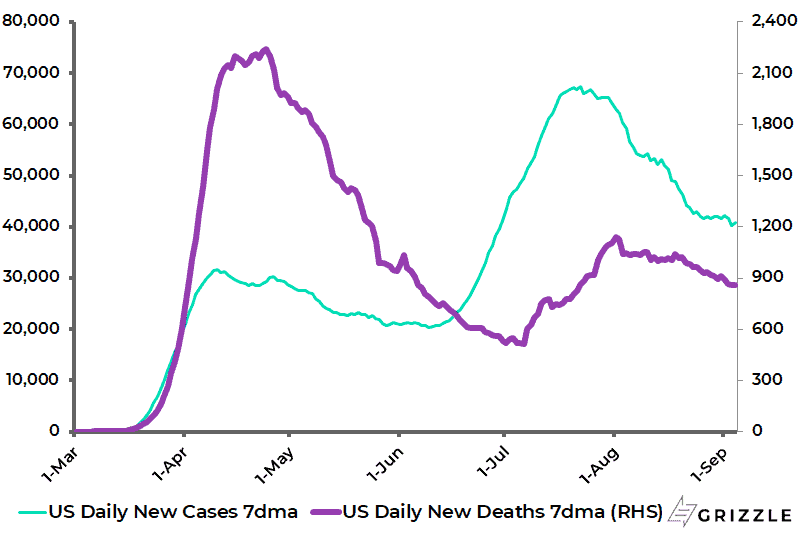

As for the Covid-19, the 7-day average number of daily cases has declined by 39.2% from the peak reached on 22 July, while the 7-day average number of daily deaths is down 24.7% from the recent high reached on 1 August and is 62% below the April peak.

US Covid-19 7-day Average Daily New Cases and Deaths

This is why it is critical for the 45th American president that the pandemic is perceived to have peaked.

All the polls suggest that Trump is perceived by voters, rightly or wrongly, to have mismanaged the pandemic.

On this point, a Economist/YouGov poll conducted between 30 August and 1 September showed that 55% of the respondents disapprove of the way the Donald has handled Covid-19 and only 38% approved of it.

It is this dynamic which has created the temptation for Trump to keep blaming China for Covid-19.

Yet the risk is that this tactic will simply look to the electorate like a crude ploy to deflect blame from his own perceived mismanagement.

What about the Democrats?

The incentive for them has clearly been to keep hyping up COVID-19, keep restrictions on schools and economic activities in place in the states they control and keep their potentially vulnerable 77-year-old presidential candidate wearing a mask in his basement.

Still, that approach has become harder to maintain as the COVID cases have declined and focus increased on what has been going on in the streets in Democrat-run cities as this is an issue which risks losing the political middle ground to the Republicans.

China Avoiding Overt Entanglement with US Administration

What about China?

So far, despite some to be expected tit for tat, Beijing has shown remarkable restraint in the face of the various American provocations.

The lack of a more forceful reaction is explained by the practical reality that there is no point in getting into a major row with a US administration which may soon be out of office.

And if Trump is re-elected Beijing probably thinks, as does this writer, that the Donald would pull back on a lot of the anti-China stuff.

In fact he is likely to look to revive phase-2 of his trade deal.

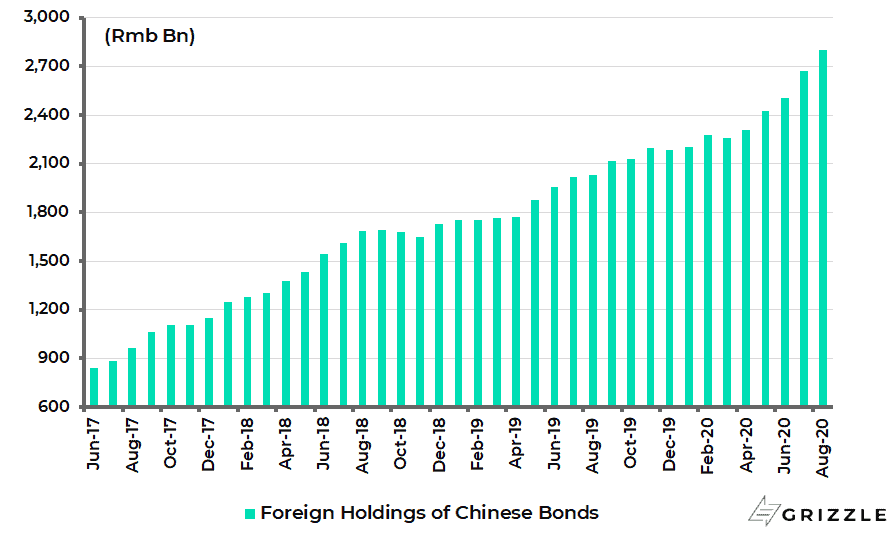

Meanwhile, if the agenda of the national security hawks in Washington is ultimately to destabilise China’s capital account and its supply lines, the irony is that the data shows a continuing stampede by foreigners to own Chinese bonds.

Foreign holdings of Chinese bonds increased by a further Rmb130bn in August and were up Rmb615bn or 28% in the first eight months of 2020 to Rmb2.80tn at the end of August.

This is not surprising since Chinese macroeconomic policy in the post-Covid world is so much more orthodox than in the G7 world.

Foreign Holdings of Chinese Bonds

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.