Twilio (NYSE:TWLO) posted their Q4 2019 earnings results today.

Revenue was $306.6 million which missed analysts’ targets of $312.85 million.

EPS came in at $0.04 which beat analysts’ targets of $0.01.

Twilio stock has a wild ride for the past year. Around this time last year, the stock was trading at about $110/share and then crashing to around $91/share this past November before rocketing back up above $120/share in the past few months. Much of the volatility was triggered by Twilio’s last quarter results which despite beating estimates both on the top and bottom line, caused the stock to crash due to weak guidance put out by the management.

What Does Twilio Even Do?

Twilio is a cloud communications platform as a service (CPaaS) company based in San Francisco, California. Twilio allows software developers to programmatically make and receive phone calls, send and receive text messages, and perform other communication functions using its web service APIs.

In plain English, Twilio builds the technology that a company needs to send you those verification codes you need for two-factor authentication. There’s much more that Twilio does of course, that’s just the Too Long: Didn’t Read (TL:DR) version. You may think that this is boring, and perhaps to some people it is, but there is big money in Software as a Service (SaaS) and these companies are the secret workhorses behind what makes all your software services function as desired.

Software As A Service (SaaS) Is The Name of the Game in 2020

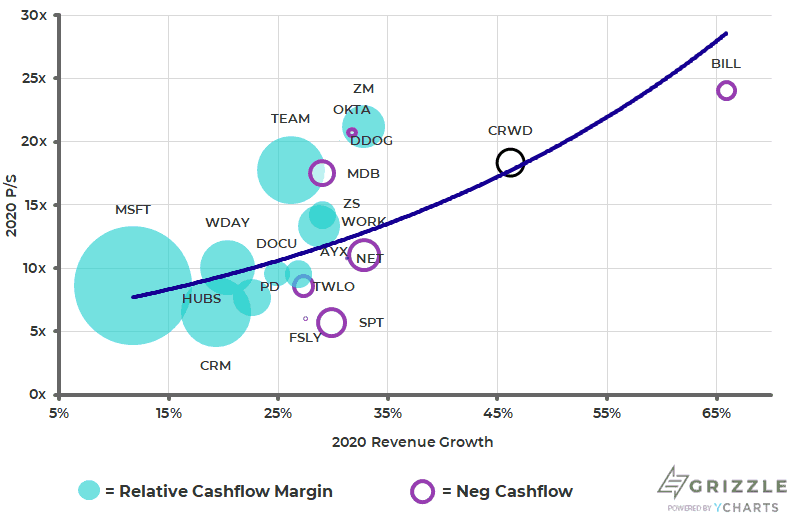

Despite its wild ride in stock price, Twilio seems to have regained the favour of Wall Street as its valuation is relatively high right now.

Although it is still far from being the most highly valued tech company out there, considering that Twilio’s cash flows are still negative, it is impressive that Twilio is still valued at almost 10x P/S and is growing their revenues faster than many other SaaS companies.

What’s Next For Twilio

Twilio is pushing hard into the email services space with their platform SendGrid which they acquired last year. The company hopes that SendGrid will be a huge growth engine in 2020 and Wall Street is watching closely for its performance.

A major risk for Twilio going forward is its reliance on big contracts to generate its revenue. In 2018, 18% of Twilio’s revenue came from just 10 contracts. And WhatsApp’s contract made up 7% of that. So all it would take for Twilio to miss big on revenue and earnings is for one of two of those big contracts to fall through.

Setting that aside though, it does appear that Twilio is a growth beast. The company has boasted that it has a $66 billion total addressable market and if they are to be believed, this could mean way more growth for the company in the future.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.